In This Guide

Condo master policy premiums have doubled since 2022, and more than 1,400 Florida buildings are now on Fannie Mae's financing blacklist. If a building's insurance falls below Fannie/Freddie standards, buyers can't get a conventional loan and values drop 10–25%. Here's what to check before you offer.

Master insurance is metric #5 in The GoverningDocs 5-Number HOA Health Check and one of the six criteria in the Warrantability Checklist. That's why an insurance failure flips a building non-warrantable: the same policy weakness shows up in both frameworks, and Fannie Mae Lender Letter LL-2026-03 tightened the rules effective Jul 1, 2026. The composite verdict shows up as the GoverningDocs HOA Health Grade on every property report.

What does "insurance sufficient" actually mean for warrantability?

Three things, all set by Fannie Mae LL-2026-03 (March 2026) and Selling Guide B7-3-03 / B7-3-04. First, replacement-cost coverage on the building (ACV is allowed for roofs only as of Mar 18, 2026; ACV on the building itself triggers non-warrantability). Second, per-unit deductible at or below $50,000, effective for loan applications dated on or after July 1, 2026 (deductibles above that cap are now non-warrantable). Third, an HO-6 unit-owners policy required when the master has a per-unit deductible.

Buildings with $100K+ deductibles, ACV-on-building coverage, or no HO-6 requirement fail this test. Most of the 1,400+ Florida buildings on Fannie's blacklist failed on insurance, reserves, or both, and the two are linked because rising premiums force associations to choose between insurance and reserve contributions.

Why Insurance Now Decides Your Loan

A condo's master insurance policy used to be a line item. In 2026, it's the single most common reason conventional financing gets denied.

You find a condo that works. Price is right. The HOA dues look reasonable. Your lender pulls the condo project questionnaire from the HOA and the file comes back with one flag: master policy deductible exceeds 5% of coverage. The loan is killed. Not because of your credit. Not because of the appraisal. Because the building's insurance doesn't meet Fannie Mae's requirements.

This is happening every week in Florida, California, Colorado, and coastal Texas. According to The Real Deal, 1,438 Florida condo buildings are now on Fannie Mae's list of ineligible projects, with roughly half clustered in Miami-Dade, Broward, and Palm Beach. Many landed there because of insurance. Once a building is blacklisted, buyers need cash or a non-QM loan with 20–25% down. The buyer pool collapses. Prices follow. Florida's condo median fell 8.1% year-over-year in August 2025 per Realtor.com, and an analysis by Domex Labs estimates valuations in some South Florida submarkets are down roughly 27%.

The premium spike is the visible part of the crisis. The invisible part is what happens to financing when a building's coverage no longer meets the rules. This guide walks through both, what federal regulators changed in March 2026, and what to actually verify in the documents before you make an offer.

The Premium Spike: 2024–2026 Data

Master policy premiums doubled in three years. The pain is worst in Florida, but the pattern is national wherever climate risk is concentrated.

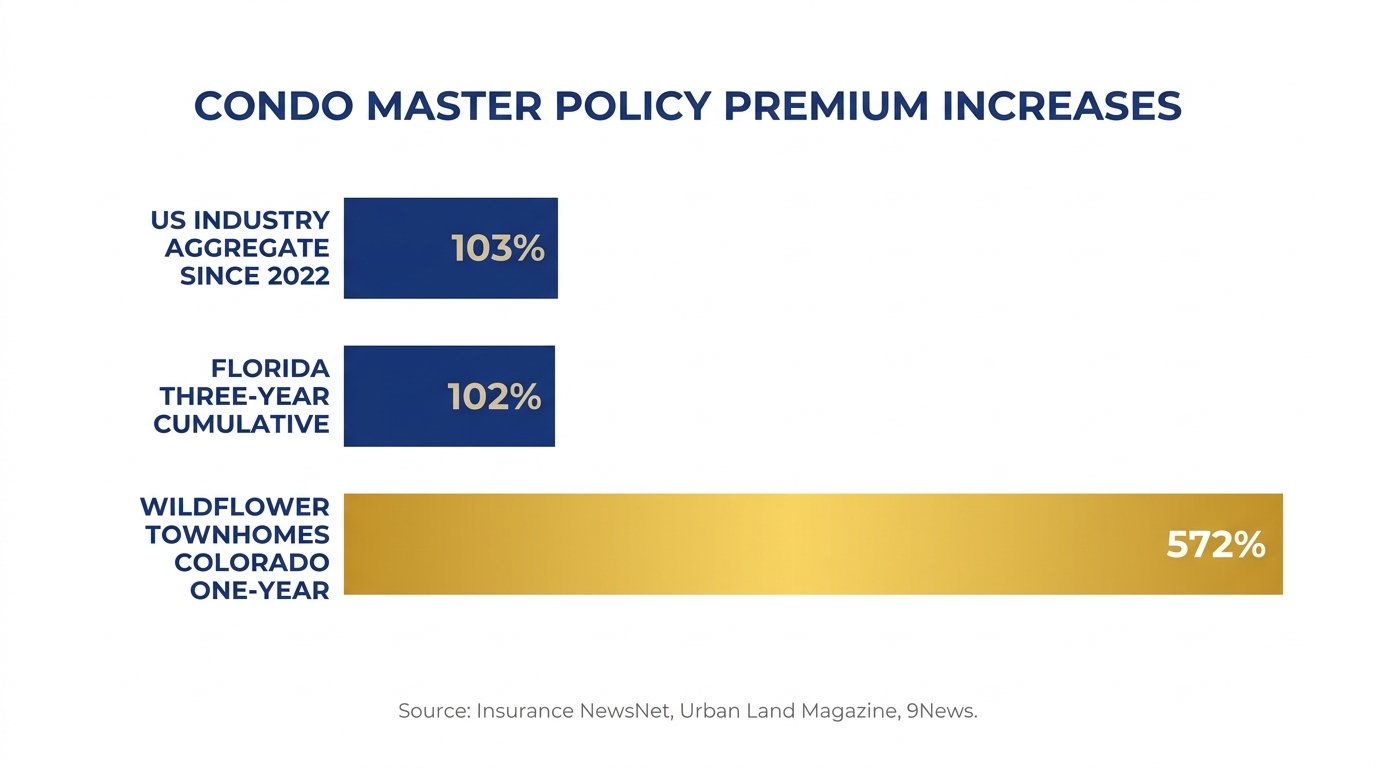

Industry data compiled by Insurance NewsNet shows condo association master policy costs have doubled since 2022, a 103% aggregate increase. Sample association renewals for 2024 came in anywhere from 11% to 54% higher than the prior year, per Connie Phillips Insurance.

Florida

Florida is the extreme case. Florida condo owners saw a 102% cumulative rate increase over three years post-Surfside, according to Urban Land Magazine. The unit-owner side of the ledger is just as stark: Florida HO-6 premiums rose from about $1,100 in 2020 to roughly $2,000 by the end of 2024, with Miami-Dade averaging $2,300, per WLRN reporting. Master policies for many coastal high-rises now run roughly two to five times their pre-2021 levels per industry reporting, with several Coral Gables and Miami-Dade buildings reporting single-renewal increases of 50% or more.

The good news: 2025 brought stabilization. Florida condo unit rates rose only 1.3% from January to September 2025, and the Florida Office of Insurance Regulation received 73 rate-decrease filings plus 94 zero-increase filings by late November, per Insurance NewsNet. Florida Peninsula filed a 12% condo rate cut, the largest in its 20-year history, taking effect on renewals in late 2025 and early 2026. Stabilization, not relief.

Outside Florida

Colorado associations have reported sharp premium increases. The Wildflower townhome community's annual master premium jumped from $65,000 in June 2022 to $437,000 in June 2023, per a 9News investigation. In California, State Farm received approval for a 17% emergency homeowners rate hike in May 2025, alongside a 32.8% landlord rate and 5.8% condo unit rate under a settlement with the California Department of Insurance. State Farm alone projects $7.6 billion in payouts from the January 2025 LA wildfires.

Why Carriers Are Leaving

At least 10 carriers have exited Florida since 2020, and major national carriers have stopped writing new policies in California. The carriers that remain charge more and exclude more.

In Florida, Farmers, FedNat, Southern Fidelity, United Insurance Holdings, and others have left the market or gone insolvent since 2020, per Insurance.com. That concentrated coverage in state-backed Citizens Property Insurance, which peaked at 1.42 million policies in October 2023. Since then, Citizens has shed about 541,000 policies through depopulation and by late 2025 was no longer Florida's largest property insurer, per Florida Realtors. Total exposure dropped sharply.

That's the recovery story. But the buildings those policies moved to are private carriers that price strictly, exclude wind in some coastal zones, and can drop coverage at renewal. Florida's 2022–2023 tort reforms (eliminating one-way attorney fees, banning assignment of benefits) brought 17 new carriers into the state, per Storm Smart. Some will write master policies. Some won't touch them.

California's story is different. State Farm stopped writing new homeowner policies in 2023. Allstate followed. Governor Newsom's emergency declaration on January 7, 2025 imposed a one-year non-renewal moratorium in LA County wildfire ZIPs, per the California Department of Insurance. Commissioner Lara's Sustainable Insurance Strategy now lets carriers use catastrophe modeling and reinsurance costs in rate-setting in exchange for writing in distressed ZIPs. Those rates, when approved, will be higher.

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →How Fannie and Freddie Use Insurance to Block Loans

Insurance requirements are in the GSE selling guides. Miss them and the building becomes non-warrantable, which means no conventional conforming loan for any buyer in that project.

Per Fannie Mae Selling Guide B7-3-03, a condo master property policy must:

- Equal 100% of the replacement cost value (RCV) of all improvements

- Settle claims on a replacement cost basis, not actual cash value (ACV)

- Carry a deductible no greater than 5% of the master policy coverage amount (with narrow exceptions)

- Document the RCV through an appraisal or comparable evidence acceptable to the lender

Miss any of those and the project fails the lender's project review. The building is flagged non-warrantable. The buyer's only options are cash, a portfolio loan from a local bank, or a non-QM loan with higher down payment (typically 20–25%) and higher rates, per BCP Mortgage. The buyer pool shrinks. The value drops.

Industry analysts estimate property values in non-compliant Florida buildings trade at material discounts (commonly cited in the 10–25% range) compared to compliant neighbors. That gap is the market pricing in the loss of the conventional-loan buyer pool.

The Coverage Gaps That Kill Deals

The master policy's declarations page often looks fine. The gaps are in the deductibles, the hurricane endorsement, and what the policy explicitly excludes.

Hurricane and Named-Storm Deductibles

Florida law ( Fla. Stat. §627.4025 ) requires carriers to offer hurricane deductibles of $500, 2%, 5%, or 10% of insured value. Coastal associations routinely end up at the 5% tier. An $80 million building at 5% means a $4 million deductible per event before coverage pays a dollar. A $10 million building at 2–5% means $200K to $500K out of pocket first, per Mitchell Joseph. That shortfall gets passed to owners as a loss assessment.

Loss Assessment Gaps on the Unit-Owner Side

Standard HO-6 unit-owner policies include only $1,000 of loss assessment coverage by default, per Stanton Insurance. Industry recommendations in 2025 are $50,000 to $100,000, particularly for high-rise and coastal buildings. Most condo owners carry the default without realizing it, then face five or six-figure assessments with no coverage.

"Bare Walls-In" Master Policies

Many master policies now insure only the structural framing, leaving drywall, flooring, cabinets, and fixtures as the owner's responsibility. Buyers reading the declarations page see impressive-looking dwelling limits and assume they're protected. Check the CC&Rs or condominium declaration for the precise coverage boundary, then match the HO-6 walls-in coverage to it.

What the March 2026 FHFA Changes Actually Do

The Federal Housing Finance Agency eased some insurance requirements in March 2026. The easing helps at the margin. It doesn't solve the problem.

On March 18, 2026, the FHFA announced three changes affecting condo project insurance:

- Actual cash value permitted for roofs only on single-family and condo buildings, instead of replacement cost

- A new $50,000 per-unit deductible cap for condo master policies (an alternative to the 5%-of-coverage rule in some scenarios), effective for loan applications on or after July 1, 2026, per Florida Realtors

- Inflation guard endorsement requirement retired

Two additional changes matter for condo buyers in 2026. The Limited Review process, which allowed streamlined condo approval for low-LTV loans on established projects, is retired on August 3, 2026 per ABA Banking Journal reporting on the Fannie Mae lender letter. And Fannie's reserve-funding threshold rises from 10% to 15% of the operating budget effective January 4, 2027. A building that squeaked by in 2026 can fail in 2027.

What to Request Before the Offer

The declarations page alone tells you almost nothing. You need the full insurance picture plus the supporting governance documents.

Request these items from the listing agent or the HOA management company before writing an offer. If the seller pushes back, that's a signal.

- Master policy declarations page. Verify 100% RCV, replacement cost (not ACV) settlement, deductible ≤5% of coverage, named-storm/wind deductible amount, carrier name, expiration date.

- Five-year loss runs. Prior claims show whether the building has a pattern of losses the next carrier will price punitively.

- Most recent lender questionnaire (Fannie Mae Form 1076 or Freddie Mac Form 476) if the HOA has one on file.

- Last 12–24 months of board meeting minutes. Search the meeting minutes for: insurance, premium, deductible, non-renewal, carrier change, questionnaire, SIRS, milestone. Board discussion precedes the formal vote by months.

- Most recent reserve study. In Florida, the structural integrity reserve study (SIRS) is required for buildings three stories and up.

- Last two operating budgets plus the current reserve fund balance.

- Most recent audited financial statements.

- Pending litigation disclosure.

On the buyer side, your HO-6 should carry loss assessment coverage of at least $50,000 (closer to $100,000 for high-rise or coastal buildings), walls-in coverage matched to what the master excludes, a separate hurricane deductible where applicable, and ordinance/law coverage if the building is older. For a deeper walkthrough of the entire financial picture, see the complete guide to HOA financial health.

Frequently Asked Questions

How much have condo master insurance premiums increased?

Industry data from Insurance NewsNet shows condo association master policy costs have roughly doubled since 2022, a 103% aggregate increase. Florida condo owners saw a 102% cumulative rate increase over three years post-Surfside, per Urban Land Magazine. Master policies for coastal Florida high-rises are now 2x to 5x their pre-2021 levels.

What are Fannie Mae's master policy insurance requirements?

Per Fannie Mae Selling Guide B7-3-03, condo master policies must provide 100% of the replacement cost value of improvements, settle claims on a replacement cost basis (not actual cash value), and carry a deductible no greater than 5% of the policy coverage amount. As of March 2026, a $50,000 per-unit deductible cap applies as an alternative in some scenarios. Buildings that miss these requirements are flagged non-warrantable.

What happens if my condo building loses insurance coverage?

If a building's insurance falls below Fannie Mae or Freddie Mac standards, the project becomes non-warrantable. Buyers can no longer use a conventional conforming loan. Their options shrink to cash, portfolio loans from local banks, or non-QM loans with 20–25% down and higher rates. With a smaller buyer pool, values in non-compliant Florida buildings have dropped 10–25% compared to compliant neighbors, per Urban Land Magazine.

How much loss assessment coverage should I have on my HO-6?

Standard HO-6 unit-owner policies include only $1,000 of loss assessment coverage by default. Industry recommendations in 2025 are $50,000 to $100,000, especially for high-rise or coastal buildings. With master policy deductibles now reaching $4 million on large coastal buildings, the assessed share per unit can easily hit five or six figures after a storm.

Did the March 2026 FHFA changes solve the condo insurance problem?

No. The FHFA changes permit actual cash value on roof coverage, introduce a $50,000 per-unit deductible cap, and retire the inflation guard requirement. Those help associations at the margin. But master policy premiums remain elevated, the Limited Review process is retiring on August 3, 2026, and Fannie's reserve-funding threshold rises from 10% to 15% on January 4, 2027. Buildings that are borderline in 2026 can still fail in 2027.

How do I find out if a condo building is non-warrantable?

Ask the HOA management company for a completed Fannie Mae Form 1076 or Freddie Mac Form 476 condo project questionnaire. Your lender can also check Fannie Mae's Condo Project Manager for unavailable-project status. Review the master policy declarations, recent meeting minutes for insurance and reserve discussions, and the most recent reserve study before committing to an offer.

Find the insurance red flags hidden in the HOA documents

Upload the reserve study, CC&Rs, or meeting minutes and get an instant risk report: reserve funding, deductible exposure, discussions of non-renewal or carrier change, and warrantability signals. Built on analysis of 1,900+ HOA documents. No signup required.

Related Articles

Sources & References

- Fannie Mae Selling Guide B7-3-03 - Master Property Insurance Requirements - 100% RCV, 5% max deductible, replacement cost basis

- FHFA - Fannie Mae and Freddie Mac Remove Certain Homeowners Insurance Requirements (March 2026) - $50,000 per-unit deductible cap, ACV roof coverage, inflation guard retired

- ABA Banking Journal - Fannie Mae and Freddie Mac Ease Certain Property Insurance Requirements - Limited Review retired August 3, 2026

- Insurance NewsNet - Condo Association Insurance Costs Doubled Since 2022 - 103% national premium increase data

- Urban Land Magazine - After Surfside, Skyrocketing Insurance Premiums Strain Condo Owners - 102% three-year FL increase, 2x–5x master policy multiples, 10–25% value impact

- Domex Labs - When Insurance (Not Inventory) Moves the Market - 1,400+ FL buildings on Fannie blacklist, 8.1% YoY median decline

- WLRN - Condominium Unit Insurance (September 2025) - FL HO-6 premium $1,100 to $2,000 trajectory

- Florida Realtors - Citizens Policies Plummet 2025 - Citizens depopulation and no longer FL's largest insurer

- California Department of Insurance - State Farm Settlement (2025) - 17% emergency rate hike, LA fire payout projections

- Florida Statute §627.4025 - Hurricane Deductible Provisions - $500, 2%, 5%, 10% deductible options

- Stanton Insurance - What Is Loss Assessment Coverage - $1,000 default and recommended $50,000–$100,000 limits

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, insurance, or real estate advice. Insurance requirements, state statutes, and Fannie Mae/Freddie Mac guidelines change frequently. Consult a qualified insurance agent, lender, and real estate attorney before making decisions based on the coverage or financing situation of a specific condominium project.