In This Guide

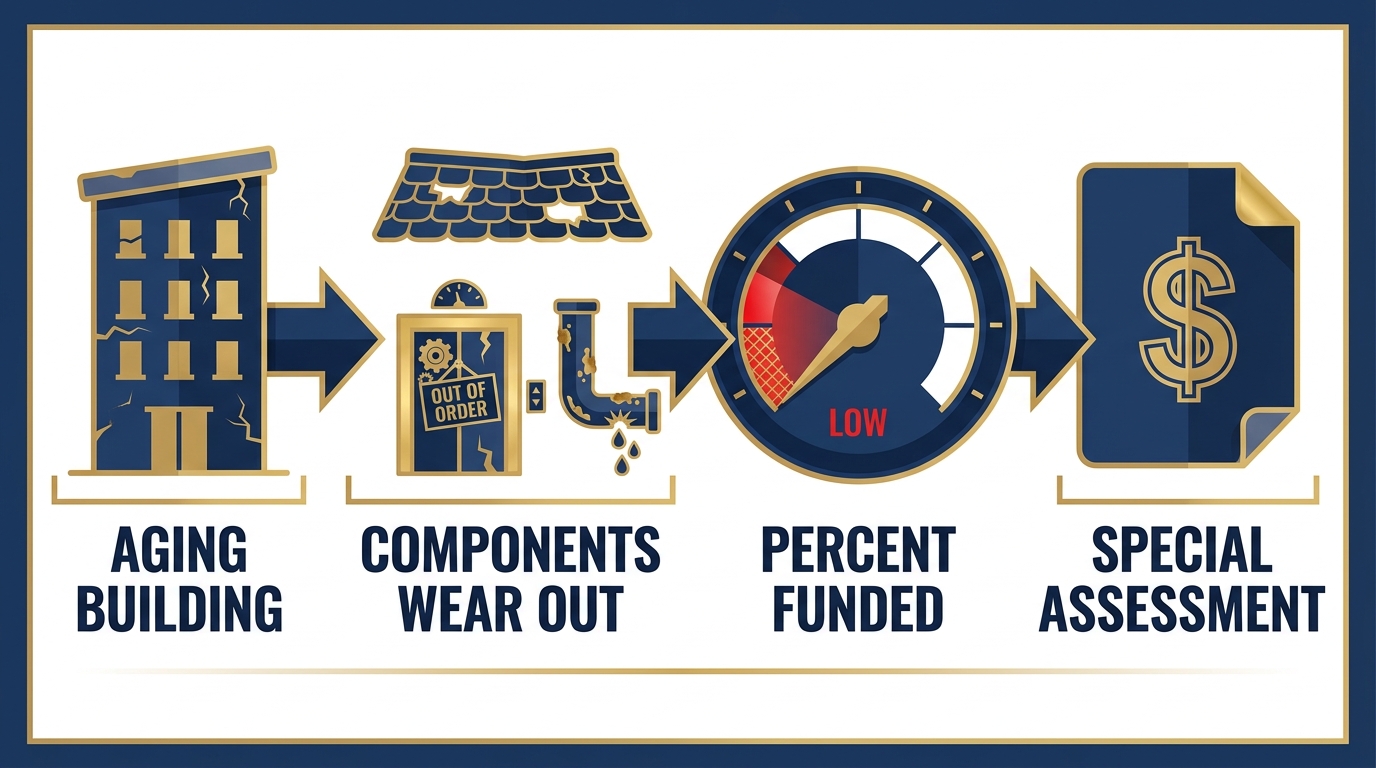

A condo's age matters because it puts a clock on every major system, from the roof and plumbing to the elevators and the concrete itself, and because a wave of post-Surfside laws now forces older buildings to inspect their structure and fully fund their reserves. Age alone does not sink a purchase. A well-run 40-year-old building can be a safer buy than a neglected 15-year-old one. What separates them is in the paperwork: the reserve study, the milestone or engineering report, the meeting minutes, and the special-assessment history. Read those, and a building's real condition stops being a mystery.

You find two condos in the same price range. One went up in 2015, the other in 1984. The older one has more space, a better location, lower asking price. On a walkthrough it looks fine, maybe even charming. It is easy to treat the build year as a footnote, a line on the listing next to the square footage. But a building's age is not a cosmetic detail. It is the single best predictor of what is about to break, what it will cost to fix, and whether the association has quietly been setting money aside for the bill.

The problem is that age tells you where to look but not what you will find, and the two buildings that share a birth year can be in wildly different shape. The only way to tell them apart is to read what the association has written down about its own condition. This guide explains why age drives risk, what the new inspection and reserve laws require of older buildings, and exactly which documents reveal whether a given older condo is a bargain or a liability waiting for a vote.

Why a Condo's Age Is Really a Countdown

Every major building component has a useful life, and most of them run out somewhere between 15 and 30 years. Age tells you how close the bill is.

A condo building is a bundle of expensive systems, and each one wears out on its own schedule. Reserve-study professionals track these as useful life estimates, and they cluster in a range that should get a buyer's attention. Roofs typically last about 15 to 25 years. Rooftop HVAC and boilers run roughly 15 to 20 years. Plumbing supply lines and fixtures land in a similar band. Elevator equipment usually needs a modernization at 20 to 25 years. That is why a professional reserve study projects a capital plan across a 30-year horizon: it is trying to catch every one of these before it fails.

| Component | Typical useful life | Why it matters to a buyer |

|---|---|---|

| Roof | ~15 to 25 years | One of the largest single line items in any reserve plan |

| HVAC / boilers | ~15 to 20 years | Common-area systems the association, not you, must replace |

| Plumbing supply / fixtures | ~15 to 20 years | Aging pipes drive leaks, water damage, and insurance claims |

| Elevator modernization | ~20 to 25 years | Six-figure projects in mid- and high-rise buildings |

| Structure, concrete, waterproofing | Decades, but degrades with exposure | The category that turned deadly at Surfside |

Useful-life numbers are reserve-study rules of thumb, not guarantees, and they vary by climate, construction, and maintenance. The point is not the exact year. The point is that a building crossing 20, 30, or 40 years is a building whose major systems are lining up to be replaced at roughly the same time. Whether that produces a smooth, pre-funded replacement or a panic special assessment depends entirely on whether the association saw it coming and saved for it. That answer lives in the reserve study, which we come back to below.

How Age Became a Legal Issue, Not Just a Maintenance One

The 2021 Surfside collapse turned aging condos from a maintenance question into a regulated one, driving new inspection and reserve laws nationwide.

For decades, deferred maintenance in an aging condo was treated as the association's business, something owners could vote to put off. That changed on June 24, 2021, when Champlain Towers South in Surfside, Florida, partially collapsed and killed 98 people. The building was roughly 40 years old, completed in 1981.

What made Surfside a turning point for buyers was not the age by itself but the paper trail behind it. A 2018 engineering report from Morabito Consultants had flagged major concrete deterioration and failed waterproofing that was "beyond its useful life," and estimated the repairs at more than $9.1 million. A March 2020 reserve analysis found the association held only a few hundred thousand dollars in reserves against a recommendation of roughly $10.3 million. By April 2021 the board had approved a remediation program of about $15 million, with per-unit assessments from about $80,000 for a one-bedroom to more than $336,000 for a penthouse. The structural work had not begun when the building came down. Federal investigators at NIST later found the collapse began at the connections between the garage columns and the pool deck, and that the original structural design did not meet the building code in force when it was built.

The lesson is not that old buildings fall down. They almost never do. The lesson is that the warning signs were written down years in advance, in exactly the documents a buyer can request, and that a building can carry a known, expensive, unfunded repair for years while looking perfectly normal from the sidewalk. Age is a risk amplifier: the older the building, the more of these compounding decisions sit in its history. In the aftermath, Florida and a growing list of other states stopped leaving those decisions entirely to owner votes.

Florida's Two Age-Driven Rules: Safety vs Funding

Florida requires two things of older condos: a milestone inspection asking if the building is safe, and a SIRS asking if reserves can pay for it.

Florida's response is the clearest example of how age became law, and it comes in two parts that buyers constantly confuse. They answer different questions.

The first is the milestone inspection under Fla. Stat. §553.899. It applies to condominium and cooperative buildings three habitable stories or more, and it is triggered by age. The statewide standard is an inspection by the time the building reaches 30 years old, with a local enforcement agency able to require it at 25 years where conditions such as proximity to salt water warrant. A licensed engineer or architect performs a Phase One visual inspection; if they find substantial structural deterioration, a more invasive Phase Two follows. After the first one, the building repeats the milestone every 10 years. This is a safety inspection. It asks whether the structure is sound.

The second is the Structural Integrity Reserve Study, or SIRS, under Fla. Stat. §718.112(2)(g). Every condo building three stories or higher had to complete one by December 31, 2025. It requires the association to study and reserve for a specific list of structural components, including the roof, load-bearing structure, fireproofing, plumbing, electrical, waterproofing and exterior painting, and windows and exterior doors, plus any other item whose deferred-maintenance or replacement cost tops $25,000 (raised from $10,000 by HB 913 in 2025). Crucially, for budgets adopted on or after December 31, 2024, owners can no longer vote to waive or underfund those structural reserves. This is a funding study. It asks whether the association has the money to pay for what the milestone inspection might find.

One building can pass the milestone and fail the SIRS, or the reverse. That is why they exist as two separate requirements, and why a buyer should ask for both. We cover the distinction in depth in our guide to reserve study versus SIRS report, and what a failed inspection actually means in the Florida milestone inspection explainer. Florida is also the state where the crunch is most visible, as our 2026 Florida condo crisis breakdown lays out.

What Older Buildings Face Outside Florida

Florida is strictest, but Maryland, New Jersey, California, and other states now impose their own inspection or reserve mandates on aging buildings.

Surfside pushed reform well beyond Florida. Buyers looking at older condos in other states should know whether a similar clock applies, because a pending inspection or a new reserve mandate can drive an assessment the same way Florida's rules do. Here is how several major markets compare.

| Jurisdiction | What it requires of older buildings | Trigger |

|---|---|---|

| Miami-Dade County, FL | Building recertification, then every 10 years | 30 years of age (shortened from 40 in 2022) |

| New Jersey | Periodic structural inspection plus a capital reserve study with mandatory funding (P.L.2023, c.214) | Load-bearing concrete, masonry, or steel condo/co-op buildings |

| Maryland | Statewide reserve study, with up to three years to reach the recommended funding level (HB 107, 2022) | All condominium associations |

| California | Inspection of balconies, decks, and other exterior elevated elements every 9 years (SB 326) | Wood-supported elevated elements more than 6 feet up |

| Chicago, IL | Recurring facade "critical examination" on a 4- to 12-year cycle by wall type | Buildings 80 feet or taller (roughly 7 to 8 stories) |

| Colorado | Written reserve-study and funding disclosure policy required (no mandated study schedule or funding level) | All common-interest communities |

Sources for the table: Miami-Dade 30-year recertification ordinance; New Jersey P.L.2023, c.214; Maryland Real Property §11-109.4 (HB 107); California SB 326; the Chicago facade ordinance; and Colorado's reserve-study disclosure policy requirement under CCIOA ( C.R.S. §38-33.3-209.5).

Two patterns are worth noting. First, some of these are triggered by age (Miami-Dade's 30-year clock) and some by construction type or height (New Jersey's load-bearing systems, Chicago's 80-foot rule), but in practice they all bite hardest on older stock, because older buildings are the ones with deteriorating concrete, wood, and facades. Second, several of these are new enough that many associations are only now completing their first inspection or study, which means the resulting assessment may not have hit the budget yet. If you are buying in one of these states, ask whether the required inspection or study has been done and what it found. Rules change and new states are added regularly, so confirm the current requirement locally rather than relying on a building's past compliance.

The Document That Reveals the Truth

The reserve study is the most revealing document on an older building. Check the percent funded and whether the plan funds the aging components.

If you read only one document on an older condo, make it the reserve study. It does two things at once. It inventories the major components and estimates how much useful life each has left, and it reports the association's percent funded, meaning how much cash it has on hand versus how much it should have by now. That single percentage is the closest thing to a health score an aging building has.

According to Association Reserves, which has analyzed more than 100,000 reserve studies, roughly 74% of associations are funded below the 70% mark that professionals consider strong. Its widely used percent-funded tiers put 0 to 30% funded in the "weak" band (high risk of special assessments and deferred maintenance), 30 to 70% as "fair," and 70% or above as "strong," where special assessments are rare. The math that should worry a buyer is the combination: an older building whose roof, elevators, and plumbing are all near the end of their useful life, sitting at 20% funded, is not a maintenance risk. It is a special assessment that has not been voted on yet.

This is exactly the analysis that gets skipped under a tight inspection deadline, because reading a reserve study by hand is slow and technical. Our guides on how to read a reserve study and what counts as a good percent funded walk through it, and the free reserve study analyzer pulls the percent funded and special-assessment risk in seconds.

Beyond the Reserve Study

Engineering reports, meeting minutes, assessment history, and the insurance line reveal whether an older building is managed or neglected.

The reserve study tells you whether the money exists. Four other documents tell you whether the association is actually staying ahead of its age.

- Engineering and inspection reports. The milestone, recertification, facade, or exterior-element report names specific defects and repair costs. Surfside's 2018 report is the cautionary example: the warning existed in writing for roughly three years. If an older building has one, read it and see whether the flagged repairs were funded and completed.

- Meeting minutes. Recurring mentions of leaks, concrete spalling, deferred repairs, or contested assessment votes are the pattern that precedes a crisis. The same repair item raised meeting after meeting with no action is a board postponing an aging-building problem.

- Special-assessment history. A pattern of large assessments in an older building signals chronic underfunding, not bad luck. One planned assessment can also disqualify financing, as the next section explains.

- Insurance status. Older and coastal buildings face rising master-policy premiums, high deductibles, and sometimes non-renewal. A fast-climbing insurance line in the budget, or a recent coverage gap, is an age-linked cost that compounds every year. Our breakdown of the condo insurance crisis covers how that reaches your mortgage.

Reading two years of minutes and a stack of engineering reports by hand is exactly the diligence that gets skipped under a contingency clock. The free meeting minutes analyzer surfaces deferred-maintenance discussions and assessment votes buried in the record, and for the full pre-offer routine, see how to review HOA documents.

Why Older Buildings Are Harder to Finance

Deferred maintenance, unsafe-condition findings, and thin reserves can make an older condo ineligible for a conventional loan.

Age becomes a financing problem when it shows up as deferred maintenance or a failed inspection. Under Fannie Mae's project eligibility rules, a condo project is ineligible for a conventional loan when it needs critical repairs, a category that includes significant deferred maintenance and any deficiency affecting the safety, soundness, structural integrity, or habitability of the project. A project that has received a directive from a regulatory or inspection authority to fix unsafe conditions, which is exactly what a failed milestone inspection produces, is also ineligible until the repairs are made and documented (Fannie Mae Selling Guide B4-2.1-03). Any current or planned special assessment must also be reviewed for acceptability, so an assessment triggered by an aging component can freeze financing for the whole building, not just the unit you want.

The reserve bar is also rising. Under Fannie Mae Lender Letter LL-2026-03, the minimum reserve contribution climbs from 10% to 15% of budgeted assessment income for loan applications dated on or after January 4, 2027, and the Limited Review shortcut for established projects is retired for applications dated on or after August 3, 2026. Older buildings that were already marginal on reserves are the ones most likely to fall below the new line. We cover the full set of changes in our 2026 Fannie and Freddie condo rules guide, and what a failed lender questionnaire feels like at the closing table in this explainer. One caveat worth keeping straight: the VA does not enforce these thresholds the way Fannie, Freddie, and FHA do, so a building that is non-warrantable for a conventional loan may still be financeable through a different program.

An Age-Based Due-Diligence Checklist

For any building past 20 years, pull the reserve study, the latest inspection report, two years of minutes, and the assessment history first.

Age is not a reason to walk away from a condo. It is a reason to ask for more paper. When a building is past about 20 years, and especially past 30, work through this list before you remove a contingency:

- Pull the reserve study and check the percent funded. Measure it against the 70% "strong" and 30% "weak" tiers, and cross-check the remaining useful life on the roof, elevators, and plumbing against the building's age.

- Ask for the latest inspection report. In Florida, that means the milestone inspection; elsewhere it may be a recertification, facade, or exterior-element report. Confirm what it flagged and whether those repairs were funded and done.

- Read 12 to 24 months of meeting minutes. Look for recurring deferred-maintenance items, contested assessment votes, and any mention of an upcoming inspection or study.

- Get the special-assessment history and current budget. A pattern of assessments, or a single large one on the horizon, is both a cost and a financing risk.

- Check the insurance line. Rising premiums, a high deductible, or a recent non-renewal are age-linked costs that will not go down.

- Confirm financeability with your lender early. If deferred maintenance, an unsafe-condition finding, or a planned assessment is in the file, verify the project is warrantable before you are deep into contract.

Anything that lands in the disqualifying-repair or major-assessment zone is worth an attorney's or engineer's eyes before you commit. For the complete pre-offer routine across every document type, see the complete condo buying checklist and our guide to reading an HOA budget for red flags.

Frequently Asked Questions

How old is too old for a condo?

There is no age at which a condo becomes automatically unsafe or unfinanceable. A well-managed 40-year-old building with a fully funded reserve and a clean inspection can be a better buy than a neglected 15-year-old one. What matters is not the build year but whether the association has inspected its structure, funded its reserves for the components that are aging out, and stayed ahead of deferred maintenance. Age tells you how carefully to read the documents, not whether to buy.

What documents should I review when buying an older condo?

Start with the reserve study and its percent funded, then get the most recent engineering or inspection report (in Florida, the milestone inspection and the SIRS), 12 to 24 months of board meeting minutes, the special-assessment history, the current budget, and the master insurance policy. Together these reveal whether the building's aging components are funded and maintained or whether an assessment is building. For condos three stories or higher in Florida, the milestone inspection and SIRS are now required by law.

At what age does a Florida condo need a milestone inspection?

Under Fla. Stat. §553.899, condominium and cooperative buildings three habitable stories or more must have a milestone structural inspection by the time they reach 30 years of age, with a local enforcement agency able to require it at 25 years where conditions such as coastal exposure warrant. The inspection then repeats every 10 years. It is separate from the Structural Integrity Reserve Study (SIRS), which is a funding requirement rather than a safety inspection.

Can I get a mortgage on an old condo?

Usually yes, but age becomes a problem when it shows up as deferred maintenance, an unsafe-condition finding, or thin reserves. Fannie Mae treats a project as ineligible for a conventional loan when it needs critical repairs, has significant deferred maintenance, or has been directed by an inspection authority to fix unsafe conditions, and any planned special assessment must be reviewed. A building that is non-warrantable for a conventional loan may still be financeable through a different program, so confirm with your lender early.

Do older condos have higher HOA fees?

Not always, and that can be the warning sign. An older building with unusually low fees may be underfunding its reserves rather than genuinely running lean, which sets up a special assessment when an aging component fails. What matters is whether the fees and reserve contributions are large enough to fund the replacements the reserve study projects. A higher fee that fully funds the plan is often safer than a low fee that does not.

Get Your HOA Documents Analyzed

GoverningDocs analyzes CC&Rs, reserve studies, and meeting minutes, identifying red flags, restrictions, and financial risks so you can buy with confidence. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

Sources & References

- Fla. Stat. §553.899 (milestone inspection: 3+ habitable stories, 30-year statewide trigger with 25-year local option, 10-year recurrence)

- Fla. Stat. §718.112(2)(g) (Structural Integrity Reserve Study: required components, $25,000 threshold, Dec 31 2025 deadline, no-waiver rule)

- Florida HB 913 (2025) (raised the SIRS catch-all threshold from $10,000 to $25,000 and extended the SIRS deadline)

- Fannie Mae Selling Guide B4-2.1-03 (ineligible projects: critical repairs, significant deferred maintenance, unsafe-condition directives, special-assessment review)

- Fannie Mae Lender Letter LL-2026-03 (reserve minimum 10% to 15% on Jan 4 2027; Limited Review retired Aug 3 2026)

- Association Reserves (percent-funded tiers: 0-30% weak / 30-70% fair / 70%+ strong; ~74% of associations underfunded)

- Reserve Advisors reserve-study terminology (definition of useful life and the 30-year capital-plan horizon; component life ranges are industry rules of thumb that vary by study)

- New Jersey P.L.2023, c.214 (structural inspection and capital reserve study for covered condo/co-op buildings)

- Md. Code, Real Property §11-109.4 (statewide reserve study requirement, HB 107 of 2022)

- California SB 326 / Civil Code §5551 (exterior elevated element inspections every 9 years)

- Miami-Dade County recertification ordinance (40-year recertification shortened to 30 years in 2022)

- NIST Champlain Towers South investigation (technical findings on the 2021 Surfside collapse)

- NBC News: 2018 Morabito Consultants report (major structural damage, failed waterproofing, ~$9.1M in identified repairs)

- CNN: March 2020 reserve analysis (~$706K in reserves against a ~$10.3M recommendation)

- CNN: April 2021 special assessment (~$15M program; per-unit ~$80,190 for a one-bedroom to ~$336,135 for a penthouse)

- Surfside condominium collapse overview (1981 construction, 98 deaths)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, engineering, or real estate advice. Building-inspection laws, reserve requirements, and lending rules vary by state and locality and change over time, and structural condition can only be assessed by a licensed professional. Figures and citations are current as of July 2026 and may be superseded. Read your community's actual governing documents and inspection reports, and consult a qualified real estate attorney or structural engineer for guidance specific to your situation.