In This Guide

Median condo HOA fees hit $420/month in 2026, up 29% since 2019. Every $100/month in dues removes roughly $16,000 in purchasing power. Here's what's driving the increase and what buyers must check.

HOA fee level alone isn't the signal. The structure of those fees inside the operating budget is. That structure shows up in The GoverningDocs 5-Number HOA Health Check as reserve contribution rate (#3) and connects to delinquency rate (#2) when fee jumps push owners into late status. Both are criteria in the Warrantability Checklist, so a fee structure that fails either one can flip the building non-warrantable. The composite verdict shows up as the GoverningDocs HOA Health Grade on every property report.

What does a $420/month median fee actually tell a buyer?

Almost nothing on its own. Two buildings with identical $420 fees can have opposite financial health. Building A allocates 25% to reserves and is 75% funded, so the fee is sustainable. Building B allocates 5% to reserves and is 25% funded, so the fee is too low, and a $50K+ assessment is on the horizon to catch up. The signal isn't the dollar amount. It's the contribution rate inside the budget and the resulting percent funded in the reserve study.

Per Fannie Mae Lender Letter LL-2026-03, the contribution-rate floor is rising from 10% to 15% effective January 4, 2027. Buildings that have been keeping fees artificially low by under-contributing are about to face a forced fee increase (raise contributions to 15%) or a non-warrantability flag (don't, and lose conventional financing for every unit). Either outcome shows up in the buyer's monthly cost.

The Shadow Mortgage Nobody Mentions

HOA fees have risen faster than mortgage rates, insurance premiums, and home prices in many markets. Most buyers treat them as a footnote. They're not.

You see the listing. The price looks right. The monthly payment looks manageable. Then you notice the HOA fee: $420 a month. That's $5,040 a year. Money you pay before the mortgage, before property taxes, before any maintenance of your own unit. It's non-negotiable, non-optional, and it can increase every year.

According to an April 2026 Realtor.com analysis, the national median condo HOA fee is now $420 per month, up 29% from $325 in 2019. Meanwhile, 43.6% of homes currently listed for sale carry HOA fees, up from 34.3% in 2019. Condo buyers in particular have no way to shop around the HOA fee the way they can shop around a mortgage rate.

That fee is a second mortgage payment with no amortization schedule and no payoff date. Over 10 years at $420/month, you will pay more than $50,000 in dues on top of your mortgage principal. And unlike a mortgage, the payment can go up without your consent.

What's Driving the Surge

The 29% increase since 2019 isn't arbitrary. Five structural forces are pushing HOA fees higher, and most of them are not going away.

1. Insurance Premiums

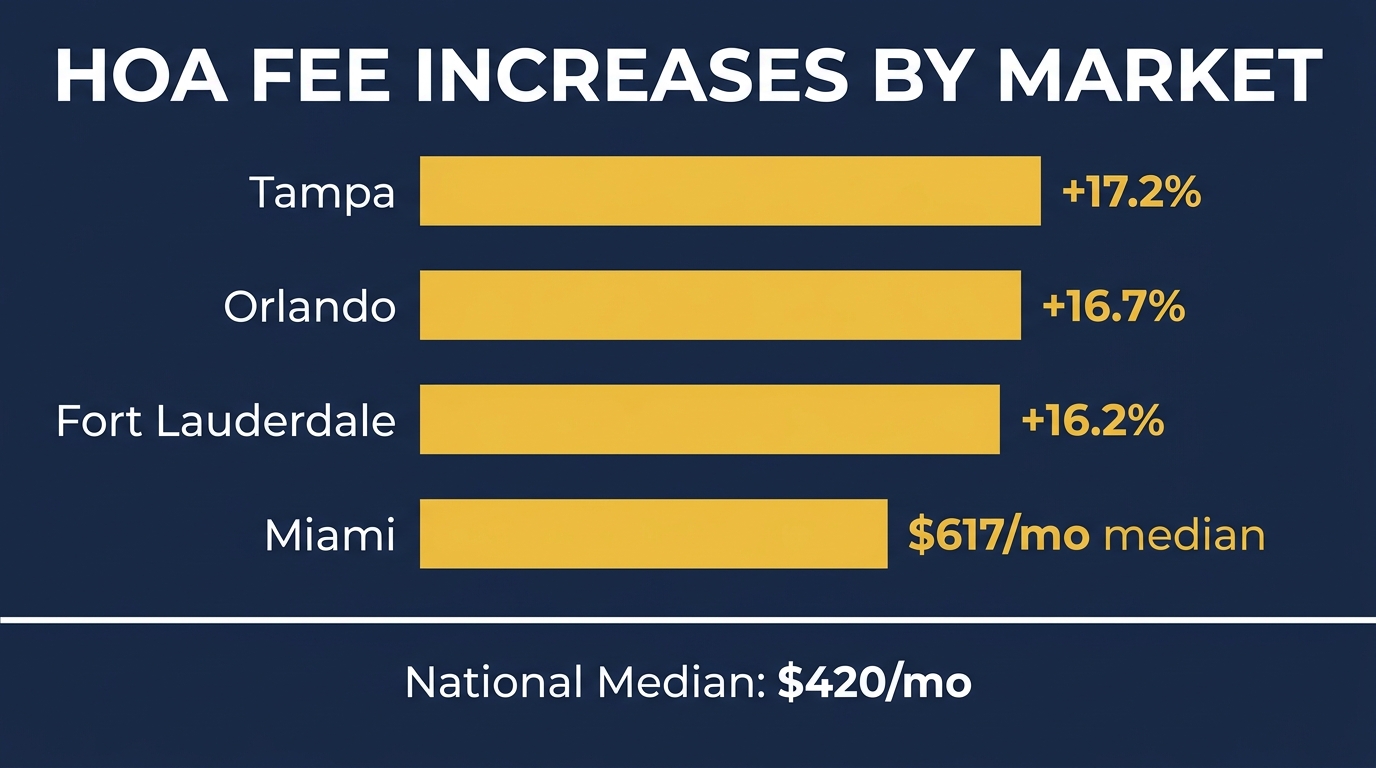

HOA master policies cover the building structure, common areas, and liability. In Florida, insurance premiums have risen to 2.5 times the national average, and several major carriers have exited the market entirely. When the HOA's renewal comes in 40% higher than last year, that increase gets passed directly to unit owners through higher dues. In high-risk coastal markets like Miami ($617/month median) and Fort Lauderdale, insurance costs have become the single largest driver of recent fee increases.

2. Deferred Maintenance Catching Up

For years, boards held fees artificially low to avoid unhappy owners. That strategy defers costs but does not eliminate them. When a roof hits 25 years, when an elevator needs a full rebuild, when a parking garage requires structural repairs, those bills arrive regardless of what the reserve fund contains. Buildings that kept fees low for a decade are now catching up all at once.

According to Association Reserves, which has analyzed more than 100,000 reserve studies since 1986, 74% of community associations are underfunded. The correction is showing up in fee increases and special assessments.

3. Post-Surfside Structural Mandates

The 2021 Champlain Towers collapse triggered sweeping changes in Florida and increased scrutiny nationally. Florida's milestone inspection requirements and SIRS mandates require buildings to quantify deferred structural maintenance and fund it properly. Reserve waivers are banned for most condos. Buildings that had been waiving reserves for 20 years can no longer do so. The result: mandatory fee increases to fund reserves that were legally avoided for decades.

4. Inflation on Labor and Materials

Concrete, steel, roofing materials, and skilled trades all cost significantly more today than they did in 2019. A roof replacement that cost $350,000 in 2019 may cost $500,000 or more today. Reserve studies use current replacement costs, so those inflated numbers flow directly into the required reserve contribution, which flows into monthly dues.

5. Years of Below-Market Fees Now Correcting

Many HOA boards, particularly in older buildings, set dues at levels that covered operating expenses but not adequate reserve contributions. That worked while the building was young. As major systems age simultaneously, the gap between what is collected and what is needed becomes impossible to ignore. The correction is abrupt: fees that should have risen 3-4% annually for 15 years are instead rising 20-30% in a short window.

When High Fees Are Actually a Good Sign

A high HOA fee is not automatically a problem. The question is where the money is going.

A building charging $600/month with 30% going to reserves ($180/month per unit) is in a fundamentally different position than a building charging $400/month with 5% going to reserves ($20/month per unit). The first building is funding its future. The second is deferring it.

High fees become a good sign when they indicate:

- Reserves are adequately funded: 70%+ percent funded is the healthy benchmark per Association Reserves

- No pending special assessments or history of frequent ones

- A recent reserve study showing strong percent funded and no major components at Remaining Useful Life = 0

- Low delinquency rate: below the 15% Fannie/Freddie warrantability cap for units 60+ days past due (5-8% is the typical healthy range per CAI)

As we covered in Are Low HOA Fees a Red Flag?, a $150/month fee on a building with aging infrastructure is not a deal. It is a deferred liability arriving at your doorstep after closing. The full HOA financial health picture requires looking beyond the dues line.

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →What Buyers Should Check Before Closing

The fee itself tells you the cost. The documents tell you whether it's going up.

Every $100/month in HOA fees removes roughly $16,000 in purchasing power when calculated against current 30-year mortgage rates. Before closing on a condo, verify these five things about the fees you're agreeing to pay.

1. Fee History: The 3-Year Trend

Request the last three years of HOA budgets and look at the dues line. A building raising fees 3-5% annually is managing costs responsibly. A building that held fees flat for four years and is now proposing a 25% increase is signaling financial stress. The trend matters more than the current number.

2. Reserve Contribution Rate

Find the line item labeled "Reserve Contribution" or "Reserve Fund Allocation" in the current operating budget. Divide it by the total budget. Fannie Mae and Freddie Mac currently require at least 10% of the annual budget to go to reserves. That threshold rises to 15% effective January 4, 2027. A building at 6-8% is underfunding its reserves every year and will likely fail the Fannie/Freddie standard after that date.

3. Reserve Study Percent Funded

The reserve study executive summary shows a "percent funded" number. This measures how much money the building actually has versus how much it should have for future repairs. Below 30% is a serious red flag. Below 50% is worth investigating carefully. See the guide to percent funded thresholds for a full breakdown.

4. Pending or Approved Special Assessments

Sellers are required to disclose pending special assessments, but "pending" does not always mean formally approved. Read at least 12 months of board meeting minutes and search for mentions of upcoming projects, structural issues, or reserve shortfalls. If the board has been discussing a $2 million elevator replacement for six months but has not voted yet, that assessment could land after you close.

Always require an estoppel certificate before closing. Florida condominium associations must provide estoppel certificates within 10 business days of a written request under Florida Statute §718.116. Other states have similar but varying requirements. The estoppel certificate lists all current and pending assessments.

5. Compare to Regional Median for Building Type and Age

A $420/month fee in Miami is below the market median. A $420/month fee in a mid-sized Midwestern city is significantly above it. Context matters. Compare the fee to similar buildings in the same market: same age, same unit count, similar amenities. A fee that seems high nationally may be normal for that market, or low enough to suggest underfunding.

For a deeper look at reading the reserve study specifically, see How to Read a Reserve Study in 5 Minutes. For what to do when the numbers look bad, see HOA Special Assessment Red Flags.

Frequently Asked Questions

How much have HOA fees increased in recent years?

According to Realtor.com's April 2026 analysis, the national median condo HOA fee is $420 per month, up 29% from $325 in 2019. Some markets have seen even larger recent increases: Tampa is up 17.2%, Orlando up 16.7%, Fort Lauderdale up 16.2%. Miami's median has reached $617 per month, nearly 50% above the national figure.

How do HOA fees affect purchasing power?

Every $100 per month in HOA fees removes roughly $16,000 in purchasing power at current 30-year mortgage rates. That is because $100/month equals $1,200/year. At current rates, that annual cash flow supports approximately $16,000 in additional mortgage principal. Buyers who treat HOA fees as a separate line item rather than part of their total monthly housing cost are systematically misjudging affordability.

Are high HOA fees always a bad sign?

Not at all. A high fee with strong reserve funding: 70%+ percent funded, 15-25% of budget going to reserves, no pending assessments. That combination is actually reassuring. It means the building is maintaining itself properly and is unlikely to surprise owners with a large special assessment. The real concern is a high fee combined with poor reserve funding, which suggests the board is raising dues reactively rather than proactively.

Can an HOA raise fees without owner approval?

Most HOA governing documents allow the board to raise dues up to a set percentage, often 10-20% per year, without a member vote. Increases beyond that threshold typically require a member vote. The specific limit is in the CC&Rs or bylaws under the assessment or dues section. Some states also impose statutory caps. Check the governing documents for your specific building before assuming the board's authority is limited.

What percentage of home listings now have HOA fees?

According to Realtor.com's April 2026 data, 43.6% of homes currently listed for sale carry HOA fees, up from 34.3% in 2019. The share is significantly higher for condominiums and townhomes, where HOA membership is nearly universal. Buyers in these categories should treat the HOA fee as a core component of their monthly housing cost, not an add-on.

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

Sources & References

- Realtor.com Research - HOA Fee Data (April 2026) - Median condo fee $420/month, 29% increase since 2019, 43.6% of listings with HOA fees

- Bankrate - HOA Fees: What You Need to Know - Purchasing power impact of HOA fees on mortgage capacity

- Association Reserves - Three Quarters of Associations Are Underfunded - 74% underfunding rate from 100,000+ reserve studies (1986–2025)

- CondoApproval.com - Fannie Mae & Freddie Mac Condo Reserve Requirements Guide - 10% current minimum rising to 15% on January 4, 2027

- Florida Statute §718.116 - Assessments; Liability; Estoppel Certificates - 10 business day requirement for estoppel certificate delivery

- NAIC - Homeowners Insurance Report (2024) - Florida insurance premiums relative to national average

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. HOA fee trends, disclosure requirements, and reserve funding rules vary by state and governing documents. Consult a qualified real estate attorney or financial advisor before making decisions based on HOA financial data.