In This Guide

The national median HOA or condo fee was about $135 per month in 2024 (U.S. Census). Averages run higher, roughly $200 to $355 depending on the source, because expensive high-rise condos pull the number up. Typical dues range from under $50 in covenant-only single-family communities to well over $1,000 a month in coastal high-rises. The fee alone tells you almost nothing. What matters is whether it funds the building's reserves and insurance, or leaves a repair bill waiting for you.

You are comparing two condos. One charges $250 a month, the other $520. The cheaper one looks like the smart buy, and the listing agent agrees. Then you read the reserve study on the $250 building and find it has been underfunding repairs for years, with a roof and two elevators due. The $520 fee turns out to be the honest one.

This is the problem with shopping on the HOA fee. A low number can mean a well-run, low-cost community, or it can mean a board that has been kicking maintenance down the road and is one special assessment away from a five-figure bill landing on every owner. A high number can mean amenities and fully funded reserves, or an insurance market that has spun out of control. The dollar figure does not distinguish between them.

This guide gives you the real 2026 benchmarks, what the average HOA fee actually is nationally and by state, then shows you how to read a specific fee the way an underwriter would: is it normal for the property type, and is it a red flag or a green light for the building behind it.

What Is the Average HOA Fee in 2026?

The national median HOA fee was about $135 per month in 2024 per the U.S. Census. Averages run higher because costly condos skew the mean.

The most authoritative number comes from the U.S. Census Bureau. Its 2024 American Community Survey, the first year the Census combined condo and HOA fees into a single measure, put the national median at about $135 per month across the 21.6 million owned households that pay any such fee, roughly one in four homeowners (U.S. Census Bureau). Median means half of fee-paying owners pay less than $135 and half pay more. About 5.6 million households pay under $50 a month, and roughly 3 million pay more than $500.

Watch the difference between median and average, because it trips up almost every headline. The Census $135 figure is a median. Industry aggregators that publish an average land much higher, commonly in the $200 to $355 range, because a handful of very expensive high-rise condos drag the mean upward while barely moving the median (hoacosts.com, self-reported data). Neither is wrong. They measure different things. If someone tells you the average HOA fee is $135, they have quietly swapped the median for the average.

The direction of travel is clearly up. Realtor.com listing data shows the median HOA fee on for-sale homes climbing from $108 in 2019 to $135 in 2025, while the share of listings carrying any HOA fee rose from 34.3% to 43.6% over the same period (Realtor.com data). Community associations now house nearly 80 million Americans across roughly 373,000 associations, about a third of the U.S. housing stock (Foundation for Community Association Research).

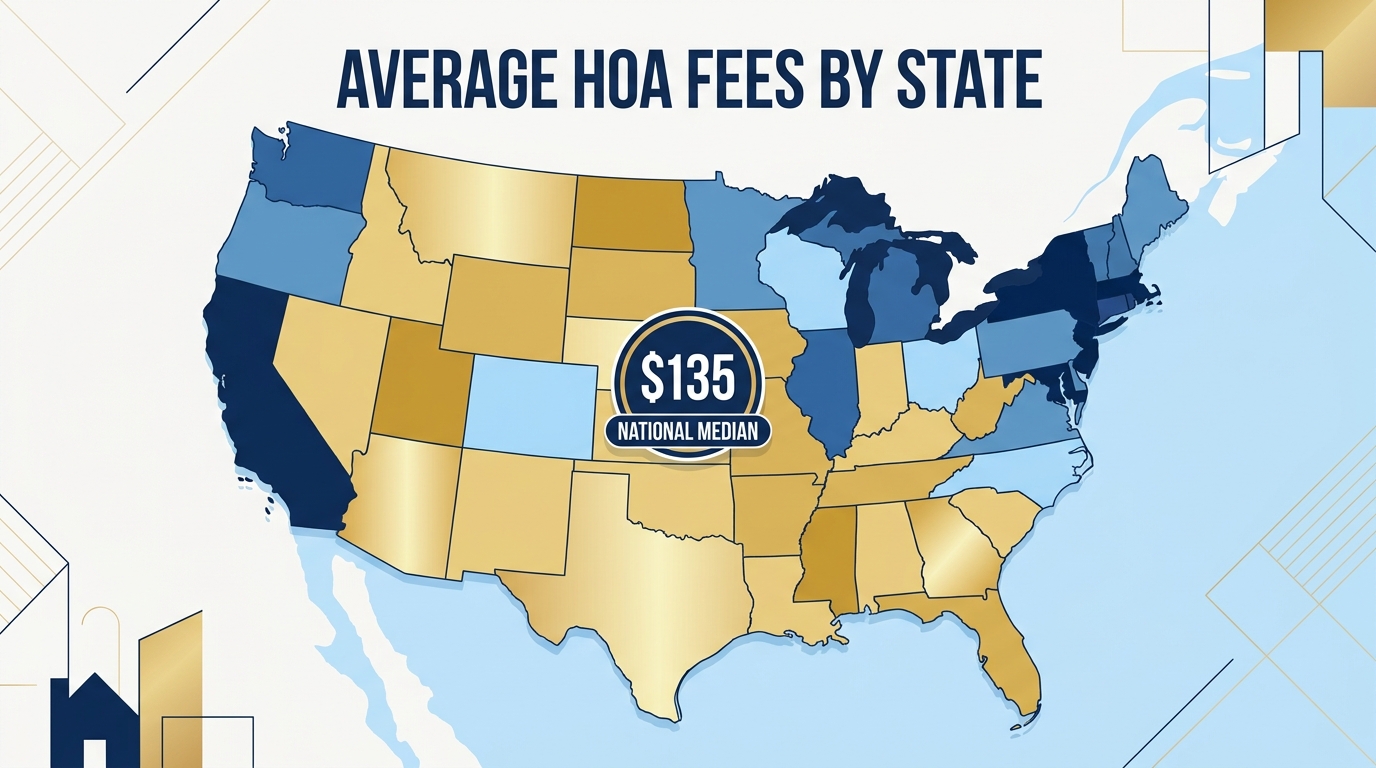

Average HOA Fees by State (2026)

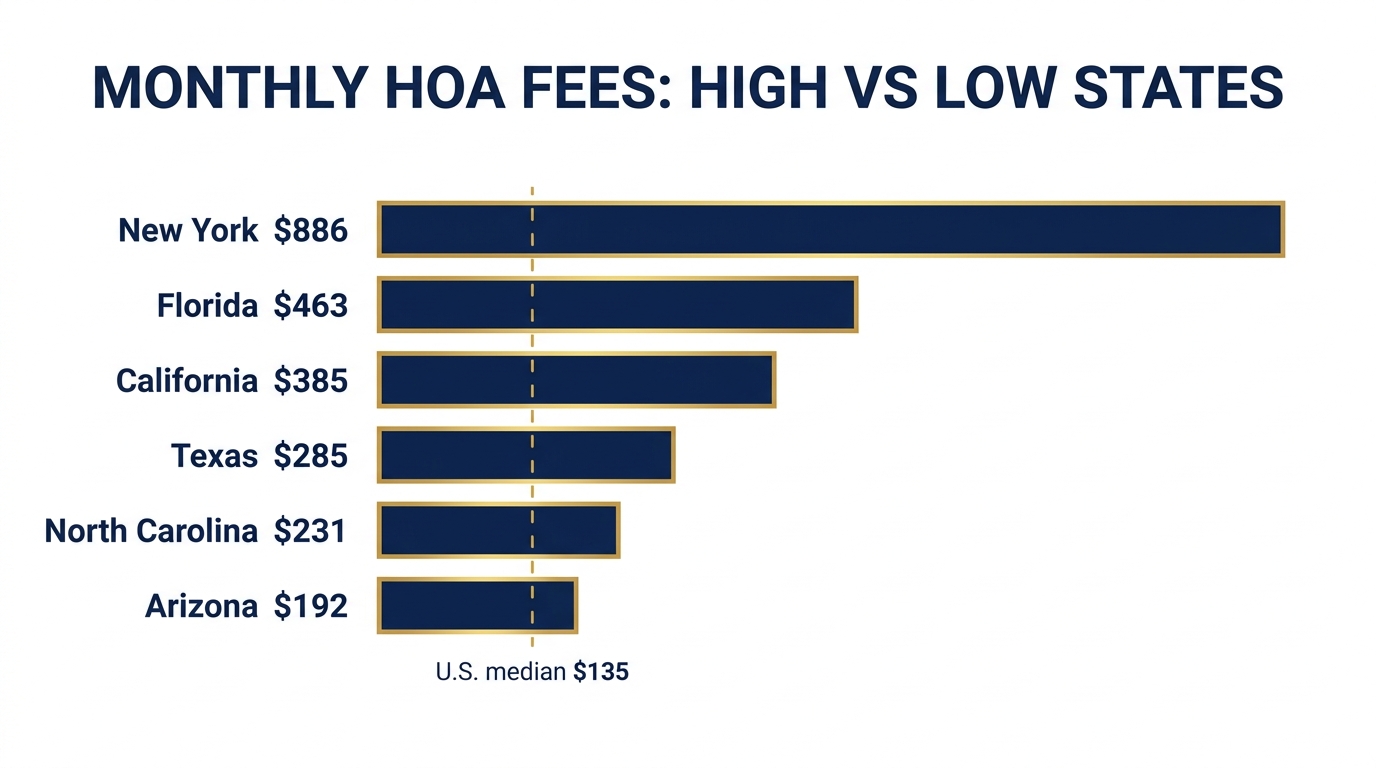

State averages range from roughly $190 in Arizona to nearly $900 in New York, but treat any state ranking as a broad estimate, not a precise figure.

There is no government table of average HOA fees by state. The Census reports a national median plus a few state signals, not a clean 50-state dollar list. The state figures below come from hoacosts.com, which aggregates self-reported dues and Census microdata. Read them as self-reported averages that skew toward condos, useful for relative ranking, not as precise, Census-grade numbers. We have shown only states with large sample sizes and left out states where the data was too thin to trust.

| State | Reported average monthly fee |

|---|---|

| New York | ~$886 |

| Washington, D.C. | ~$787 |

| Hawaii | ~$605 |

| Massachusetts | ~$513 |

| Florida | ~$463 |

| Connecticut | ~$427 |

| New Jersey | ~$423 |

| Minnesota | ~$398 |

| California | ~$385 |

| Illinois | ~$364 |

| Washington | ~$326 |

| Michigan | ~$319 |

| Ohio | ~$289 |

| Texas | ~$285 |

| Georgia | ~$283 |

| Maryland | ~$281 |

| Colorado | ~$268 |

| Virginia | ~$261 |

| North Carolina | ~$231 |

| Tennessee | ~$209 |

| Nevada | ~$207 |

| Arizona | ~$192 |

The Census data corroborates the top of that list. New York has by far the highest dues, with 64% of fee-paying New York homeowners paying more than $500 a month, the highest share of any state, followed by Washington, D.C., and Hawaii at about 50% each. The states with the highest share of homeowners paying any HOA fee are Arizona, Florida, and Nevada, which are heavy with planned and retirement communities, even though their average dollar figures sit at the lower end because so many of those are covenant-only single-family HOAs with minimal services.

Why HOA Fees Vary So Much by State

Insurance costs, building type, reserve mandates, and amenities drive the spread, so the same fee can mean very different things in different states.

The gap between Arizona and New York, more than fourfold, is not random. Four forces explain almost all of it:

- Insurance. Master property insurance is the single biggest driver of rising dues, especially in Florida, California, and coastal markets where premiums have doubled or tripled since 2022. When the building's policy jumps, dues follow.

- Building type. A high-rise condo with elevators, structural systems, and a doorman costs far more to run than a single-family HOA that only maintains a few common areas. Realtor.com listing data shows 84.8% of condo and townhome listings carry a fee, versus 33.4% of single-family listings (Realtor.com data).

- Reserve requirements. States that mandate funded reserves and structural inspections, led by Florida after the 2021 Surfside collapse, force dues up to legally required levels that some associations had avoided for years.

- Amenities and services. Pools, gyms, gated security, landscaping, and bundled utilities all live inside the fee. Two buildings with identical fees can deliver wildly different value.

Most states also place no statutory cap on how much an HOA can raise dues, so the ceiling is set by the governing documents, not the law. We cover that in can an HOA raise fees with no limit.

Florida and California: The Two States Buyers Ask About

Florida dues are spiking on insurance and new reserve laws. California runs high on high-rise stock and disaster-market insurance.

Florida averages roughly $463 a month across the largest state sample in the data, but that headline hides a fast-moving story. Coastal condos commonly run $350 to $800 a month, and high-rises exceed $1,000. In Miami-Dade, average high-rise assessments have climbed past $1,900 a month (WLRN), and the county's median condo fee rose from $567 to $900 between 2019 and 2024, a 59% jump (Miami Herald). Two forces are driving it: insurance premiums that have doubled or tripled, and Florida's post-Surfside reserve laws. Under the Structural Integrity Reserve Study requirements and milestone-inspection deadlines (statutes 718.112(2)(g) and 553.899, updated by HB 913 in 2025), associations that once waived reserves must now fully fund them, resetting dues upward.

California averages about $385 a month, second only to the Northeast among large states. The drivers are high-rise condo stock in San Francisco, Los Angeles, and San Diego, earthquake and wildfire insurance in a stressed market, aging inventory, and the reserve-study and reserve-disclosure requirements of the Davis-Stirling Act (Civil Code 5550, the reserve study, and 5565, the reserve disclosure summary). As in Florida, the trend line points up.

What's a Normal Fee for Your Property Type?

Compare against similar properties, not the national number. Single-family HOAs run low, condos mid-range, and high-rises far higher.

The national median is a starting point, but a $135 benchmark is meaningless if you are buying a downtown high-rise. Compare a fee against its own category:

- Single-family HOA (covenant only). Often under $50 to a few hundred dollars a month. These associations maintain shared landscaping, signage, and maybe a pool, but each owner insures and maintains their own home, so fees stay low.

- Condo or townhome. Commonly $300 to $500 or more. The fee bundles the master insurance policy, exterior and roof maintenance, and sometimes water and trash, which single-family owners pay separately.

- High-rise or luxury condo. $500 to well over $1,000 a month. Elevators, structural systems, staffing, and amenities carry real recurring cost, and coastal insurance adds a large premium on top.

A $400 fee is unremarkable for a Florida condo and a screaming outlier for a Phoenix single-family HOA. The number only becomes a red flag or a green light once you place it next to comparable buildings and, more importantly, look at what the fee is actually funding.

When a Low HOA Fee Is a Red Flag

An unusually low fee often means underfunded reserves and deferred maintenance, which surface later as a special assessment.

A below-market fee is frequently a warning, not a bargain. Dues that are held artificially low usually come out of the reserve line, the fund that pays for big future repairs like roofs, elevators, and repaving. The health of that fund is measured by percent funded, the ratio of actual reserves to what a reserve study says the building should have saved. Association Reserves, a national reserve-study firm, groups percent funded into three bands (Association Reserves):

- 0 to 30% (weak). Special assessments are common and deferred-maintenance risk is high.

- 30 to 70% (fair). Special assessments are infrequent.

- 70% and above (strong). Special assessments are rare and the building is largely pre-paying its future repairs.

The mechanism is simple. Low dues lead to thin reserves, percent funded drifts down, deferred maintenance piles up, and eventually the building funds a major repair through a special assessment or an emergency dues hike. The buyer who "saved" $80 a month inherits a $30,000 bill. This is the exact dynamic playing out across Florida right now, where years of artificially low condo fees are being reset upward by mandatory inspections and reserve funding. For the full argument, see are low HOA fees a red flag and our guide to HOA special assessments.

When a High HOA Fee Is Perfectly Fine

A high HOA fee is perfectly fine when it buys real amenities, fully funded reserves, or coverage in a costly insurance market.

A high fee is not automatically bad, and this is where fee-shopping buyers make their second mistake. A large monthly number can reflect three perfectly healthy things. It can pay for real amenities and services, elevators, staffing, pools, security, bundled utilities, that you would otherwise pay for separately. It can mean the association is funding its reserves properly, so you are far less likely to face a surprise assessment. And it can reflect a high-cost insurance market like coastal Florida or wildfire-exposed California, where the premium is simply the price of owning there.

The question is never whether the fee is high or low. It is whether the fee is adequate for what the building actually needs. A well-run community with a fully funded reserve and a fair fee is worth far more than a neighbor charging half as much and quietly deferring its roof. Check the percent funded before you judge the dollar amount.

How HOA Fees Affect Your Financing

The fee itself counts toward your debt-to-income ratio, and the reserves it funds decide whether the building is even lender-eligible.

HOA fees shape your loan in two ways. First, the fee is folded into your monthly housing cost and counts against your debt-to-income ratio, so a $600 fee can shrink the loan you qualify for just as much as a higher interest rate would. Second, and less obvious, the reserves that the fee funds decide whether the building is eligible for a conventional loan at all.

Fannie Mae and Freddie Mac will only back a loan if the project passes their standards. Two of those are moving in 2026 and 2027, both set out in Fannie Mae Lender Letter LL-2026-03:

| Rule | Threshold | Effective |

|---|---|---|

| Reserve minimum | Budget must fund reserves at 10% of income, rising to 15% | 15% from Jan 4, 2027 |

| Limited Review retired | Established projects over 10 units move to Full Review | Aug 3, 2026 |

| Delinquency ceiling | Project ineligible if more than 15% of units are 60+ days past due | In effect |

A building whose low fee cannot fund reserves to those levels risks becoming non-warrantable, which cuts off conventional financing for every unit, not just the one being sold. The same 15% delinquency test applies to FHA. One nuance to keep straight: VA does not enforce a hard 15% delinquency cutoff the way Fannie, Freddie, and FHA do, so VA eligibility can survive where a conventional loan cannot, but that has to be confirmed with the lender for the specific project. See the 2026 Fannie and Freddie condo rules, the 15% delinquency rule, and what a non-warrantable condo means.

The takeaway for a buyer is to stop reading the fee as a price and start reading it as a signal. Pull the budget, the reserve study, and the delinquency report, and check whether the fee is actually funding the building or hollowing it out. Our HOA budget red flags guide and the HOA financial health guide walk through exactly what to look for, and the reserve fund calculator helps you sanity-check the numbers.

Frequently Asked Questions

What is the average HOA fee in the United States in 2026?

The U.S. Census Bureau put the national median condo and HOA fee at about $135 per month in 2024, its most recent data. Industry aggregators that report an average rather than a median land higher, commonly $200 to $355 per month, because expensive high-rise condos pull the average up while barely affecting the median.

Which states have the highest HOA fees?

New York has the highest, with an estimated average near $886 a month and 64% of fee-paying owners paying more than $500. Washington, D.C., Hawaii, Massachusetts, Florida, New Jersey, Connecticut, and California follow. These are driven by high-rise condo stock and expensive insurance markets.

Which states have the lowest HOA fees?

Among states with reliable data, Arizona (about $192), Nevada (about $207), Tennessee (about $209), and North Carolina (about $231) sit at the low end. These states have many covenant-only single-family HOAs that maintain shared common areas but leave each owner responsible for their own home, which keeps dues low.

Is a low HOA fee a good thing?

Not always. An unusually low fee often means the association is underfunding its reserves, the fund that pays for major future repairs. That can surface later as a large special assessment. Before treating a low fee as a bargain, check the reserve study and the building's percent funded to see whether the dues are actually covering long-term costs.

Why are Florida HOA and condo fees rising so fast?

Two forces. Property insurance premiums in Florida have doubled or tripled since 2022, and the state's post-Surfside reserve laws now require Structural Integrity Reserve Studies and milestone inspections. Associations that used to waive reserves must fully fund them, which resets dues upward. Miami-Dade condo fees rose about 59% over five years as a result.

Do HOA fees affect whether I can get a mortgage?

Yes, in two ways. The fee counts toward your debt-to-income ratio, so a high fee reduces the loan you qualify for. And the reserves the fee funds determine whether the building itself is eligible for a conventional Fannie Mae or Freddie Mac loan. A building with chronically low fees and thin reserves can become non-warrantable, which limits financing for every unit.

Get Your HOA Documents Analyzed

GoverningDocs analyzes CC&Rs, reserve studies, and meeting minutes, identifying red flags, restrictions, and financial risks so you can buy with confidence. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

Sources & References

- U.S. Census Bureau (2024 ACS: national median condo/HOA fee $135/month; 21.6M paying households; state shares paying over $500)

- hoacosts.com (self-reported state average monthly fees; national average ~$355; used for the state ranking with a large-sample filter)

- Realtor.com data (via Mecklenburg Times) (listing HOA fee median $108 in 2019 to $135 in 2025; 43.6% of listings carry a fee; 84.8% of condos/townhomes)

- Foundation for Community Association Research (~373,000 associations; nearly 80 million residents; about one-third of U.S. housing stock)

- WLRN (Miami-Dade high-rise assessments over $1,900/month)

- Miami Herald (Miami-Dade median condo fee $567 in 2019 to $900 in 2024, +59%, based on Redfin listing data)

- Florida Senate, HB 913 (2025) (SIRS deadline Dec 31, 2025; baseline reserve funding plan; reserve-item threshold raised to $25,000; effective July 1, 2025)

- Association Reserves (percent-funded strength bands: 0 to 30% weak, 30 to 70% fair, 70% and above strong)

- Fannie Mae Lender Letter LL-2026-03 (reserve minimum 10% to 15% effective Jan 4, 2027; Limited Review retired Aug 3, 2026)

- Fannie Mae Selling Guide B4-2.2-02 (Full Review: 15% delinquency ceiling, reserve funding requirement)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. HOA fee figures are estimates drawn from Census and industry data, vary widely by building and market, and change over time. State averages are approximate and should not be treated as precise or Census-grade. Figures are current as of July 2026 and may be superseded. Review a specific association's budget and reserve study, and consult a qualified real estate attorney for guidance specific to your situation.