In This Guide

There is no single dollar figure that is "enough" for every building, because reserves depend entirely on what a property has to replace and when. The right yardstick is percent funded: the actual reserve balance divided by the fully funded balance the reserve study calculates. A reserve above 70% funded is considered strong, 30% to 70% is fair, and below 30% is at risk. By that measure, 74% of community associations are underfunded, according to Association Reserves. This guide gives you two ways to estimate what your specific building should have saved, so you can judge a reserve fund before you buy instead of inheriting someone else's shortfall.

"The reserves look healthy." It is one of the most common things a buyer hears, and one of the least useful, because almost no one says what they are comparing the balance to. A $400,000 reserve fund sounds reassuring until you learn the building needs $1.2 million in roof, elevator, and facade work over the next decade. The number on the bank statement means nothing on its own.

That gap is where six-figure special assessments come from. When a building has saved far less than its aging components will cost to replace, the shortfall does not disappear. It lands on whoever owns a unit when the roof finally fails or the garage has to be reconcreted, as a lump-sum bill that can run from a few thousand dollars to well over $100,000 per unit. The previous owner sells before the bill arrives. The buyer who skipped the math inherits it.

The good news is that the math is not complicated, and you do not need to be an accountant to do it. Below are the two numbers that tell you whether a reserve fund is adequate, two ways to estimate the target your building should be hitting, and the lending and state rules that set a hard floor underneath all of it.

How Much Should an HOA Have in Reserves?

A strong reserve holds at least 70% of its fully funded balance, the cost of accumulated wear on every major component. The real target comes from the building's reserve study.

The honest answer to "how much should an HOA have saved?" is "enough to cover the wear it has already accumulated on its major components." A reserve fund is not a rainy-day account or a savings buffer. It is money set aside specifically to repair and replace the big-ticket shared assets, the roof, elevators, plumbing risers, paving, painting, pool, and structural systems, as they reach the end of their useful lives.

Because those components age continuously, the target balance grows every year. A reserve study quantifies it as the fully funded balance, the dollar value of the deterioration that has already happened. The closer a building's actual savings sit to that number, the better positioned it is to pay for the next big repair out of reserves instead of an emergency assessment. That ratio, actual savings divided by the fully funded balance, is percent funded, and it is the single most important reserve number a buyer can look at.

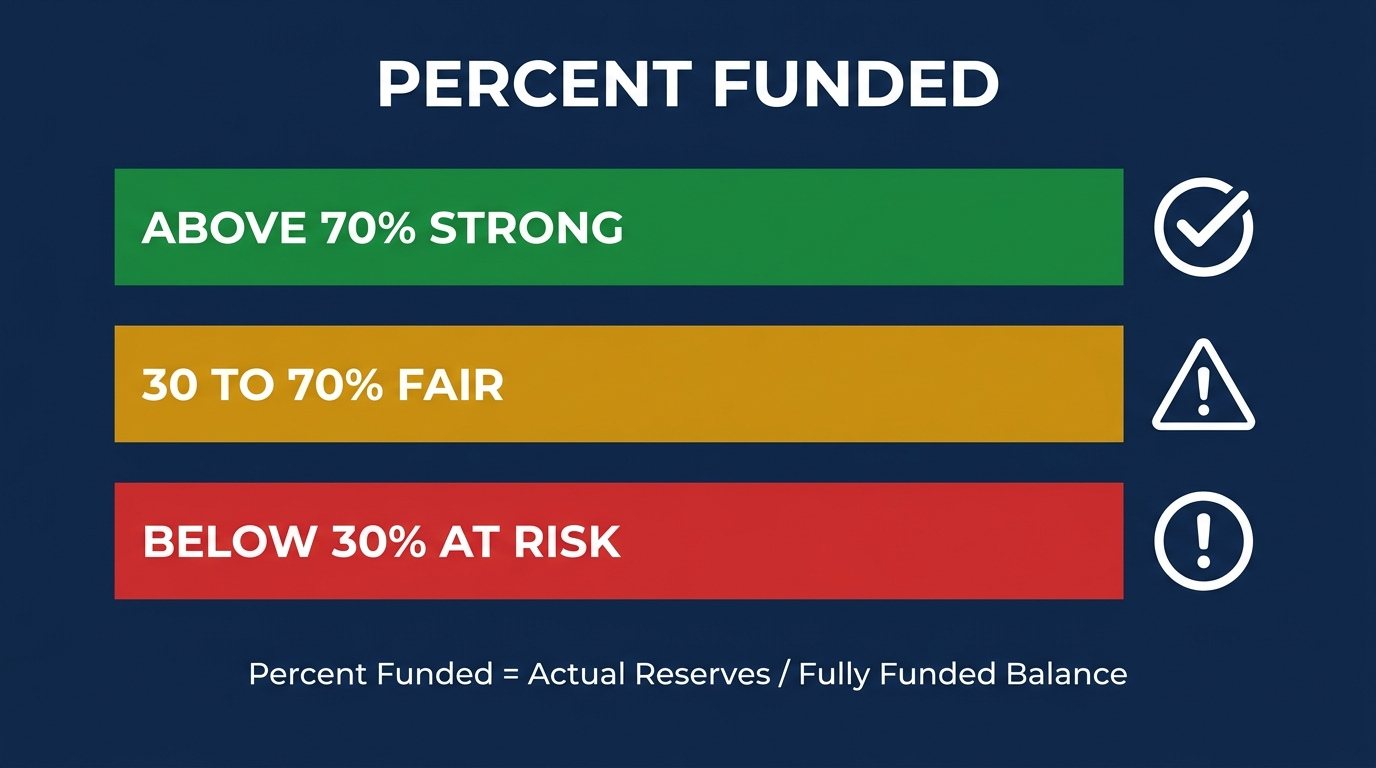

The Number That Actually Matters: Percent Funded

Percent funded = actual reserve balance / fully funded balance. Above 70% is strong, 30% to 70% is fair, below 30% is at risk of a special assessment.

Percent funded translates a building's reserve balance into a grade that works regardless of the building's size, age, or location. The formula, defined by Association Reserves, is simply:

Percent Funded = Actual Reserve Balance ÷ Fully Funded Balance

The fully funded balance is built component by component. For each major asset, the study multiplies its fractional age (how much of its useful life has been used) by its current replacement cost, then adds them up. A roof that is 7 years into a 20-year life and costs $200,000 to replace contributes 7/20 of $200,000, or $70,000, to the target. Paint that is 3 years into a 5-year cycle at $50,000 contributes $30,000. Add those and the fully funded balance is $100,000. If the building has actually saved $40,000, it is 40% funded.

Association Reserves groups the result into three tiers that buyers can use as a quick verdict:

| Percent funded | Tier | What it means for a buyer |

|---|---|---|

| Above 70% | Strong | Low probability of a special assessment; the building can usually fund major repairs from reserves. |

| 30% to 70% | Fair | Workable but watch the trend; a single large project can force an assessment. |

| Below 30% | At risk | High probability of a special assessment; every major repair becomes a cash call. |

These tiers and the underfunding statistic come from Association Reserves, which has analyzed more than 100,000 reserve studies, not from a single rule of thumb. Their finding is blunt: 74% of associations are less than 70% funded. If you walk into a purchase assuming the building is fine, the data says you are more likely wrong than right. For a deeper walkthrough of the metric, see our explainer on what counts as a good percent funded, and our guide to reading a reserve study in five minutes.

Two Ways to Estimate Your Building's Reserve Target

If you have the reserve study, use percent funded directly. If you only have the budget, screen the reserve contribution as a share of dues to flag underfunding fast.

There are two paths to sizing what a building should have saved. The first is precise and uses the reserve study. The second is a quick screen you can run from the annual budget alone when no study is in front of you.

Path A: From the reserve study (most accurate)

If you have the reserve study, the work is mostly reading, not calculating:

- Find the fully funded balance in the study (sometimes labeled "fully funded reserve" or shown alongside percent funded).

- Find the actual current reserve balance from the study's starting balance or the association's financial statements.

- Divide actual by fully funded. Example: $350,000 saved against a $500,000 fully funded balance is 70% funded, right at the strong threshold.

- To reach "strong," the building needs at least 70% of its fully funded balance ($350,000 in this example). To be fully funded, it needs the entire $500,000.

Most reserve studies state the percent funded outright, so this is often a matter of confirming the math rather than running it. Our free reserve study analyzer pulls the percent funded, fully funded balance, and special-assessment risk out of an uploaded study automatically.

Path B: From the budget (a quick screen)

When you only have the operating budget, you cannot calculate the true target balance, but you can flag obvious underfunding by looking at how much of dues income goes to reserves each year:

- Find the annual reserve contribution (the reserve line item) and divide it by total annual assessment income. On a $1,000,000 budget, a $100,000 reserve line is 10%.

- As a rough industry guideline, healthy associations often direct 15% to 40% of assessment income to reserves, with older buildings and amenity-heavy properties at the higher end. This is a rule of thumb, not a standard, so treat it as a screen, not a verdict.

- Mortgage lenders set a harder floor: at least 10% of the budget to reserves today, rising to 15% for loans dated on or after January 4, 2027 (more on that below). A building contributing well under 10% is very likely underfunded.

The key limit to keep in mind: Path B sizes the annual contribution, not the target balance. A building can contribute a healthy percentage today and still be deep in a hole if it underfunded for years. Only a reserve study gives the true target. Use the budget screen to decide whether to dig deeper, not to clear a building. There is no reliable per-unit dollar benchmark, because the target depends on the specific assets a building owns and their ages, so be skeptical of any "X dollars per door" shortcut.

What Lenders Require (and Why It Sets a Floor)

Fannie Mae requires at least 10% of the budget go to reserves, rising to 15% for loans dated on or after January 4, 2027. Miss it and buyers lose conventional financing.

Even if you are paying cash, the lending rules matter, because they determine whether the next buyer can get a mortgage, which determines what your unit is worth. Under the Fannie Mae Selling Guide (B4-2.2-02), a condo project's budget must allocate at least 10% of its annual budgeted assessment income to replacement reserves. That floor rises to 15% for loan applications dated on or after January 4, 2027, under Lender Letter LL-2026-03. We cover the change in detail in our guide to the Fannie Mae 15% reserve rule.

A building can satisfy the requirement another way: a reserve study completed within the past three years by a qualified professional can substitute for the percentage test, but only if reserves meet or exceed the study's recommendations and the budget follows the study's highest recommended funding plan. Under the 2027 rule, the riskiest funding approach, baseline funding (which lets the balance drift toward zero), no longer qualifies for that exception.

The consequence of falling short is severe and largely invisible until it bites. Projects with thin reserves, deferred critical repairs, insurance gaps, or active litigation can land on Fannie Mae's list of ineligible projects, which reportedly held about 5,175 condo and co-op projects in 2025, up from roughly 1,400 in mid-2023. Once a project is ineligible, conventional Fannie and Freddie loans dry up, the buyer pool shrinks to cash and portfolio borrowers, and values follow. Owners usually find out only when a buyer's loan gets rejected at the closing table.

What Your State Requires

Most states require periodic reserve studies; a few set funding rules. Florida now bars waiving structural reserves. Colorado only requires a disclosure policy, not funding.

State law shapes how seriously a building has to take its reserves. Some states mandate regular professional studies, a few restrict waiving reserves, and others require only disclosure. Here is how several major states handle it.

| State | Statute | What it requires |

|---|---|---|

| Florida | Fla. Stat. §718.112(2)(g) | Condo and co-op buildings three or more habitable stories must have a Structural Integrity Reserve Study. For budgets adopted on or after December 31, 2024, owner-controlled associations may not vote to underfund the structural reserve items. |

| California | Civ. Code §5550 / §5565 | A reserve study (with visual inspection) at least every three years, reviewed annually, plus an annual Assessment and Reserve Funding Disclosure Summary showing components, fully funded balance, and percent funded. |

| Nevada | NRS 116.31152 / 116.3115 | A reserve study at least every five years, an annual review of whether reserves are sufficient, and annual adjustment of the funding plan to provide adequate funding. |

| Washington | RCW 64.90.545 | A reserve study prepared and updated annually, with a professional visual site inspection at least every three years (limited exemptions for nominal reserve costs). |

| Virginia | Va. Code §55.1-1965 | A reserve study at least every five years, reviewed annually, with budget and assessment adjustments to maintain reserves for capital components. |

| Colorado | C.R.S. §38-33.3-209.5 | No reserve study or funding is mandated; the association must adopt a written reserve-study policy disclosing whether a study and funding plan exist. A disclosure state, not a minimum-funding state. |

The pattern to notice: even states that require a study rarely dictate a minimum dollar balance. The study tells the building what it should have; whether the board actually funds it is a separate question. That is why percent funded, not a statute, is your best gauge. Always confirm the current statute text for the specific state, since reserve laws have been changing quickly, particularly after the 2021 Surfside collapse.

Why Low Fees Usually Mean Low Reserves

Underfunding is a deferral, not a saving. Construction costs keep rising, so the bill grows the longer a building waits, then arrives all at once as an assessment.

A reserve that looks thin is almost always the product of dues that were kept low, and low dues are a powerful selling point that boards and developers are reluctant to give up. But money not collected for reserves is not money saved. It is a cost deferred, and deferred costs grow. Construction prices keep climbing; the Engineering News-Record Building Cost Index rose 4.2% in 2025 alone, with steel up nearly 12%. A roof that could have been funded gradually over twenty years costs more in real dollars the longer the building waits, and when it finally fails the entire bill arrives at once.

The cautionary cases are not hypothetical. Champlain Towers South in Surfside, Florida, held under $800,000 in reserves against a recommended level of roughly $10.3 million, leaving it funded at about 6.9%, while it faced an estimated $16 million in needed repairs. The board finally levied a $15 million special assessment in 2021. The Cricket Club in North Miami hit owners with a $30 million assessment, about $134,000 per owner, for safety-driven repairs. These are extreme outcomes, but the mechanism behind them, years of underfunding catching up at once, is the ordinary case that the percent-funded math is designed to catch early. For a fuller set, see our look at what happens when HOA reserves hit zero.

What to Check Before You Buy

Pull the reserve study and budget, calculate percent funded, check the reserve contribution against the 10%-to-15% lending floor, and read the funding plan.

Before you remove your contingencies, run the reserve fund through a short checklist:

- Get the reserve study and calculate percent funded. Actual balance divided by fully funded balance. Below 30% is a serious warning; aim to understand why anything under 70% is where it is.

- Check the reserve contribution in the budget. Divide the reserve line by total dues. Under 10% is a financing concern today; under 15% will be one for loans dated in 2027 and later. Our guide to reading an HOA budget walks through the calculation.

- Look at the trend, not just the snapshot. A building at 45% funded and climbing is healthier than one at 60% and falling. Several years of financials show the direction.

- Read the funding plan. A credible study lays out how the building gets from where it is to where it should be. A plan that relies on a future special assessment is telling you one is coming.

- Confirm what your state requires. Check whether a study is mandated and how recent the current one is. A stale or missing study is itself a red flag.

None of this requires special expertise, just the documents and a few minutes of arithmetic. The reserve fund is the clearest financial signal a building gives off before you buy, and unlike the lobby or the model unit, it does not lie about what is coming.

Frequently Asked Questions

How much should a condo association have in reserves?

Enough to cover the accumulated wear on its major components, measured as percent funded: the actual reserve balance divided by the fully funded balance the reserve study calculates. A building above 70% funded is considered strong, 30% to 70% is fair, and below 30% is at risk of a special assessment. There is no universal dollar figure, because the target depends on each building's specific assets and their ages.

What is a good percent funded for an HOA?

According to Association Reserves, above 70% funded is strong, 30% to 70% is fair, and below 30% is at risk. Higher is better, with 100% meaning the building has saved exactly the value of the deterioration its components have accumulated. Most associations fall short: 74% are less than 70% funded.

Is 50% funded okay for a condo building?

Fifty percent funded sits in the "fair" range, which is workable but not comfortable. It means the building has saved about half of what its aging components are worth, so a single large project, like a roof or elevator replacement, can outstrip reserves and trigger a special assessment. Look at the trend and the funding plan: 50% and climbing is reassuring, 50% and falling is a warning.

What happens if HOA reserves are too low?

Low reserves mean major repairs cannot be paid from savings, so the board funds them through special assessments (lump-sum bills that can run from a few thousand dollars to over $100,000 per unit) or large dues increases. Severely underfunded buildings can also become non-warrantable, losing access to conventional Fannie Mae and Freddie Mac financing, which shrinks the buyer pool and depresses values.

How much of HOA dues should go to reserves?

As a general industry guideline, many healthy associations direct 15% to 40% of assessment income to reserves, with older and amenity-heavy buildings at the higher end. Mortgage lenders set a harder floor: Fannie Mae requires at least 10% of the budget today, rising to 15% for loan applications dated on or after January 4, 2027. A building contributing well under 10% is very likely underfunded.

Does my state require an HOA reserve study?

It varies. California (every three years), Nevada and Virginia (every five years), and Washington (annually updated) all require periodic studies. Florida requires a Structural Integrity Reserve Study for buildings three or more stories and bars underfunding structural reserves for budgets adopted on or after December 31, 2024. Colorado requires only a written reserve-study policy, not a study or funding. Always confirm the current statute for your state.

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

Sources & References

- Association Reserves (definition of percent funded and the fully funded balance calculation)

- Association Reserves (74% of associations are less than 70% funded, based on 100,000+ studies)

- Fannie Mae Selling Guide B4-2.2-02 (10% reserve allocation requirement)

- Fannie Mae Lender Letter LL-2026-03 (reserve minimum rising to 15% for loans dated on or after January 4, 2027)

- The Mortgage Reports (Fannie Mae ineligible-project count, approximately 5,175 in 2025)

- Fla. Stat. §718.112(2)(g) (Structural Integrity Reserve Study requirement)

- Cal. Civ. Code §5550 (reserve study every three years) and §5565 (reserve funding disclosure)

- NRS 116.31152 and 116.3115 (Nevada reserve study and funding requirements)

- RCW 64.90.545 (Washington reserve study requirement)

- Va. Code §55.1-1965 (Virginia reserve study requirement)

- C.R.S. §38-33.3-209.5 (Colorado reserve-study policy disclosure)

- Engineering News-Record (2025 Building Cost Index increase)

- CNN (Champlain Towers South reserve funding and $15 million special assessment)

- Axios Miami (Cricket Club $30 million assessment, citing the Wall Street Journal)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. Reserve funding standards, percent-funded benchmarks, lending requirements, and state reserve laws vary by jurisdiction and by the specific building, and the examples cited are reported situations, not legal conclusions. Statutes and lending guidelines referenced are current as of June 2026 and may be superseded. Consult a qualified real estate attorney, reserve specialist, or your lender for guidance specific to your situation.