In This Guide

Most condo buyers skip the financials and read the CC&Rs. The financials are where the next special assessment is already written down. Eight lines, thirty minutes, no accounting degree required.

A typical condo resale package runs sixty pages, and somewhere in the middle is a stack the buyer's agent will skim past with the words "have your accountant look at this." That stack is the HOA's financial statements. It is also the single best forecast of whether you are about to inherit a six-figure special assessment.

Boards know this, which is why mature associations often present financials in a format that is technically complete and practically unreadable. The 217-unit Cricket Club in North Miami carried no reserves on the books for years before owners were billed roughly $134,000 per unit in 2024. Champlain Towers South had a March 2020 reserve study showing $706,000 on hand against $10.3 million recommended (6.9% funded), thirteen months before the board approved a $15 million assessment averaging $110,000 per owner. Both numbers were sitting in the financials before the bills landed.

What follows is the buyer's read. Eight lines across three documents. No accounting jargon, no spreadsheet skills required.

Why Financial Statements Are the Most Underread Document in Your Packet

Reserve studies estimate. Meeting minutes describe. Financial statements measure. They are the only document in the packet that has to balance to the penny.

Every other document in a resale package is narrative. The CC&Rs are rules. The reserve study is a forecast. The meeting minutes are a record of decisions made. None of them have to add up. The financials do.

That makes the financials the only document where a board cannot hide a problem with careful wording. Cash is cash, the AR aging is the AR aging, and the reserve fund balance either matches what the reserve study said it should be or it does not. We have linked our broader HOA Financial Health Guide for the strategic framework. This post is the line-by-line read for when the documents are sitting in your inbox and the offer deadline is Friday.

What You Should Receive (And What You Often Get Instead)

A complete HOA financial packet has six pieces under CIRA standards. Most resale packages include four. The two that go missing matter most.

The American Institute of Certified Public Accountants publishes the Audit and Accounting Guide for Common Interest Realty Associations, first issued in 1991 and codified to FASB Accounting Standards Codification Topic 972 effective July 1, 2009. The CIRA Guide is the industry standard for how an HOA's books are supposed to be presented. Under accrual basis with separate operating and reserve fund accounting, a complete packet contains:

- Balance sheet (assets, liabilities, fund balances) as of the most recent month or year-end

- Statement of revenue and expense (also called the income statement)

- Statement of changes in fund balances

- Reserve fund schedule (often a supplementary schedule)

- AR aging report showing 30/60/90/120+ day buckets

- Audit, review, or compilation report from a CPA, with footnotes

Many small associations (5-20 units) operate on a cash basis and produce only a check register and a year-end summary. That is not a deal-breaker, but it is information. Cash basis means no AR aging, no accrued liabilities, and reserves that are tracked through a separate bank statement instead of a fund balance. If the building you are looking at is small and self-managed and the financials are a one-page summary, ask for the bank statements for the reserve account and the most recent reserve study, and use those instead.

The Balance Sheet: Five Lines, Five Minutes

Five lines on the balance sheet matter: operating cash, reserve cash, AR, accrued liabilities, and fund balance separation. That is the buyer's read.

A balance sheet is two columns. Assets on one side, liabilities and fund balances on the other, totals equal. For a buyer, only five line items matter:

| Line | What it tells you | Red flag |

|---|---|---|

| Operating cash & investments | How much liquid cash is available for day-to-day expenses | Less than 2-3 months of operating expenses |

| Restricted reserve fund | Cash held for future capital projects (must be segregated from operating cash) | Reserve balance materially below the reserve study's recommended balance |

| Accounts receivable | Assessments owed by owners but not paid | AR > 5% of annual assessments, or rising trend year-over-year |

| Accrued liabilities | Bills the HOA owes but has not yet paid (payables) | Large or growing payables paired with low operating cash |

| Fund balance separation | Operating fund balance vs reserve fund balance, shown separately | No separation, or reserves "commingled" with operating cash |

Commingling is the one to flag aggressively. Under CIRA accounting and most state HOA statutes, restricted reserve cash is supposed to be held separately so that a board cannot quietly use it to plug operating shortfalls. When the balance sheet shows a single combined "cash" line with no reserve segregation, the question to ask is not whether something is wrong, but what.

The Income Statement: Find the Transfer-to-Reserves Line

Annual assessment income on top, vendor expenses in the middle, transfer-to-reserves at the bottom. The transfer line is the single most important number.

The income statement (or statement of revenue and expense) tracks one year of operations. Most buyers focus on the operating surplus or deficit at the bottom, which is the wrong line. The right one is the "transfer to reserves" or "reserve contribution" line, usually shown as an expense or a transfer below operating income.

Compare that transfer figure to two benchmarks. First, what the reserve study's funding plan recommends as the annual contribution. Second, the percentage of total assessment income that the contribution represents. Fannie Mae's Lender Letter LL-2026-03, issued March 18, 2026, requires lenders to confirm that established condo projects allocate at least 10% of the operating budget to reserves, rising to 15% effective January 4, 2027. Below 10% today, you are looking at a project that may not pass Fannie's warrantability check next year, which compresses your future buyer pool when you sell.

For more on what those Fannie thresholds mean for resale, see our breakdown of the 2026 Fannie/Freddie condo rules.

The Reserve Fund Schedule: Does the Math Match the Reserve Study?

Opening balance plus contributions plus interest minus expenditures equals closing. Compare that closing balance to what the reserve study said it should be.

The reserve fund schedule is usually a one-page supplement showing how the reserve account moved over the year. It looks like this:

- Opening balance (start of year)

- Plus: contributions transferred in from operating

- Plus: interest earned

- Minus: capital expenditures (roof, elevator, paving, etc.)

- Equals: closing balance (end of year)

Two checks. First, does the closing balance match what the reserve study's funding plan said the reserves should be at this point in time? A material gap means the board is underfunding relative to what its own engineer recommended. Second, are the expenditures rolling against components the reserve study identified, or are they ad-hoc emergency repairs? Emergency repairs charged to reserves are how funded percentages collapse without a single "assessment" vote.

The industry framework, published by Association Reserves and used by most reserve study firms, classifies funding tiers as 0-30% weak, 31-70% fair, and 71-130% strong. Below 30% is the tier where deferred maintenance and surprise assessments become the norm. Our explainer on percent funded walks through the math.

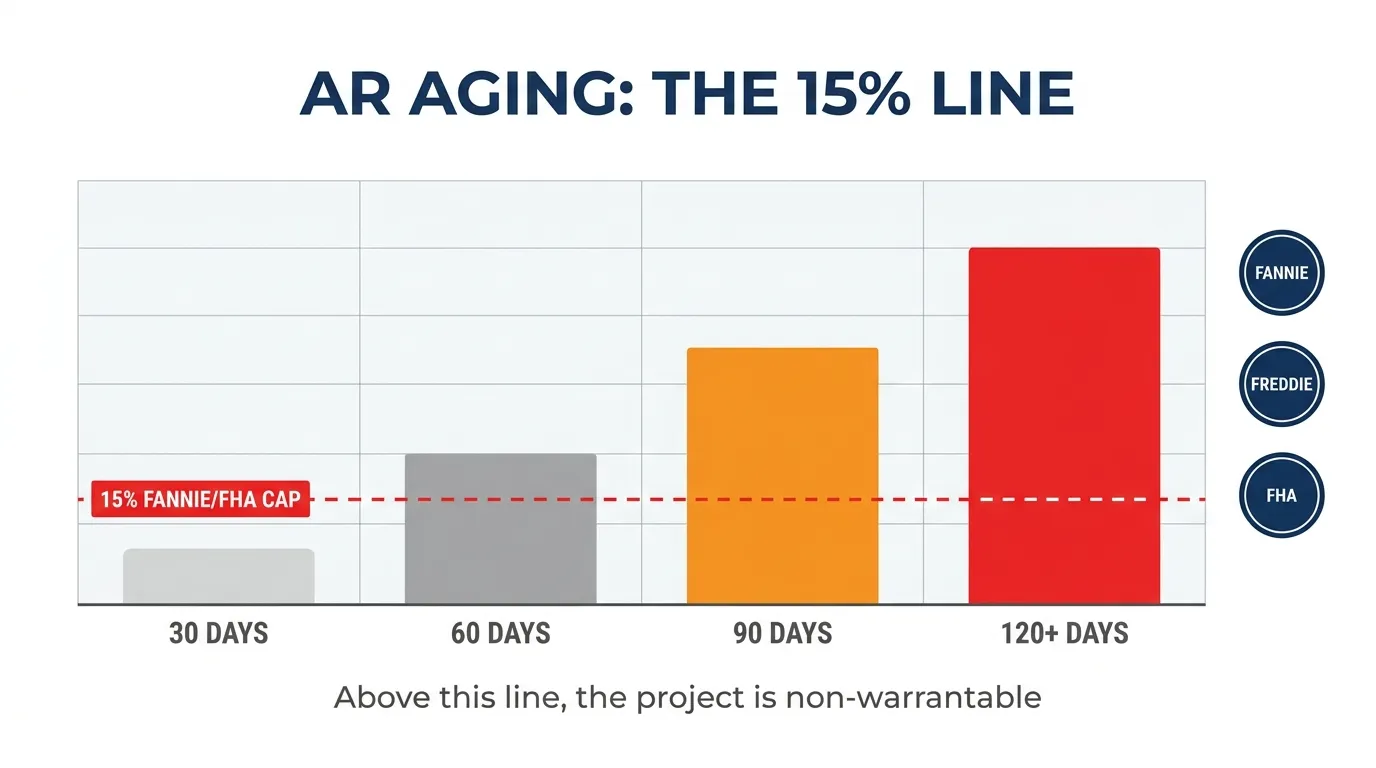

AR Aging: The 15% Threshold That Breaks Your Loan

FHA, Fannie, and Freddie all cap delinquency at 15% of units 60+ days past due. Above that line, the project is non-warrantable and your loan stalls.

The accounts receivable aging report breaks down assessment delinquencies into 30-day, 60-day, 90-day, and 120+-day buckets. For most buildings, the 30-day bucket is noise: owners traveling, autopay glitches, normal lag. The 60-day and longer buckets are the signal.

FHA condo approval rules cap the percentage of units 60+ days delinquent at 15%. Fannie Mae and Freddie Mac apply parallel thresholds for project warrantability, calculated separately for regular and special assessments. When a project crosses 15%, lenders cannot sell the loan to Fannie or Freddie, which means conventional financing is unavailable to your future buyer. FHA also reduces its required owner-occupancy threshold from 50% to 35% when delinquency is at or below 10%, so the cleaner the AR, the larger your future buyer pool.

For deeper context on this number, see our post on HOA delinquency rate and condo purchase.

Audit vs Review vs Compilation: What Level of CPA Assurance

Audit is the highest level. Review tests reasonableness. Compilation is just formatting. The cover letter says which one you have.

The cover page of the financials is signed by a CPA firm and identifies the engagement as one of three things:

- Audit. The CPA tests transactions, confirms balances with banks, and issues an opinion on whether the statements are fairly stated. Highest assurance.

- Review. The CPA performs analytical procedures and inquiries, but does not test transactions. Limited assurance.

- Compilation. The CPA assembles the statements from the HOA's books with no testing or assurance. The cover page typically says "no assurance is provided."

Several states tie the required level to association size. Florida Stat. §718.111(13) requires an audit at $500,000+ in annual revenue, a review at $300,000-$500,000, and a compilation at $150,000-$300,000. California Civ. Code §5305 sets a $75,000 gross income threshold for an annual review by a licensed CPA. If a building's revenue is well above its state's audit threshold and you are still seeing only a compilation, ask why.

Read the audit footnotes. Footnotes are where the auditor discloses contingent liabilities, pending litigation, related-party transactions, and reserve methodology. Many of the financial-statement red flags in the case studies below were sitting in audit footnotes years before they made the news.

Three Buildings Whose Financials Told the Story

Villas of Carillon disclosed a 20-year reserve waiver. Champlain's 6.9% funded was on the reserve schedule. Palm Bay's audit footnotes flagged the fraud.

Villas of Carillon, Feather Sound, Florida (165 townhomes, 2024)

The cleanest hero case for buyer-readable financials. The Villas of Carillon association disclosed, in plain English in association communications, a 20-year history of waiving the decision to fully fund Reserves. Owners were billed a special assessment averaging roughly $60,000 per unit in 2024. The entire board resigned. A buyer reading the prior years' financials would have seen a transfer-to-reserves line consistently below what the reserve study recommended, with the "waiver" framed as a budget decision in the footnotes.

Champlain Towers South, Surfside, Florida (136 units, 1981)

The first reserve study the association ever received arrived in March 2020 and showed roughly $706,000 on hand against about $10.3 million recommended for planned repairs, or 6.9% funded. By April 2021 cost had escalated past $16 million and the board approved a $15 million special assessment averaging roughly $110,000 per owner, plus a $12 million Valley National Bank loan. New angle for a financials read: the prior years' income statements would have shown effectively no "transfer to reserves" line at all, because the operating budget was consuming all assessment income. Reserve fund balance and reserve study recommendation were never reconciled in the financials before the structural report landed.

Palm Bay Yacht Club, Miami, Florida (235 units)

A 235-unit Miami tower billed owners a $48 million assessment for 40-year recertification work. Owners hired their own engineer who put the figure closer to $23 million, then sued. On December 10, 2025 a jury awarded owners $6.3 million ($5.8 million against South Florida Construction Management, plus $550,000 against D&R Roofing) for mismanagement and construction fraud. The financial-statement signal here was unusual reclassifications: $4 million in Hurricane Irma insurance proceeds with no clear restricted-fund treatment, and $2.5 million labeled as "emergency" work that the audit footnotes did not specifically describe.

For more buildings where reserves told the story, see our post on HOAs whose reserves hit 0%.

State Law: When You Get the Financials, And What You Can Do With Them

Most states require the seller to deliver financials in the resale package. Several give a 3-7 day right to cancel after receipt. The window is short.

State law on buyer access to HOA financials varies, but the high-volume condo states have similar mechanics: you receive the package, the clock starts, and you have a defined window to cancel without penalty.

| State | Statute | Cancellation window | Fee cap |

|---|---|---|---|

| Florida | §718.503 (resale) + §718.111(13) (audit thresholds); HB 1021 (Jul 1, 2024) added SIRS to resale | 3 business days post-receipt (§718.503(2)(a)); estoppel 10-business-day deadline | Estoppel: $299/$179/$119 |

| California | Civ. Code §4525 + §5300 (annual budget) + §5305 (CPA review at $75K) | Contract-driven (no statutory rescission) | No statutory cap |

| Texas | Prop. Code §82.157 (condo) / §207.003 (HOA) | 6 days post-receipt (condo) | $375 + $75 update (HOA only) |

| Washington | RCW 64.90.640 (WUCIOA, all CICs since Jan 1, 2026) | 5 days | $275 |

| Virginia | §55.1-1990 / §55.1-1991 (Va. Condo Act, 2024 amendments eff. Jul 1, 2024) | 3 days post-receipt; 14-day deemed-unavailable rule | Statutory cap (varies) |

| Colorado | CRS 38-33.3-317 (records access) | No statutory rescission; 30-day records production | $50/day after day 11, capped $500 |

| Massachusetts | c. 183A §10 (annual financial report) + §6(d) (closing certificate) | No statutory rescission | No statutory cap |

| Illinois | 765 ILCS 605/22.1 (resale disclosure) | No statutory rescission | No statutory cap |

| Arizona | A.R.S. §33-1258 / §33-1810 | 10-business-day records production | $0.15/page copy cap |

| New York | BCL §624 (annual balance sheet on request); custom resale practice | Contract-driven | No statutory cap |

The cancellation windows are real and short. Texas gives a condo buyer six days from receipt, Washington five, Florida and Virginia three. If the financials disclose a problem, the time to act is during that window, not after closing. Treat the day you receive the resale package as day zero.

The 30-Minute Read

One balance sheet, one income statement, one reserve schedule, one AR aging, one audit cover page. Eight numbers. Thirty minutes.

Open the balance sheet. Confirm reserves and operating cash are shown separately. Note operating cash, restricted reserve fund balance, AR, and accrued liabilities. Five minutes.

Open the income statement. Find the transfer-to-reserves line. Calculate it as a percent of total assessment income. Below 10% is the Fannie threshold today; below 15% is the threshold effective January 4, 2027. Five minutes.

Open the reserve fund schedule. Compare closing balance to what the reserve study's funding plan said reserves should be at this point in time. A gap is a future shortfall. Ten minutes.

Open the AR aging. Compute the percent of units 60+ days delinquent. Above 15% breaks Fannie/Freddie/FHA financing. Three minutes.

Open the audit cover page. Audit, review, or compilation. Read the footnotes for litigation, related-party transactions, and the reserve methodology. Seven minutes.

That is the read. If anything failed the threshold, you have a question for the seller, the listing agent, or the HOA management company before the cancellation window closes.

Frequently Asked Questions

What is the most important line item in HOA financial statements for a buyer?

The transfer-to-reserves line on the income statement, expressed as a percent of total assessment income. Fannie Mae LL-2026-03 (March 18, 2026) requires lenders to confirm at least 10% of operating budget is allocated to reserves, rising to 15% on January 4, 2027. Below 10% today is a project that may fail warrantability when you sell.

What does it mean when an HOA balance sheet does not segregate reserves?

Under the AICPA CIRA Audit Guide and most state HOA statutes, restricted reserve cash is supposed to be held separately from operating cash so the board cannot use it for routine expenses. A balance sheet showing a single combined cash line with no reserve fund segregation is a sign the association is either commingling funds or has so little in reserves that segregation is moot. Both are buyer concerns.

What delinquency percentage makes a condo non-warrantable?

15% of units 60+ days past due on assessments breaks FHA condo approval and parallels Fannie Mae and Freddie Mac project-eligibility thresholds. Above that line, conventional financing is unavailable, which compresses the buyer pool when you resell. FHA also reduces required owner-occupancy from 50% to 35% when delinquency is at or below 10%.

Is a compilation as reliable as an audit?

No. A compilation is a CPA-formatted assembly of the HOA's books with no testing and no assurance. A review involves analytical procedures and inquiries (limited assurance). An audit tests transactions and confirms balances with third parties (highest assurance). Florida Stat. §718.111(13) requires an audit at $500K+ in annual revenue. If a building well above its state threshold is producing only a compilation, ask why.

How fast does a buyer have to act after receiving the resale package?

It depends on state law. Texas gives a condo buyer six days post-receipt to cancel, Washington five, and Florida and Virginia three business days under §718.503(2)(a) and §55.1-1990 respectively. California is largely contract-driven with no statutory rescission window for established condos. The cancellation window is the practical deadline for raising any issue the financials surface.

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

- HOA Financial Health: The Complete Guide for Condo Buyers

- HOA Meeting Minutes: 5 Patterns That Predict Your Next Special Assessment

- What Happens When HOA Reserves Hit 0%? Real Cases from 2025-2026

- How to Read an HOA Reserve Study

- HOA Delinquency Rate and Condo Purchase

- Fannie/Freddie 2026 Condo Rules: What Buyers Need to Know

Sources & References

- Fannie Mae Lender Letter LL-2026-03 (March 18, 2026) — Reserve and delinquency thresholds for condo project eligibility

- AICPA Audit and Accounting Guide for Common Interest Realty Associations — CIRA framework, FASB ASC 972

- Association Reserves: Percent-Funded Tiers — Industry tier framework (0-30 weak, 31-70 fair, 71-130 strong)

- CNN: Surfside condo finances — Champlain Towers reserves and assessment timeline

- Bay News 9: Villas of Carillon special assessment — Reserve waiver disclosure and board resignation

- Biscayne Bay Tribune: Palm Bay Yacht Club $6.3M jury verdict

- Fla. Stat. §718.111 (financial reporting + records access)

- Cal. Civ. Code §5305 — CPA review threshold

- RCW 64.90.640 — Resale certificate, fee cap, cancellation window

- HUD FHA Condo Approval rules — 15% delinquency cap and owner-occupancy thresholds

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, accounting, or real estate advice. Statute citations and regulatory thresholds are current as of publication and may change. Reserve and delinquency rules from Fannie Mae, Freddie Mac, and FHA are subject to lender overlays. Consult a qualified real estate attorney, CPA, or mortgage professional for guidance specific to your situation.