In This Guide

Special assessments of $5K–$400K per unit hit without warning if you don't know what to look for. Five document patterns predict them before they're announced.

The $50K Surprise Nobody Saw Coming

Most buyers find out about pending special assessments after closing. The warning signs were in the documents the whole time.

In June 2024, a couple closed on a condo at Toscana in Highland Beach, Florida. Five months later, they received a notice: $91,000 due for elevator replacement. The catch? Their seller had known about the planned $7 million assessment since March 2024, three months before closing. The board had discussed it in meeting minutes. The seller said nothing.

They sued. But the legal fight doesn't undo the financial shock. The assessment was already levied. The money was already owed.

This isn't rare. Association Reserves, which has analyzed more than 100,000 reserve studies since 1986, found that 74% of community associations are underfunded, meaning most buildings are quietly running out of money before a major repair arrives.

The good news: the warning signs are almost always in the documents. A reserve study, meeting minutes, and CC&Rs will tell you what's coming, if you know what to look for.

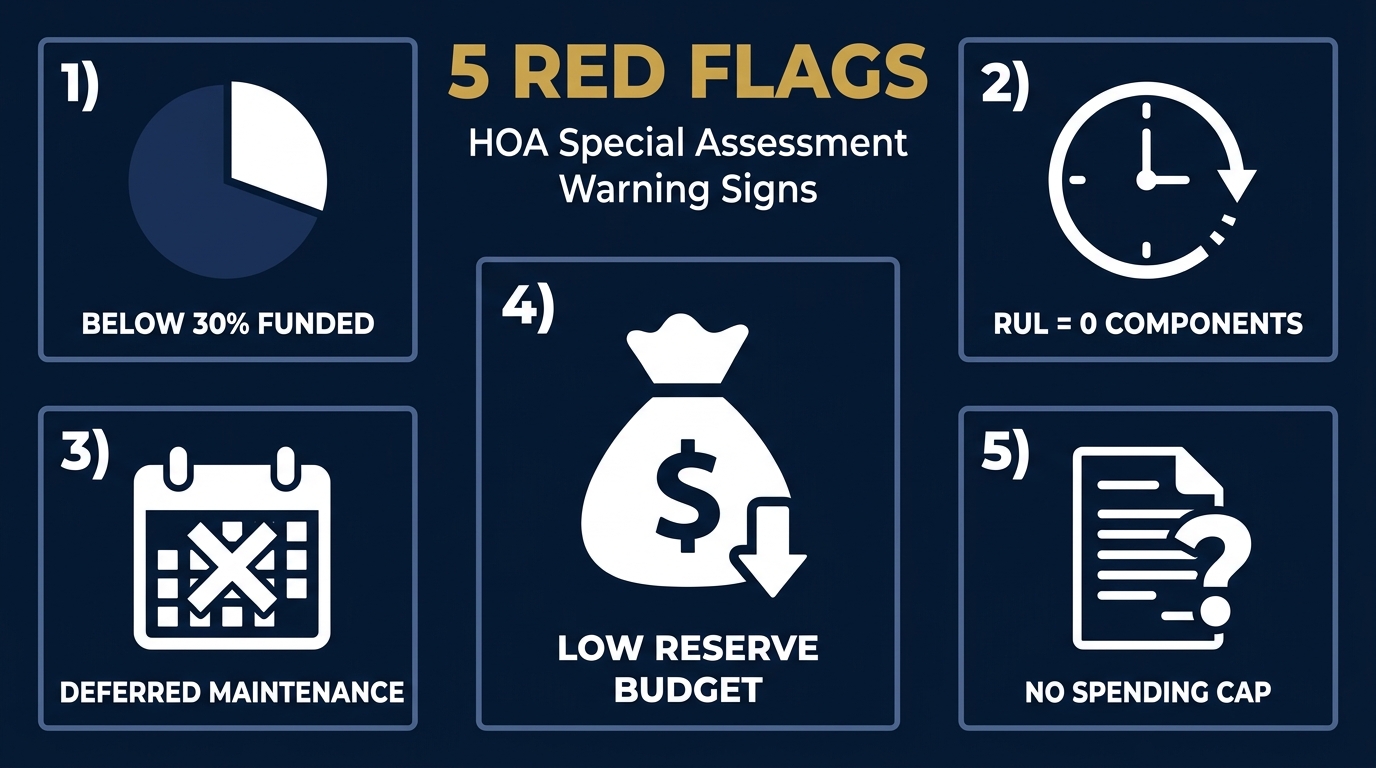

5 Red Flags Hidden in the Documents

These five patterns (across the reserve study, meeting minutes, budget, and CC&Rs) consistently precede special assessments.

Red Flag #1: Reserve Study Percent Funded Below 30%

The percent funded metric measures how much money the HOA actually has in reserves compared to what it should have. According to Association Reserves, the industry's largest reserve study firm:

- 70%+ funded: Strong. Low special assessment risk.

- 30–70% funded: Fair. Medium risk. Watch for trends.

- Below 30% funded: Poor/critically underfunded. High risk of special assessments and deferred maintenance.

A building at 18% funded with a major repair due in three years isn't a yellow flag. It's a near-certainty that owners will face an assessment. The money isn't there.

Red Flag #2: 3 or More Reserve Study Components at RUL = 0

Every reserve study includes a component list, a table of every major building element (roof, elevator, HVAC, plumbing, parking surfaces, pool equipment) with its expected useful life and Remaining Useful Life (RUL).

RUL = 0 means the component is past due for replacement. One expired component is a yellow flag. Three or more is serious. A single major component (a roof, an elevator, or a central HVAC system) can generate a $50K–$400K per-unit assessment on its own.

Red Flag #3: Meeting Minutes With Repeated Deferred Maintenance

Board meeting minutes are a paper trail of what the board knew and when. Look through two years of minutes and search for the same maintenance items appearing over and over (voted down, tabled, deferred, or ignored).

This pattern means two things: the problem is real (it keeps coming up), and the board hasn't funded a fix (it keeps being deferred). That deferred work doesn't disappear. It compounds, gets more expensive, and eventually becomes an emergency assessment.

Red Flag #4: Reserve Contribution Below 10% of Annual Budget

Fannie Mae and Freddie Mac currently require HOAs to allocate at least 10% of their annual budget to reserves as a condition of mortgage eligibility (rising to 15% effective January 4, 2027). A building contributing less than 10% is actively underfunding its reserve account every year and may already be non-warrantable.

The real healthy range is 15–40% of the operating budget, with an industry average around 25%. A building contributing 6–8% every year is slowly building toward the moment when a major repair arrives with no money to pay for it.

Red Flag #5: CC&Rs With No Cap on Board Assessment Authority

This one surprises most buyers. Your CC&Rs determine whether the board can levy a large special assessment without a homeowner vote.

Some CC&Rs include strong protections: "No special assessment exceeding $500 per unit may be levied without approval of two-thirds of the membership." Others say nothing, giving the board unlimited authority to levy any amount it deems necessary.

State law sometimes fills the gap. In California, Civil Code Section 5605 caps board authority at 5% of annual budgeted expenses without a vote. But protections vary widely by state, and many states have no cap at all. If the CC&Rs are silent and your state has no limit, the board has unilateral power.

Where to Find Each Red Flag

Each red flag lives in a specific document. Here's exactly where to look and what to search for in each.

| Red Flag | Document | Search Term / Location |

|---|---|---|

| Percent funded below 30% | Reserve study | Cover page or executive summary. Ctrl+F "percent funded" or "funding level" |

| RUL = 0 components | Reserve study | Component list appendix. Look for "RUL" column; count entries showing 0 or negative |

| Deferred maintenance | Board meeting minutes (last 2 years) | Ctrl+F "table," "defer," "postpone," "no action." Flag any item appearing in 2+ meetings |

| Low reserve contribution | Annual budget | Find "Reserve Contribution" or "Reserve Allocation." Divide by total budget. Below 10% is a lender flag |

| Board assessment authority | CC&Rs | Ctrl+F "special assessment," "board authority," "vote required." Look for dollar caps or member vote requirements |

State laws vary on how quickly HOAs must provide documents: California requires 10 days under Civil Code §4530, while Florida condos require 10 business days under Fla. Stat. §718.116(8)(a) (estoppel certificate). Ask your agent to request the full document package before you make an offer, not after. Once you're under contract, the clock is already ticking.

For a deeper guide on reading the reserve study specifically, see How to Read a Reserve Study in 5 Minutes.

What to Do When You Find Red Flags

Finding red flags doesn't mean walking away. It means negotiating with accurate information. Here's how.

One red flag is worth noting. Two is worth quantifying. Three or more (especially percent funded below 30%, multiple RUL=0 components, and a history of deferred maintenance) signals that a major assessment is likely inevitable. At that point, the question isn't whether an assessment is coming but who will pay it.

Option 1: Request a Price Reduction

If the reserve study shows a building that's 20% funded with a roof at RUL=0, you can estimate the likely assessment (get a contractor estimate or use comparable building data) and negotiate a price reduction equal to your share. This is your cleanest option: the discount bakes in the expected cost.

Option 2: Seller Credit at Closing

Instead of a price reduction, the seller credits you a set amount at closing. Functionally similar, but easier for some loan structures. Make it specific: "Seller to provide $25,000 credit for anticipated reserve shortfall based on reserve study dated [date]."

Option 3: Escrow Holdback for Approved Assessments

If a special assessment is already approved but the final per-unit amount isn't confirmed, an escrow holdback protects you. The seller's share is held in escrow until the amount is finalized, then paid out.

The Walk-Away Rule

If you find three or more of the red flags listed above (especially in combination with a board that has consistently deferred major maintenance), the financial risk is structural. No price reduction fully compensates for a building heading toward $100K+ assessments with no money to cover them. Walking is rational.

Make sure your purchase contract includes a contingency for satisfactory HOA document review, and require the seller to provide an estoppel certificate listing all pending or approved assessments. In the Toscana case described above, the seller's contract included a representation that no pending assessments existed, a false statement that became the basis of the lawsuit.

For more on who pays when a special assessment lands at closing, see Who Pays the HOA Special Assessment at Closing?

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Frequently Asked Questions

What is the biggest red flag for a pending HOA special assessment?

A reserve study showing percent funded below 30% is the single strongest predictor. Below 30%, the building has less than one-third of what it needs to cover future repairs, and any major system failure becomes an immediate special assessment. Combine that with multiple RUL=0 components and the risk becomes near-certain.

How common are HOA special assessments?

Very common. Association Reserves, which has analyzed more than 100,000 reserve studies since 1986, found that 74% of community associations are underfunded. When reserves are inadequate, any major repair becomes a special assessment. This is why document review before closing matters so much.

Can a HOA board levy a special assessment without a homeowner vote?

It depends on the CC&Rs and state law. Some CC&Rs require a member vote for assessments above a set dollar threshold. California's Civil Code Section 5605 caps board authority at 5% of annual budgeted expenses without a vote. Many states have no statutory cap, leaving the answer entirely in the governing documents. If the CC&Rs are silent and your state has no limit, the board may be able to levy any amount without member approval.

What does RUL = 0 mean in a reserve study?

RUL stands for Remaining Useful Life. RUL = 0 means the component is at or past its expected replacement date. It doesn't guarantee immediate failure, but it does mean the HOA should be actively planning and funding a replacement. Three or more components at RUL = 0 (especially major items like roofs, elevators, or HVAC systems) signals serious deferred maintenance risk.

What should I do if I find multiple red flags during due diligence?

Start by quantifying the likely assessment: get a contractor estimate for the deferred work and calculate your unit's share. Then decide whether to negotiate a price reduction, request a seller credit, or walk away. Always require the seller to provide an estoppel certificate listing all pending or approved assessments before closing. If three or more red flags are present, the financial risk may be structural; no discount fully covers a building heading toward a six-figure assessment.

Don't go into a closing blind

Upload the reserve study, CC&Rs, or meeting minutes and get an instant risk report, built on analysis of 1,900+ HOA documents. No signup required.

Related Articles

Sources & References

- Association Reserves: Three Quarters of Associations Are Underfunded 74% underfunding rate from 100,000+ reserve studies (1986–2025)

- Association Reserves: Reserve Study Basics Percent funded thresholds and funding level benchmarks

- Capital Reserve Analysts: What Is Percent Funded? Funding level risk categories

- Siegfried Rivera: Condo Sellers Must Tell Buyers About Special Assessments Friedlander v. Kaplan (2024): undisclosed $91K elevator assessment

- Boston City Properties: Harbor Towers 2007 Assessment $75.6M assessment, $70K–$400K per unit

- Nolo: When HOA Associations Can Impose Special Assessments Board authority, CC&R governance

- LS Carlson Law: HOA Special Assessment Limits in California California Civil Code Section 5605 board authority cap

- CondoApproval.com: Fannie Mae & Freddie Mac Condo Reserve Requirements Guide 10% current minimum (rising to 15% Jan 4, 2027), reserve study waiver conditions

- Neighborhood.online: How Much Should Your HOA Have in Reserves? 15–40% healthy contribution range guidance

- Redfin: Who Pays for a Special Assessment at Closing? Buyer/seller negotiation and estoppel guidance

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. Special assessment rules, board authority limits, and disclosure requirements vary significantly by state and governing documents. Consult a qualified real estate attorney before making decisions based on HOA documents.