In This Guide

A fee increase is a recurring monthly cost change. A special assessment is a one-time lump sum for a specific project. For a buyer, the special assessment is usually worse because it lands as cash at or shortly after closing.

You get the seller's disclosure and somewhere in the HOA packet there are two numbers. The monthly dues went up. There is also a $24,000 line called "special assessment, balcony repair, due in three installments." Most buyers ask the listing agent which one matters more, get a shrug, and move on.

That shrug costs people money. The Cricket Club in North Miami billed owners roughly $134,000 per unit in 2024 after a $30 million special assessment. Forty units listed for sale within weeks. The buyers who closed in the months right before that vote inherited the bill. The buyers who paused, read the resale packet, and asked the right question walked away.

This post is the buyer's read on the two terms. Plain definitions, the state-by-state approval rules that actually apply, how each one hits a mortgage, and the diligence workflow that catches both before you sign. For the strategic frame, our HOA financial health guide covers the five-number HOA health check for buyers. This post is the close read on which bill is which.

The 60-Second Answer: Two Bills, Two Very Different Signals

A regular assessment increase changes your monthly carrying cost. A special assessment is a one-time charge for a specific project, due as a lump sum or in installments.

Both come from the same source: the HOA budget. Both are legally enforceable. The difference is timing, purpose, and how each one shows up in your life.

| Feature | Regular assessment increase | Special assessment |

|---|---|---|

| Frequency | Monthly or quarterly, ongoing | One-time (sometimes installments) |

| Purpose | Funds the annual operating budget and reserve contributions | Funds a specific project (roof, balcony repair, milestone inspection) |

| Approval | Board vote within statutory cap; member vote above the cap | Board vote with notice; member vote for amounts above cap |

| Mortgage impact | Raises DTI, lowers buyer pool | Project warrantability flag; may need to be paid before close |

| Tax treatment | Generally not deductible for primary residence | May add to basis if capital improvement (per IRS Pub 527) |

Buyer takeaway: a fee increase tells you the board has finally adjusted the dues. A special assessment tells you the board ran out of reserves before the work was done. The second is the louder signal.

What Counts as a Regular Assessment Increase

Regular assessments are the recurring dues set by the board through the annual budget. Most states cap how much the board can raise them without owner approval.

Every condo and HOA adopts an annual budget that covers operating expenses (insurance, management, landscaping, utilities) plus a transfer to reserves for future capital projects. The regular assessment is each owner's share, billed monthly or quarterly. When operating costs rise, the board raises the assessment to match. That is the "fee increase" you see in disclosure.

What protects owners from runaway increases is the statutory cap. The cap varies by state. In California, Civ. Code §5605(b) bars the board from raising a regular assessment more than 20% above the prior fiscal year without member approval. Arizona's A.R.S. §33-1803 applies a parallel 20% cap for planned communities. Texas has no statewide percentage cap; the limit comes from the declaration, and Tex. Prop. Code §209.0051 only requires the increase to be considered in an open board meeting.

A clean signal for buyers: ask the HOA for the last three years of adopted budgets. A board that has held dues flat for three years while operating costs and insurance premiums climbed is one that is likely deferring a correction. That correction lands as either a sharp fee increase or a special assessment, sometimes both. Our post on the hidden cost of artificially low dues covers the pattern.

What Counts as a Special Assessment

A special assessment is a one-time charge tied to a specific project. Funds can only be used for the stated purpose, and notice rules are stricter than regular assessments.

When the operating budget cannot cover a capital project and reserves are short, the board adopts a special assessment. The total cost is divided across units (usually by ownership percentage) and billed as a lump sum, an installment plan, or sometimes financed by an association loan with owner payments amortized over years.

Florida is the clearest example of how notice works. Fla. Stat. §718.112(2)(c) requires 14 days' written notice mailed, delivered, or electronically transmitted, plus a posting on the property and an affidavit of mailing, before a nonemergency special assessment can be considered. Section 718.116(10) then says the post-adoption notice must state purpose, amount, and due date, and that funds collected must be used only for the stated purpose. A board cannot quietly redirect a balcony-repair assessment to plug an operating shortfall.

The largest special assessments in recent memory landed on Florida condos after the 2022 milestone inspection law took effect. See our coverage of Florida's special-assessment wave and milestone inspections that trigger six-figure assessments for the full context. The Cricket Club is the loudest case, but it is not the only one. Yahoo and Axios both reported on multiple South Florida condos issuing six-figure assessments after milestone inspection deadlines, with owners listing units at distressed prices.

State Law: Who Has To Approve Each One

Ten high-volume condo states. Two approval rules each. Most fee-increase caps are 20%, but special-assessment rules vary widely.

The rule that decides whether a board can act unilaterally, or whether owners get a vote, is state law plus the governing documents. The table below covers ten high-volume condo states. Always confirm the current text of any cited statute and read your association's declaration for stricter local rules.

| State | Fee-increase rule | Special-assessment approval rule | Statute |

|---|---|---|---|

| Florida | No state percentage cap; follows budget process and declaration | Board may adopt; 14-day notice required; funds restricted to stated purpose | Fla. Stat. §718.112(2)(c), §718.116(10) |

| California | Board limited to 20% over prior year without member vote | Board limited to aggregate of 5% of budgeted gross expenses without member vote; quorum > 50% | Cal. Civ. Code §5605 |

| Texas | No state percentage cap; declaration controls | Must be considered in open board meeting; no state percentage cap | Tex. Prop. Code §209.0051 |

| Arizona | Board limited to 20% over prior year without member majority | Governed by declaration; open-meeting and notice rules apply | A.R.S. §33-1803 (planned communities); §33-1242 (condos) |

| Colorado | Budget ratification: deemed approved unless vetoed by majority of all owners | Same veto-style ratification when special assessment is built into the budget | C.R.S. §38-33.3-303(4) (CCIOA) |

| Washington | Board proposes budget; ratified unless rejected by majority of unit votes | Same veto-style ratification at meeting 14-50 days after notice; installment payments allowed | RCW 64.90.525 (WUCIOA) |

| Virginia | Governed by declaration | Written notice with amount, reasons, due date; lump sum due no earlier than 90 days after notice; owners may reject by majority vote within 60 days | Va. Code §55.1-1964 (Condo Act); §55.1-1825 (POA Act) |

| Illinois | Governed by declaration | If total annual assessments exceed 115% of prior year, 20% of votes can petition within 21 days for owner vote; majority of total association votes required to reject | 765 ILCS 605/18(a)(8) |

| Massachusetts | Statute does not set a percentage cap; case-law guidance only | Statute does not separately define special assessments; assessed per unit's percentage of undivided interest | Mass. Gen. Laws c.183A §6 |

| New York | No statewide percentage cap; declaration and bylaws control | No statewide percentage cap; declaration and bylaws control under Article 9-B | N.Y. Real Prop. Law §339-y (taxation); Article 9-B (association rules) |

Three honest caveats. Massachusetts has no statutory percentage cap, only case-law guidance. New York has no statewide cap on association-level special assessments; rules come from the declaration filed with the offering plan. Texas has no statewide cap on either type. In all three states, the declaration is the document that matters. Read it.

How Each Shows Up in a Closing File

A fee increase changes a number on the recurring-cost line. A special assessment shows up on the estoppel certificate or resale certificate as a separate, dated item.

Regular assessments appear on the estoppel certificate (Florida) or resale certificate (most other states) as a monthly figure. The buyer takes over from the day of closing forward. If the board just approved a 12% increase that takes effect next month, that increase is the buyer's problem.

Special assessments are itemized separately. The certificate will show the total assessment, the installment schedule, the amount paid to date, and the unpaid balance. Who actually pays depends on the purchase contract and state law. The default in most states is that the seller owes any installment with a due date before closing, and the buyer owes anything due after. Our walkthrough on who actually pays a pending special assessment covers the negotiation script.

One trap. A "pending" assessment that the board has discussed but not voted on does not appear on the certificate. Meeting minutes are where you find those. Read the last 12 to 24 months of board minutes for the words "reserve study," "loan," "special assessment," and "deferred maintenance." If those words appear in a recent meeting and the certificate is clean, the timing of your closing matters.

Mortgage Impact: Why Lenders Treat Them Differently

A fee increase hits your debt-to-income ratio. A special assessment hits project warrantability. Both can kill a loan, in different ways.

Lenders fold the monthly HOA assessment into your debt-to-income calculation. A $300 monthly dues figure becomes $375 after a 25% increase; on a borderline DTI, that swing can tip the file. The buyer with the lowest down payment is usually the first to lose financing when dues rise sharply between contract and close.

Special assessments hit a different gate: project warrantability. Fannie Mae Lender Letter LL-2026-03 (March 18, 2026) requires established condo projects to allocate at least 10% of the operating budget to reserves, rising to 15% for loans dated on or after January 4, 2027. The same Lender Letter also retires Limited Review for loan applications dated on or after August 3, 2026, making Full Review mandatory. Full Review forces lenders to examine reserves, deferred maintenance, and pending special assessments directly. Our post on the 2026 Fannie reserve and review changes walks through the timeline.

On delinquency, Fannie's Selling Guide B4-2.2-02 makes a project ineligible if more than 15% of total units are 60 or more days past due on common expense or special assessments. FHA condo approval applies a parallel 15% cap. A large special assessment that owners cannot pay quickly drives delinquency past that line, and the project goes non-warrantable. Conventional financing dries up. Cash buyers take the discount.

Which Is Worse: A Decision Framework

For owners, the special assessment is usually worse short-term but the fee increase is usually worse long-term. For buyers pre-closing, the special assessment is almost always the bigger threat.

Same bill, different angle depending on who is reading it.

Owner perspective

A $24,000 special assessment is cash you have to find now. A $75/month fee increase is $900 a year, every year, compounding into the next dues hike. Owners who plan to stay 10+ years actually take more total dollars from a fee increase than from a one-time assessment. Owners who plan to sell within 2 to 3 years feel the special assessment more, because it lands inside their holding period.

Buyer pre-closing perspective

The special assessment is the bigger threat. Three reasons. First, it is often paid as a lump sum at closing or in the first year, so it is real cash on top of your down payment. Second, the underlying problem (deferred maintenance, an underfunded reserve study) usually has more work behind it, which means another assessment in 18 to 36 months is plausible. Third, it can flip a project non-warrantable for your loan or your future buyer's. A fee increase, by contrast, mostly affects your monthly carrying cost and DTI.

Refinance or sale

A pending or recently paid special assessment shows up in the next appraisal cycle. If the project is mid-repair and reserves are below Fannie's 10% (or 15% after January 4, 2027), refinance options narrow. A clean recent fee increase has the opposite effect: it signals a board that is funding reserves and is more likely to be inside the Fannie threshold.

Tax treatment

For a primary residence, regular dues and most special assessments are not deductible. The exception is the portion of a special assessment that funds a capital improvement, which adjusts your cost basis (and can reduce capital gains at sale). For a rental property, IRS Publication 527 treats assessments for maintenance and repairs (and interest on improvement loans) as deductible operating expenses, while assessments for capital improvements add to basis and depreciate over the asset's recovery period. The split matters. Always confirm with a CPA before relying on this for a specific filing.

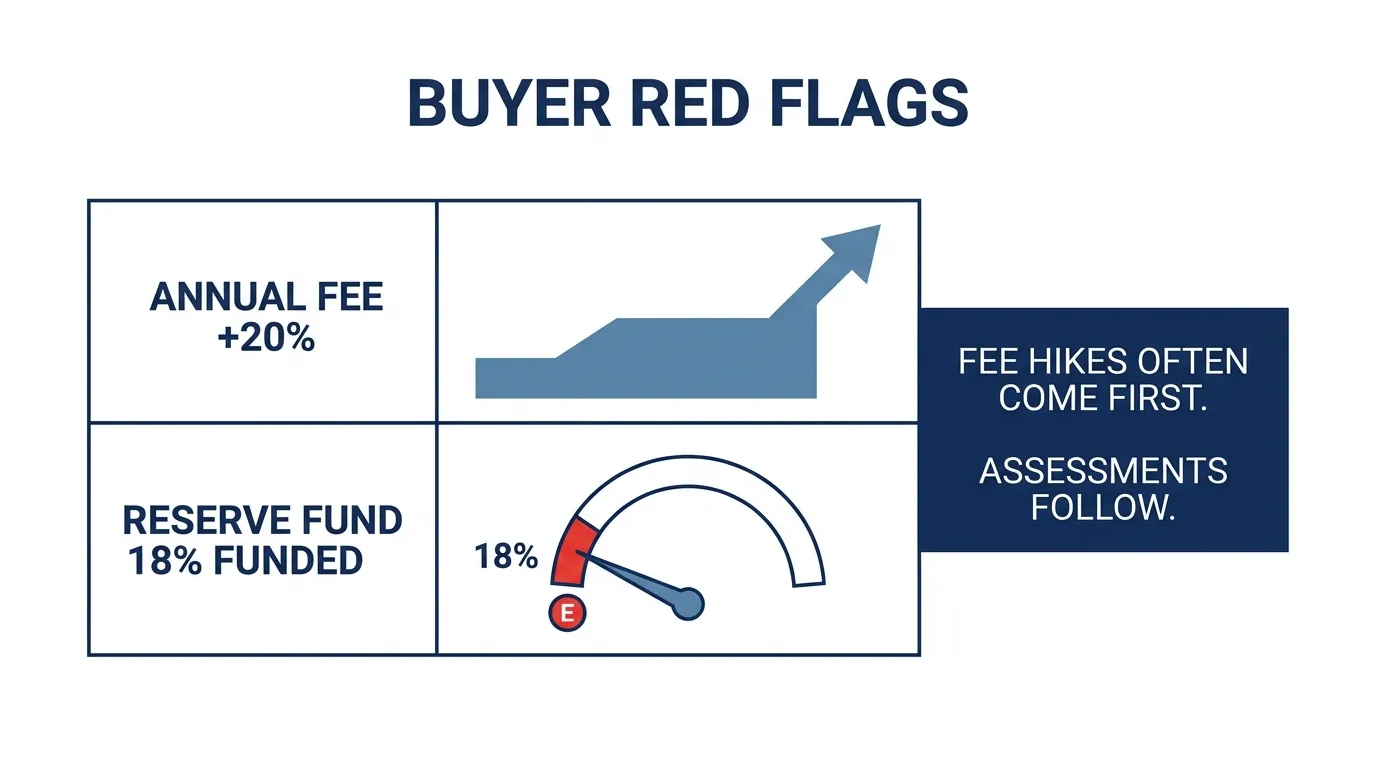

The Hidden Connection: Fee Hikes Often Predict Assessments

A sharp dues increase without a matching reserve plan is one of the strongest leading indicators of a future special assessment, often within 12 to 24 months.

Low reserves often lead to special assessments. That is the framing in BCP Mortgage's analysis of Fannie LL-2026-03, and it matches what we see across the 1,900+ HOA documents we have indexed. The mechanism is straightforward. The board catches up on flat insurance and maintenance costs by raising regular dues. The dues increase covers operating expenses but does not refund the reserve account, which has been quietly drained by years of deferred maintenance and emergency repairs. When the next big component (roof, elevator, balcony) hits its useful life, reserves are not there, and the board passes the bill as a special assessment.

What to look for in the financials. Compare the percent of total assessment income going to reserves against the recommended figure in the reserve study's funding plan. Anything below 10% today (and below 15% next year) is a project Fannie may not warrant. Our explainer on the percent-funded number that predicts special assessments walks through the threshold math.

For the broader pattern of low dues hiding future cost, see why HOA dues function as a second mortgage payment.

A Buyer's 5-Step Diligence Workflow

Five documents, five checks. Done in order, this catches the vast majority of fee-hike and special-assessment risk before the cancellation window closes.

- Pull the last 24 months of board meeting minutes. Search for "reserve study," "loan," "special assessment," "balcony," "roof," "deferred," and "milestone." Our meeting minutes analyzer runs these searches across a full board-year in one pass. A discussion that has not turned into a vote yet is still a discussion you bought into.

- Read the reserve study's percent funded. Below 30% is the tier where surprise assessments become routine. Compare the closing balance in the most recent reserve fund schedule against the study's recommended balance at the same point in time. A gap is a future shortfall.

- Scan the last three annual budgets for line-item jumps. Insurance premiums doubling, utility costs rising sharply, or the transfer-to-reserves line falling year-over-year are leading indicators.

- Request the estoppel or resale certificate. Confirm regular assessment amount, effective date of any increase, and any itemized special assessments with installment schedule and unpaid balance.

- Read the audit footnotes and financial statements. Look for "loan," "contingent liability," "pending litigation," and any reserve methodology disclosure. Our walkthrough on the eight lines a buyer reads on an HOA financial statement covers the read.

The cancellation windows in most states are short. Treat the day you receive the resale package as day zero, and run all five checks before the deadline. If anything fails a threshold, the question goes to the seller, the listing agent, or the HOA management company immediately.

Frequently Asked Questions

What is the difference between a special assessment and a regular assessment?

A regular assessment is the recurring monthly or quarterly dues paid by every owner to fund the annual operating budget and reserve contributions. A special assessment is a one-time charge for a specific project (roof, milestone inspection, balcony repair) when the operating budget and reserves cannot cover it. Special assessments must be used for the stated purpose under most state statutes.

Which is worse for a buyer: a fee increase or a special assessment?

For a buyer pre-closing, the special assessment is usually worse. It often lands as a lump sum at or near closing, the underlying maintenance problem suggests more work is coming, and a large unpaid balance can flip the project non-warrantable for Fannie, Freddie, or FHA financing. A fee increase mostly affects monthly carrying cost and debt-to-income ratio.

Can an HOA raise dues without owner approval?

In most states, yes, up to a statutory cap. California (Cal. Civ. Code §5605) caps board-only increases at 20% above the prior year. Arizona (A.R.S. §33-1803) applies a parallel 20% cap. Texas has no statewide percentage cap; the declaration controls. Above the cap, an owner vote is required.

Who pays a special assessment at closing, buyer or seller?

It depends on the purchase contract and state law, but the default in most states is that the seller owes any installment with a due date before closing, and the buyer owes anything due after. Some contracts shift the entire pending balance to the seller. The estoppel or resale certificate itemizes paid and unpaid amounts. Always confirm with the closing attorney or escrow officer.

Are HOA special assessments tax deductible?

For a primary residence, no, with one exception: the portion of a special assessment that funds a capital improvement adjusts your cost basis and can reduce capital gains at sale. For a rental property, IRS Publication 527 treats assessments for maintenance and repairs as deductible operating expenses, while capital-improvement assessments add to basis and depreciate. Confirm with a CPA.

Does a recent fee increase predict a future special assessment?

A sharp dues increase without a matching boost to the reserve contribution is one of the strongest leading indicators of a future special assessment. The board has caught up on operating costs but has not refunded reserves, so the next big capital component lands as a separate bill, often within 12 to 24 months.

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

Sources & References

- Fannie Mae Lender Letter LL-2026-03 (March 18, 2026). Reserve allocation rising from 10% to 15% on Jan 4, 2027; Limited Review retired Aug 3, 2026

- Fannie Mae Selling Guide B4-2.2-02. 15% delinquency cap on common expense or special assessments

- FHA Condo Approval Guidelines. 15% delinquency cap for FHA project eligibility

- Cal. Civ. Code §5605. 20% regular assessment cap and 5% special assessment cap

- Fla. Stat. Chapter 718. Notice and purpose-restriction rules for condo special assessments

- A.R.S. §33-1803. Arizona 20% regular assessment cap

- Tex. Prop. Code §209.0051. Texas open-meeting requirement for assessment changes

- C.R.S. §38-33.3-303(4). Colorado CCIOA budget ratification

- RCW 64.90.525. Washington WUCIOA budget and special-assessment ratification

- Va. Code §55.1-1964. Virginia Condo Act additional assessment rules

- 765 ILCS 605/18(a)(8). Illinois 115% trigger and owner-petition rule

- Mass. Gen. Laws c.183A §6. Massachusetts common expense framework

- N.Y. Real Prop. Law §339-y. New York separate taxation rule

- IRS Publication 527. Rental-property treatment of repair vs improvement assessments

- Highest & Best: Cricket Club $30M assessment. Per-unit figure and listing fallout

- BCP Mortgage: 2026 Fannie Mae Condo Guidelines. Low reserves and special-assessment connection

Disclaimer: This article is for educational purposes only and does not constitute legal, tax, financial, or real estate advice. Statute citations and regulatory thresholds are current as of publication and may change. Fannie Mae, Freddie Mac, and FHA rules are subject to lender overlays. State laws vary, and association declarations can impose stricter limits. Consult a qualified real estate attorney, CPA, or mortgage professional for guidance specific to your situation.