In This Guide

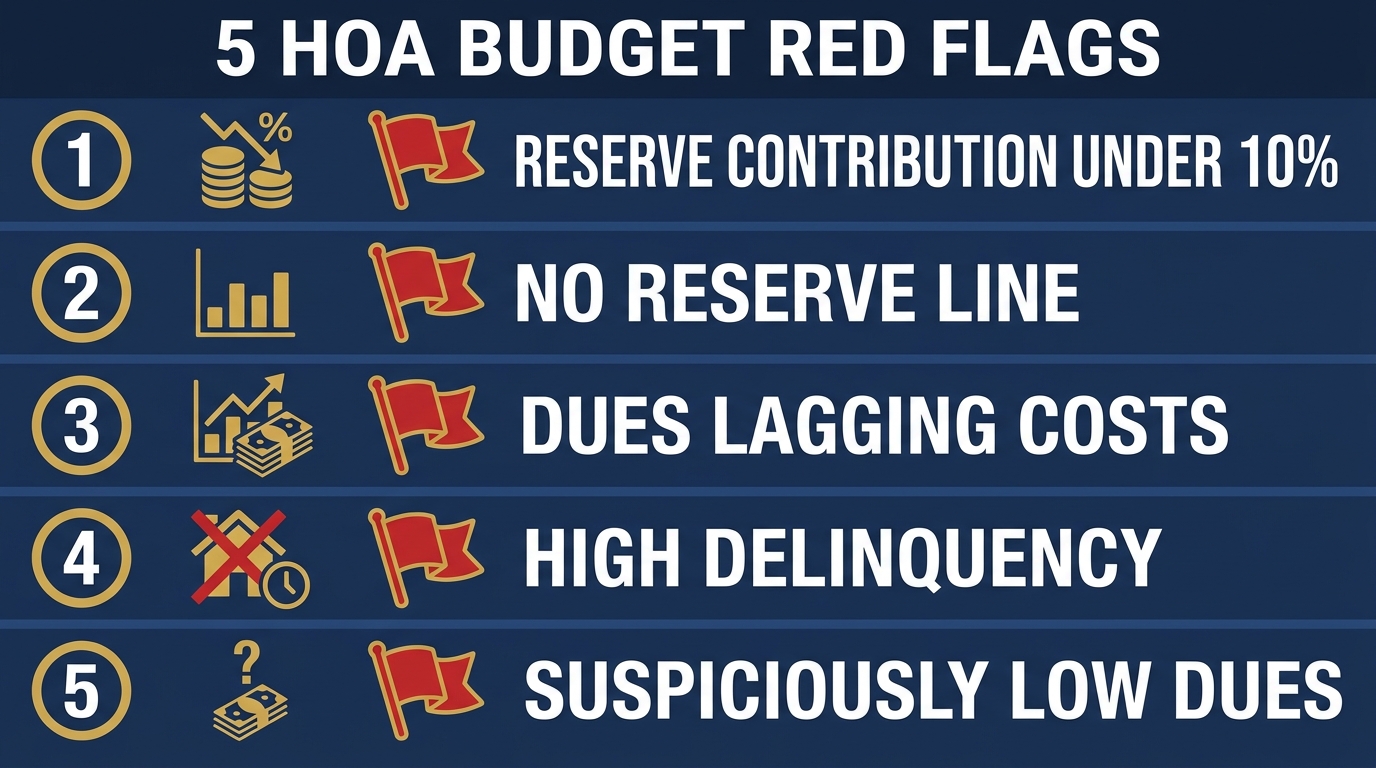

An HOA budget can balance perfectly on paper and still point to a financial crisis. The five red flags that matter most to a buyer: a reserve contribution under roughly 10% of the budget (the Fannie Mae lender floor, rising to 15% for loans dated on or after January 4, 2027), no reserve line item at all, dues that haven't kept pace with insurance and inflation, a large bad-debt or delinquency allowance (a project becomes unwarrantable above 15% delinquency), and suspiciously low dues that lean on special assessments or loans to stay afloat. The operating budget tells you about this year; the reserve study tells you about the bill coming later. Read both.

You ask for the HOA budget, the seller's agent sends it over, and the bottom line balances. Income equals expenses. You see line items for landscaping, insurance, management, utilities, and a number marked "reserves." It looks fine, so you move on to the inspection.

That balanced bottom line is exactly what hides the problem. A budget that covers this year's recurring bills can sit on top of a reserve account that is almost empty, a delinquency rate that is about to cost the whole building its financing, or dues that have been held artificially low for years while costs climbed. None of that shows up in "income equals expenses." It shows up in the line items, the assumptions behind them, and the document the budget is supposed to be funding: the reserve study.

Here are the five red flags that separate a healthy HOA budget from one that is quietly heading toward a special assessment, and where to look for each one before your contingency period runs out.

What an HOA Budget Actually Contains

An HOA budget has two halves: an operating budget for this year's recurring costs and a reserve contribution that feeds long-term repairs. They answer different questions.

Before you can spot a red flag, it helps to know what you are looking at. An association's annual budget is built from two distinct parts that answer two distinct questions.

- The operating budget answers "does income cover this year's recurring expenses?" These are the predictable, repeating costs: insurance, utilities, landscaping, management fees, pool service, pest control, minor repairs, and administrative and legal expenses. The income side is mostly the monthly dues every owner pays.

- The reserve contribution is a line item in that budget that transfers money into a separate savings account for the big, predictable, infrequent expenses: replacing the roof, repaving the parking lot, repainting the building, swapping out elevators and mechanical systems. How much should be in that account is determined by a separate document, the reserve study.

This split is the single most important thing to understand, because a building can run a perfectly balanced operating budget while contributing almost nothing to reserves. The roof is still aging whether or not anyone is saving for it. When the operating budget looks healthy but the reserve contribution is thin, the cost has not gone away. It has just been pushed into the future, where it will arrive as a special assessment or a loan instead of a planned, funded repair. That is why reading the budget and the reserve study together matters more than either one alone. The broader framework is in our complete guide to HOA financial health.

Red Flag 1: A Reserve Contribution Below 10% of the Budget

Fannie Mae requires the budget to allocate at least 10% to reserves. That floor rises to 15% for loan applications dated on or after January 4, 2027.

This is the first number to calculate, because it is the one lenders use. Under the Fannie Mae Selling Guide (section B4-2.2-02), a condo project's budget must "provide for the funding of replacement reserves for capital expenditures and deferred maintenance that is at least 10% of the budget." The test is a simple ratio: take the annual budgeted reserve contribution and divide it by the association's annual budgeted assessment income (the regular dues). If the result is below 10%, the project may not be warrantable, which means conventional Fannie and Freddie financing gets harder for every buyer in the building, including you.

That floor is about to rise. Fannie Mae's Lender Letter LL-2026-03 (issued March 18, 2026) increases the minimum reserve allocation from 10% to 15% of total annual budgeted assessment income for loan applications dated on or after January 4, 2027. The same letter eliminates the Limited Review shortcut for established projects with more than 10 units, effective August 3, 2026. So a budget contributing, say, 8% to reserves is a financing risk today and a near-certain failure once the 15% rule takes effect. We break the change down for boards and buyers in our guide to the Fannie Mae 15% reserve rule.

What to do: Find the reserve contribution or reserve transfer line in the budget. Divide it by total dues income. Below 10% is a warrantability concern now; below 15% will be a problem for loans dated in 2027 and later.

Red Flag 2: No Reserve Line, or Reserves Being Raided

A budget with no reserve contribution, or one transferring reserve cash into operations to plug a deficit, is an association living on borrowed time.

Worse than a thin reserve contribution is no reserve contribution at all. A budget with no dedicated reserve line is telling you the community is not saving for the repairs it knows are coming. The percent-funded categories that reserve professionals use put anything from 0% to 30% in the "weak" tier, 30% to 70% as "fair," and above 70% as "strong." (These tiers come from Association Reserves, the largest national reserve study firm, which reports that about three in ten of the associations it studies hold less than 30% of their recommended reserves.)

Just as telling is the reverse flow: money being moved out of reserves to cover an operating shortfall. If you see transfers from the reserve fund into the operating fund, or notes about "borrowing" from reserves to pay this year's bills, the association is spending its long-term savings on short-term costs. That is the financial equivalent of paying the electric bill with your retirement account. The repairs the reserves were meant to fund will still come due, only now there is even less money set aside for them. To check whether the reserves a budget feeds are actually adequate, run the reserve study through our reserve study analyzer, which pulls out the percent-funded figure and flags special-assessment risk.

Red Flag 3: Dues That Haven't Kept Up With Costs

If dues have stayed flat while insurance and material costs have jumped, the budget is structurally behind, even if it technically balances this year.

A budget can balance and still be quietly losing ground. The inflationary stretch from 2021 through 2024 pushed up replacement and operating costs faster than many associations adjusted their dues. Insurance in particular has been the most volatile line on the budget, especially in coastal and high-risk markets, where some associations have seen premiums climb sharply at renewal. An association that has held dues flat for several years while these costs rose is running on a structural deficit that hasn't surfaced yet.

One sign of the squeeze: the share of the budget that needs to go to reserves has crept up just to keep pace. Reserve professionals commonly point to a reserve contribution of roughly 15% to 40% of the budget as typical, with older buildings and amenity-heavy communities sitting at the high end. When you read a budget, look at the trend, not just this year's snapshot. Ask for two or three years of budgets and compare. Dues that have been frozen while expenses climbed, or an insurance line that hasn't been re-forecast for the latest renewal, are warning signs that a catch-up dues increase or an assessment is coming. Our guide to reading HOA financial statements walks through how to spot a deficit that a single year's budget can disguise.

Red Flag 4: A Large Bad-Debt or Delinquency Allowance

A big "bad debt" line means owners aren't paying. Above 15% of units 60 days past due, the project becomes ineligible for conventional financing.

Buried in the budget is a line that often reads "bad debt," "uncollectible accounts," or "allowance for delinquent assessments." It is the association's estimate of how much of the dues it bills will never get collected. A large or growing figure here tells you collections are weak, which means the owners who do pay are effectively covering for the ones who don't, and a shortfall is being absorbed somewhere.

There is a hard line attached to this. The Fannie Mae Selling Guide makes a project ineligible if more than 15% of the total units are 60 days or more past due on their common expense assessments. The same 15% test applies to each special assessment. Cross that threshold and the building loses conventional financing for everyone, which drags down resale values across the community, which makes the financial picture worse still. A delinquency assumption creeping toward that 15% wall is a serious signal, not a footnote. We cover the mechanics in depth in our guide to how the HOA delinquency rate affects a condo purchase.

Red Flag 5: Suspiciously Low Dues Propped Up by Assessments

Unusually low dues are often a deferred-cost trap. Funding a repair through a special assessment or loan costs far more than funding it through reserves.

Low HOA dues feel like a bargain. Often they are a warning. When a building's dues are noticeably lower than comparable properties of similar age and amenities, the most common explanation is not superior management. It is that the association is underfunding its reserves and planning, implicitly or explicitly, to cover big repairs with special assessments or loans when they arrive.

That choice is expensive. Association Reserves illustrates the math with a single repair: a $250,000 roof costs about $231,823 if funded gradually through budgeted reserves, the full $250,000 if covered by a special assessment, and roughly $320,071 if financed through a bank loan. Funding the same work after the fact, rather than ahead of time, can cost owners tens of thousands of dollars more. Low dues today don't make the repair cheaper; they make it more expensive and lump it into a single painful bill. The relationship is predictable: associations in the weak (0% to 30%) funded tier carry a high likelihood of special assessments, while those above 70% are largely insulated. Our companion piece, are low HOA fees a red flag, goes deeper on this specific trap.

History makes the stakes concrete. At Champlain Towers South in Surfside, Florida, the association had roughly $706,000 in reserves against about $10.3 million in recommended funding before its 2021 collapse, and owners faced a $15 million special assessment ranging from about $80,000 to $336,000 per unit. At the Cricket Club in North Miami, post-Surfside compliance triggered a $30 million special assessment, roughly $134,000 per owner, and the resale market cratered: one owner who bought for $119,000 in 2019 ended up closing at $110,000 after listing at $350,000. At San Francisco's Millennium Tower, owners were hit with a $6.8 million assessment tied to foundation overruns, an emergency charge of about $10 per square foot. In each case, the bill that arrived dwarfed what steady reserve funding would have cost. You can read more named examples in what happens when HOA reserves hit zero.

How Owners Can Push Back on a Bad Budget

Many states give owners a formal way to reject a budget. Knowing your state's mechanism tells you what recourse you'll have as an owner.

If you buy into the building, you are not powerless over the budget. State law gives owners formal tools to ratify or reject what the board adopts, and the mechanism varies by state. Knowing yours is part of due diligence, because it tells you how much say you will have.

| State | Statute | How owners can act |

|---|---|---|

| Colorado | CRS §38-33.3-303(4) | Board adopts the budget; it is deemed approved unless a majority of all unit owners vote to veto it at a ratification meeting. |

| Washington | RCW 64.90.525 | Same veto model as Colorado, and the budget must disclose the reserve contribution and the current reserve deficiency or surplus per unit. |

| Illinois | 765 ILCS 605/18(a)(8) | If a budget raises assessments above 115% of the prior year, owners holding 20% of votes can petition within 21 days to force a meeting to reject it. |

| Florida | §718.112(2)(e) | If assessments exceed 115% of the prior year, owners holding 10% of voting interests can request a meeting to adopt a substitute budget. |

| California | Civ. Code §5300 / §5550 | No owner veto, but the association must distribute an annual budget report 30 to 90 days before year-end and conduct a reserve study at least every three years. |

Two practical points fall out of this. First, in states with mandatory reserve studies on a set cadence (California every three years, Nevada every five, plus Florida's Structural Integrity Reserve Study for covered condos), a missing or stale study is itself a red flag. Second, in states like Texas and Arizona that do not mandate reserve studies at all, a clean-looking budget may simply omit reserves legally, so the absence of a reserve line tells you less and you have to dig harder. Either way, the budget is a document you can request, read, and question during your contingency period. The trick is doing it before you remove your contingencies, not after the first assessment notice arrives.

Frequently Asked Questions

How do I read an HOA budget as a buyer?

Start with the two halves: the operating budget (this year's recurring costs like insurance, utilities, and management) and the reserve contribution (savings for big future repairs). Calculate the reserve contribution as a percentage of total dues income, check for a bad-debt or delinquency line, compare dues against similar buildings, and look at two or three years of budgets to spot a trend rather than a single snapshot. Then read the reserve study alongside it.

What percentage of an HOA budget should go to reserves?

Fannie Mae requires at least 10% of the budget to go to replacement reserves for a condo project to be warrantable, and that floor rises to 15% for loan applications dated on or after January 4, 2027. Reserve professionals commonly cite a typical range of roughly 15% to 40% of the budget, with older and amenity-heavy buildings at the high end. A contribution below the 10% lender floor is an immediate financing concern.

Can a balanced HOA budget still be a problem?

Yes. A budget can balance for the year while contributing little or nothing to reserves, which means the association is not saving for predictable big repairs. A balanced operating budget says nothing about whether the roof, elevators, or pavement are funded. That gap is captured in the reserve study, which is why the budget and reserve study should always be read together.

Are low HOA dues a red flag?

Often, yes. Dues that are noticeably lower than comparable buildings frequently mean the association is underfunding reserves and plans to cover big repairs with special assessments or loans later. Funding a repair after the fact through an assessment or a loan typically costs owners significantly more than funding it gradually through reserves, so low dues today can lead to a larger bill tomorrow.

What does a high delinquency rate in an HOA budget mean?

A large bad-debt or delinquency allowance means a meaningful share of owners are not paying their dues, so the paying owners are effectively covering the shortfall. It also has a financing consequence: under the Fannie Mae Selling Guide, a project becomes ineligible for conventional financing if more than 15% of units are 60 or more days past due on common expense assessments.

Can owners reject an HOA budget?

In many states, yes. Colorado and Washington let owners veto an adopted budget by a majority vote at a ratification meeting. Illinois lets owners holding 20% of votes petition to reject a budget that raises assessments above 115% of the prior year, and Florida has a similar 10% mechanism. California does not allow a veto but requires the budget report be distributed 30 to 90 days before the fiscal year ends. Check your state's statute for the exact process.

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

Sources & References

- Fannie Mae Selling Guide B4-2.2-02 (10% reserve requirement; 15% delinquency ineligibility; reserve study recency)

- Fannie Mae Lender Letter LL-2026-03 (reserve minimum rising to 15% effective January 4, 2027; Limited Review changes)

- Association Reserves: Reserve Fund Strength (weak/fair/strong percent-funded tiers)

- Association Reserves: HOA Reserves Industry Insights Report (April 2026) (cost comparison of reserves vs special assessment vs loan)

- Colo. Rev. Stat. §38-33.3-303(4) (CCIOA owner budget-veto mechanism)

- RCW 64.90.525 (Washington WUCIOA budget ratification and reserve disclosure)

- 765 ILCS 605/18(a)(8) (Illinois 20% petition to reject a budget)

- Fla. Stat. §718.112 (Florida reserve requirement, SIRS, and owner substitute-budget mechanism)

- Cal. Civ. Code §5550 and §5300 (California reserve study cadence and annual budget report)

- CNN (Champlain Towers South reserve shortfall and $15M special assessment)

- Axios Miami (Cricket Club $30M / ~$134K-per-owner assessment and resale impact)

- NBC Bay Area (Millennium Tower $6.8M assessment, $10 per square foot)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. Reserve benchmarks, lending standards, and state budget statutes change frequently, condominium and planned-community rules differ within the same state, and the reserve and assessment figures shown are illustrative ranges and reported examples, not quoted averages. Statutes and lending guidelines referenced are current as of June 2026 and may be superseded. Consult a qualified real estate attorney and your lender for guidance specific to your situation.