In This Guide

Starting with loan applications dated on or after January 4, 2027, Fannie Mae requires a condo or co-op budget to fund replacement reserves at at least 15% of annual budgeted assessment income, up from the current 10%. A separate change on August 3, 2026 retires Limited Review for established condos, which pushes far more loans into the Full Review where this reserve test is applied. A board that funds reserves below the line, without a qualifying reserve study, can make its entire building non-warrantable, which means owners struggle to sell or refinance with a conventional loan.

A seller in your community accepts a strong offer. A week later the buyer's lender pulls the association budget, sees reserves funded at 9% of assessment income, and the deal collapses because the project no longer qualifies for a conventional loan. The board never heard the reserve line was a problem until it cost an owner a sale.

Your board adopts a budget every year, and the reserve contribution is one line on it. For most boards it has never been the line that triggers a phone call. That is about to change.

A reserve allocation that sits a few points too low does not just weaken your funding plan. Under Fannie Mae's revised project standards, it can render the whole project ineligible for conventional financing. When that happens, the consequences land on individual owners who had nothing to do with the budget vote: a seller whose buyer's loan falls through, an owner who cannot refinance out of a high rate, a unit that sits on the market while comparable buildings move. As of March 2025, more than 5,000 condo and co-op projects were on Fannie Mae's ineligible list, up from a few hundred before the 2021 Surfside collapse, according to Real Estate News.

The good news for boards and managers: this is a budget-cycle problem, and you still have one budget cycle to solve it. This guide explains exactly what the rule requires, the two dates that matter, and the concrete steps to get your project on the right side of the line before fall 2026 budgets are set.

What Is Changing, and When

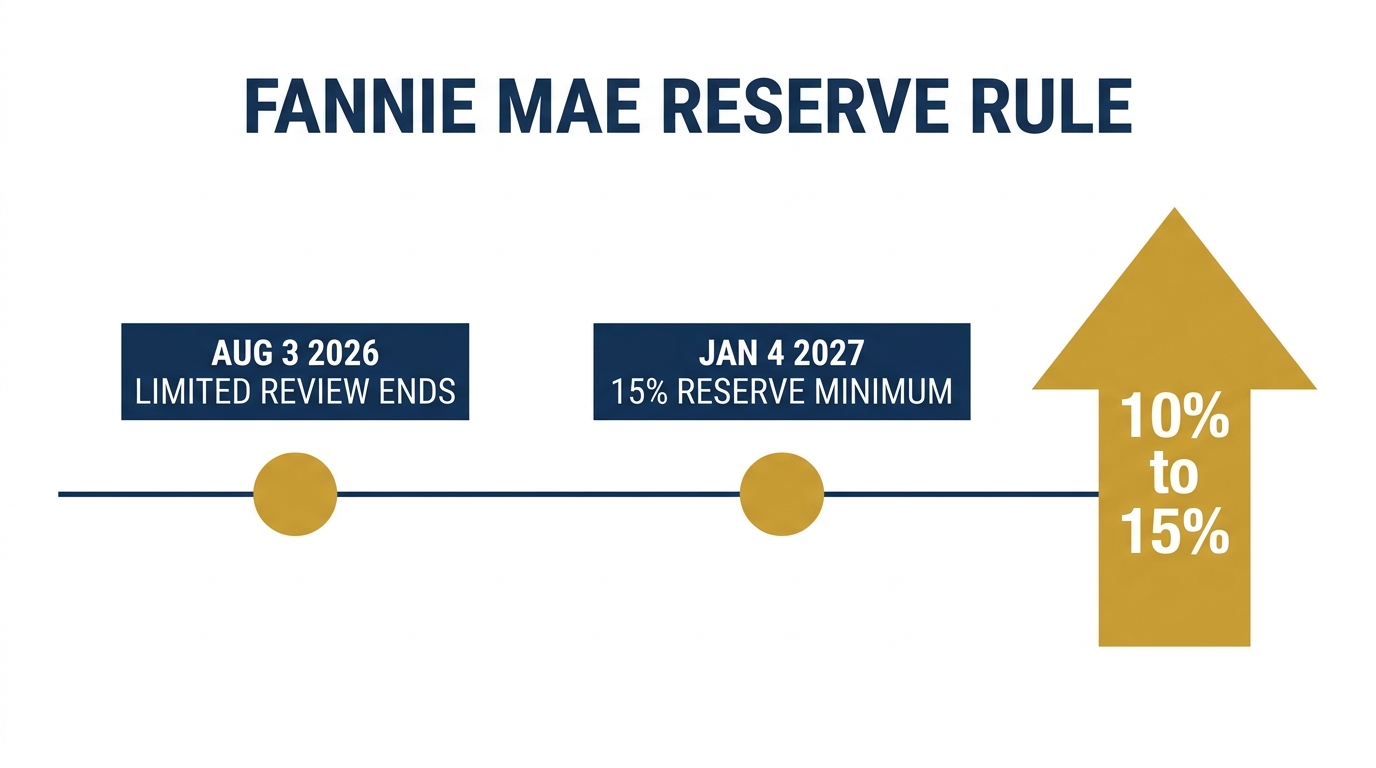

Fannie Mae's reserve minimum rises from 10% to 15% on January 4, 2027. Limited Review for established condos ends August 3, 2026.

The changes come from Fannie Mae Lender Letter LL-2026-03, issued March 18, 2026, which updates the project standards in the Selling Guide. Three effective dates matter, and they are not the same day:

| Effective date | What changes |

|---|---|

| July 1, 2026 | Updated property and flood insurance requirements take effect. |

| August 3, 2026 | Limited Review is retired for established condo projects, and the reserve study route can no longer rely on a baseline (near-zero) funding method. |

| January 4, 2027 | The minimum reserve allocation rises from 10% to 15% of annual budgeted assessment income, for loan applications dated on or after this date. |

Note that the trigger is the loan application date, not the closing or note date. A buyer who applies on January 3, 2027 falls under the old 10% rule; one who applies on January 4 falls under the new 15% rule. For a board, that means the budget you adopt for the 2027 fiscal year is the one a lender will measure against the higher bar.

What the Reserve Rule Actually Requires

The lender divides your budgeted reserve allocation by your annual budgeted assessment income. That figure must be at least 15% from January 2027.

The mechanics are specific, and getting the denominator right matters. Under Fannie Mae Selling Guide B4-2.2-02, a lender reviewing your budget divides the annual budgeted replacement reserve allocation by the annual budgeted assessment income (which includes regular common-expense fees). Today that result must be at least 10%. From January 4, 2027, it must be at least 15%.

The denominator is assessment income, not total expenses and not total assessments collected over time. Certain incidental income the association does not rely on for ongoing operations, maintenance, or capital improvements may be excluded from the calculation. In plain terms: if your community collects $1,000,000 a year in regular assessments, a 10% reserve line is $100,000 and a 15% line is $150,000. Closing that gap is a 50% increase to the reserve contribution itself, even though it is only five percentage points on paper.

Replacement reserves here mean money set aside for capital expenditures and deferred maintenance: roofs, elevators, paving, painting, mechanical systems, and the other major components that wear out on a schedule. Operating-budget line items do not count toward the reserve figure.

A few projects are exempt from the test entirely. Fannie Mae waives project review (and therefore the reserve requirement) for two-to-four-unit condo projects and for detached condo units, both new and established, under Selling Guide B4-2.1-02. Most planned-unit developments (PUDs) are also outside the condo reserve test. If your association is a typical mid-size or larger condo, though, the rule applies.

The August 2026 Change That Widens the Net

Retiring Limited Review pushes established condos into Full Review, where reserves, budget, delinquency, and litigation are all scrutinized.

The 15% number gets the headlines, but the August 3, 2026 change may reach more buildings sooner. Until now, many loans in established condo projects qualified for a Limited Review, a lighter process that did not put the full budget and reserve picture under the microscope. Once Limited Review is retired for established projects, those loans move to Full Review, the process in which the reserve test, delinquency rate, insurance, litigation, and special assessments are all examined.

The practical effect is that the reserve requirement becomes real for a much larger share of transactions in your building. A project that quietly underfunded reserves for years may have skated through on Limited Review loans. After August 3, 2026, that cushion is gone, and the budget gets read closely on more files, well before the 15% figure formally takes effect in January 2027.

Freddie Mac is making a parallel set of changes on a coordinated timeline, so a board should not assume a project that fails Fannie's test will pass Freddie's. Treat the two as moving together. (Confirm the current Freddie Single-Family Seller/Servicer Guide language with your lender, as the exact subsection wording is updated periodically.)

What Failing Costs Your Owners

A non-warrantable project forces buyers into portfolio or non-QM loans: bigger down payments, higher rates, a smaller buyer pool, lower prices.

When a project fails Fannie and Freddie eligibility, conventional financing comes off the table for units in the building. Buyers are pushed into portfolio or non-QM loans, which typically require larger down payments (commonly 20% to 30%) and carry higher interest rates, roughly 0.5% to 1.5% above conventional on portfolio products and often 2% to 4% higher on non-QM, according to 2025 lender data. The buyer pool shrinks to those who can secure specialty financing or pay cash.

The downstream effects are exactly what a board does not want to be responsible for: longer time on market, lower sale prices, and existing owners unable to refinance out of higher-rate loans. Real estate reporting on the ineligible-project list describes the result plainly as fewer qualified buyers, longer marketing times, and often lower sale prices. The damage is also concentrated geographically: Florida accounts for around 1,400 of the projects on Fannie Mae's ineligible list, followed by California and Colorado.

Underfunded reserves are not a fringe problem. An analysis of more than 100,000 reserve studies found that roughly 74% of associations are less than 70% funded, the threshold below which special-assessment risk climbs. A building that lets reserves drift while components age is the building most likely to face a surprise capital bill. Recent examples show the scale: at The Cricket Club in North Miami, special assessments reached as high as $134,000 per unit, and at Mediterranean Village in Aventura some owners were assessed up to $400,000. Outside Florida, residents of San Francisco's Millennium Tower were billed a $6.8 million special assessment in September 2023, levied at $10 per square foot, for their share of cost overruns (a structural foundation case rather than ordinary deferred maintenance, but the same lesson about what happens when a building's reserves cannot absorb a major project).

The Reserve Study Exception (and How It Changed)

A current reserve study can substitute for the flat 15%, but from August 2026 the budget must fund the study's highest recommended level.

There is an alternative to hitting the flat percentage. Fannie Mae allows a lender to rely on a reserve study in place of the 10% or 15% line item, provided the study was completed within three years of the date the lender approves the project and was prepared by an independent third party with reserve-study expertise (a credentialed reserve specialist, a construction engineer, or a CPA who specializes in reserve studies). The study must address the major components, their condition and remaining useful life, repair and replacement cost estimates, and the total annual contribution required.

This is where the August 3, 2026 change has teeth. Before, a project could lean on a reserve study that used a baseline (sometimes near-zero) funding method. After that date, when a study is used to satisfy the requirement, the budget must fund the study's highest recommended reserve allocation. A study that recommends a robust contribution no longer helps if the board funds far below it. For most well-run associations this is good news: a properly funded reserve study is the cleanest path to compliance and is more accurate than a blanket percentage, because it ties the contribution to your building's actual components.

If you want to see how a lender or buyer will read your numbers, the reserve study analyzer pulls out percent funded, the contribution trend, and special-assessment risk in one pass. For a plain-English primer, see what percent funded means and what an HOA reserve study is.

Where Your State Already Pushes You

Florida already mandates full structural reserve funding with no waiver. Most states only require a study, so Fannie's rule is the binding one.

In a handful of states, statute is already forcing reserves up, which means Fannie's requirement and state law point the same direction. In most states, no law requires a specific funding level, so Fannie's rule is effectively the only reserve mandate with real consequences, because it gates financing.

| State | Authority | What it requires |

|---|---|---|

| Florida | Fla. Stat. §718.112(2)(g); §553.899 | Structural Integrity Reserve Study for condo and co-op buildings three stories or higher. For budgets adopted on or after December 31, 2024, the structural reserves must be fully funded and cannot be waived or reduced. |

| California | Civ. Code §5550; §5551 (SB 326) | Reserve study at least every three years with annual review. Separate balcony and elevated-element inspections. AB 2050, a pending bill that would require a 30-year funding projection keeping reserves above zero (operative January 1, 2032 if enacted), passed the Assembly on May 11, 2026 and is now in the Senate. |

| Nevada | NRS 116.31152 | Reserve study at least every five years, reviewed annually, with funding-plan adjustments. Reserve specialists must hold a state permit. |

| Washington | RCW 64.34.380 | Reserve study with an update based on a visual site inspection at least every three years by an independent professional. |

| Colorado | C.R.S. §38-33.3-209.5 | Must adopt a written reserve-study policy covering whether and when a study is done and how reserves are funded. No fixed funding level. |

Florida is the outlier: for buildings subject to a Structural Integrity Reserve Study, owners can no longer vote to waive or underfund the structural components. California, Nevada, and Washington mandate the study and its update cycle but generally still leave the funding level to the board (California's AB 2050 would change that if it becomes law). In every other state, the budget is the board's call, which is precisely why Fannie's 15% line ends up being the rule with the sharpest teeth.

The Board Playbook Before Budget Season

Audit the current reserve percentage, commission or update a reserve study, and fund the higher line in the fall 2026 budget.

Most associations set their annual budget in the fall, so for practical purposes a board has one budget cycle to absorb this change before the 2027 fiscal year. Boards that wait until late 2026 give owners the least room to adjust to a higher contribution. Here is the sequence that gets a project compliant:

- Audit your current reserve percentage. Divide this year's budgeted reserve allocation by your annual budgeted assessment income. If the result is under 15% and you do not have a qualifying reserve study, you have a gap to close.

- Commission or update a reserve study. Make sure it is within three years and performed by an independent qualified professional. This is the single most useful compliance document, and it unlocks the alternative to the flat 15%. Remember that after August 3, 2026, using the study means funding its highest recommended allocation, not a baseline minimum.

- Fund the reserve line in the budget. Moving from 10% to 15% is a 50% increase to that contribution. Options include a dues increase, trimming or deferring nonessential operating spending, or a structured funding plan or association loan. Document the plan in your minutes.

- Drop any baseline or near-zero funding method. It no longer satisfies the requirement under any circumstances.

- Keep your documents lender-ready. Full Review means lenders request budgets, reserve studies, minutes, insurance, and inspection reports. A board that can produce a clean package keeps its owners' loans moving.

A dues increase is never a popular vote. But framed correctly, it is a protection: a building that funds reserves properly stays warrantable, which protects every owner's ability to sell and refinance at conventional terms. The alternative, a starved reserve fund and a non-warrantable label, costs owners far more in lost value and stranded sales than the contribution ever would. For the underlying warrantability mechanics, see Fannie and Freddie Condo Rules 2026 and the financing red flags buyers watch for in the HOA red flags that kill FHA and VA loans.

Frequently Asked Questions

When does Fannie Mae's 15% reserve rule take effect?

It applies to loan applications dated on or after January 4, 2027. The minimum replacement reserve allocation rises from 10% to 15% of annual budgeted assessment income, under Fannie Mae Lender Letter LL-2026-03. The trigger is the application date, not the closing date.

How is the reserve percentage calculated?

A lender divides the association's annual budgeted replacement reserve allocation by its annual budgeted assessment income, which includes regular common-expense fees. That figure must be at least 10% today and at least 15% from January 4, 2027, under Fannie Mae Selling Guide B4-2.2-02.

Can a reserve study replace the 15% requirement?

Yes. Fannie Mae lets a lender rely on a reserve study completed within three years by an independent qualified professional instead of the flat percentage. From August 3, 2026, when a study is used, the budget must fund the study's highest recommended reserve allocation, not a baseline minimum.

What happens if our building fails the reserve test?

The project can become non-warrantable, meaning conventional Fannie and Freddie financing is unavailable for its units. Buyers are pushed into portfolio or non-QM loans with larger down payments and higher rates, which shrinks the buyer pool and can lower unit values and lengthen time on market. Existing owners may also be unable to refinance.

Why does the August 3, 2026 date matter if the 15% rule starts in January 2027?

On August 3, 2026, Fannie Mae retires Limited Review for established condo projects, sending more loans to Full Review, where the reserve, budget, delinquency, and litigation tests are applied. So the reserve requirement effectively reaches more transactions months before the 15% figure formally takes effect.

Are any projects exempt from the reserve requirement?

Yes. Fannie Mae waives project review, and therefore the reserve test, for two-to-four-unit condo projects and for detached condo units, both new and established, under Selling Guide B4-2.1-02. Most planned-unit developments are also outside the condo reserve test. Confirm your project type with your lender.

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

Sources & References

- Fannie Mae Lender Letter LL-2026-03 (10% to 15% reserve change, Limited Review retirement, effective dates)

- Fannie Mae Selling Guide B4-2.2-02 (Full Review reserve calculation and reserve study route)

- Fannie Mae Selling Guide B4-2.1-02 (project review waivers for 2-4 unit and detached condos)

- Real Estate News (more than 5,000 projects on Fannie Mae ineligible list; geographic concentration)

- Association Reserves (74% of associations less than 70% funded)

- NBC Bay Area (Millennium Tower $6.8M special assessment, September 2023)

- Axios Miami (Cricket Club, North Miami special assessment ~$134,000 per unit)

- Brosda & Bentley (Mediterranean Village, Aventura assessments up to $400,000)

- Cal. Civ. Code §5550 (California reserve study requirement)

- California AB 2050 (pending 30-year reserve funding projection; passed Assembly May 11, 2026)

- Reserve Advisors (Florida SIRS funding and no-waiver requirements)

- Percent Funded thresholds (70%+ strong, 30% or below weak)

- X2 Mortgage (non-warrantable rate and down-payment differentials, 2025)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, lending, or real estate advice. Fannie Mae and Freddie Mac project standards, effective dates, and state reserve statutes change frequently, and condominium and planned-community rules differ within the same state. Guidance referenced is current as of May 2026 and may be superseded. Boards and managers should confirm current requirements with their lender and a qualified community association attorney or reserve professional before setting a budget.