In This Guide

HOA financial health determines whether a condo is a sound investment or a money pit. Five numbers in HOA documents predict your risk: percent funded, delinquency rate, reserve contribution percentage, components past useful life, and special assessment history. Over 70% of HOAs are underfunded.

You found the perfect condo. Great neighborhood, right price, clean inspection report. Six months later, a letter arrives: "Special Assessment: $85,000 due within 90 days for structural repairs."

This happens more often than most buyers realize. Over 70% of homeowners associations are underfunded, according to Association Reserves' analysis of over 100,000 reserve studies. That means the majority of condo buildings in America do not have enough money saved to cover the repairs they already know are coming.

The inspection checked the physical condition of your unit. But nobody checked the financial condition of the building. And financial problems in an HOA don't just affect common areas. They affect your mortgage eligibility, your property value, your monthly costs, and your ability to sell.

The good news: all of this information is available before you buy. It's sitting in the reserve study, the operating budget, the meeting minutes, and the CC&Rs. You just need to know what to look for.

This guide walks you through the five numbers that predict HOA financial health, how they connect to each other, and exactly what to check before you close. It's based on our analysis of 1,900+ HOA documents across the United States.

Why HOA Financial Health Matters More Than Location

A building's financial health determines your total cost of ownership. Underfunded reserves lead to special assessments, financing restrictions, and declining property values.

When you buy a condo, you're not just buying a unit. You're buying a share of the entire building. If the building needs a $5 million roof replacement and the reserve fund has $500,000, every owner shares the $4.5 million shortfall. That's the special assessment.

Financial health affects everything downstream:

- Your monthly costs. Underfunded buildings eventually raise fees or levy assessments. Buildings that plan ahead keep costs predictable.

- Your mortgage. Lenders check HOA finances before approving loans. A building that crosses key thresholds becomes non-warrantable, cutting off conventional financing.

- Your property value. When a building can't get conventional financing, the buyer pool shrinks to cash buyers. Prices drop 10-25%.

- Your ability to sell. Financial problems compound over time. A building that's struggling today will be harder to sell tomorrow.

A beautiful unit in a financially distressed building is a worse investment than an average unit in a well-managed one. The numbers in the HOA documents tell you which one you're looking at.

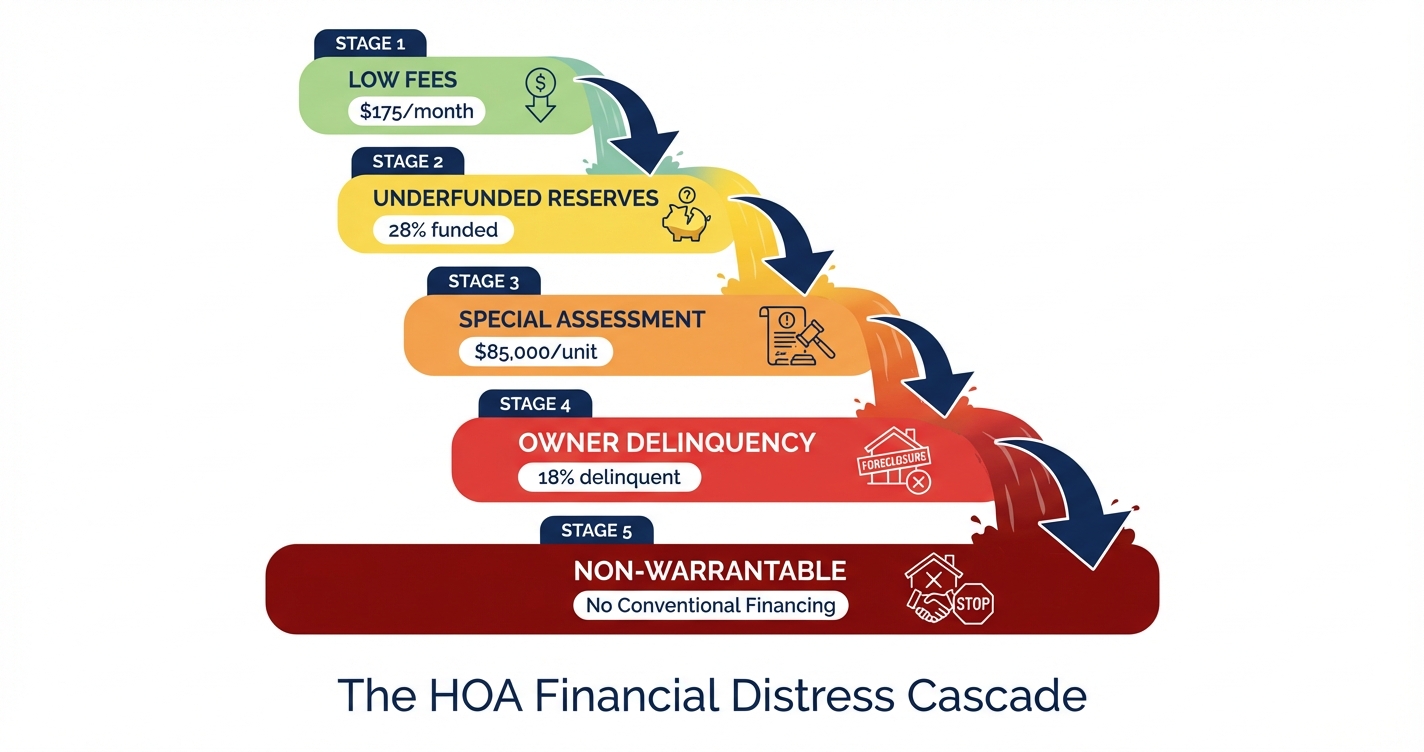

The Financial Health Cascade: How Small Problems Become Six-Figure Crises

HOA financial distress follows a predictable pattern: low fees lead to underfunded reserves, which lead to special assessments, which trigger delinquencies, which make the building non-warrantable.

Financial problems in HOAs don't appear suddenly. They follow a cascade that can take years to unfold. Understanding this chain helps you spot trouble early, before it becomes a crisis.

The HOA financial distress cascade: each stage makes the next stage more likely

Stage 1: Fees stay artificially low. Boards keep monthly dues low because owners complain about increases. The reserve fund gets a fraction of what it needs. This feels fine for years. The building looks maintained. The budget balances on paper.

Stage 2: Reserves fall behind. As years pass, the gap between what the building needs and what it has saved grows. The percent funded level drops below 70%, then below 50%, then below 30%. Major components age toward end of life without funding to replace them.

Stage 3: A special assessment hits. When a roof fails, an elevator breaks, or a structural inspection reveals problems, the board has no choice. They levy a special assessment of $20,000 to $400,000+ per unit. Owners get weeks or months to pay.

Stage 4: Some owners can't pay. Large assessments push some owners into delinquency. The delinquency rate climbs. The remaining owners bear a larger share of the burden.

Stage 5: The building becomes non-warrantable. When delinquency crosses 15%, Fannie Mae, Freddie Mac, FHA, and VA all stop backing mortgages in that building. Conventional financing disappears. Only cash buyers or portfolio lenders remain. Property values drop 10-25%.

Each stage makes the next stage worse. Declining property values trigger more defaults, which raise delinquency further, which makes financing harder, which drives prices down more. In Florida's condo market, this cycle has played out across hundreds of buildings since 2022.

The 5 Numbers That Tell You Everything

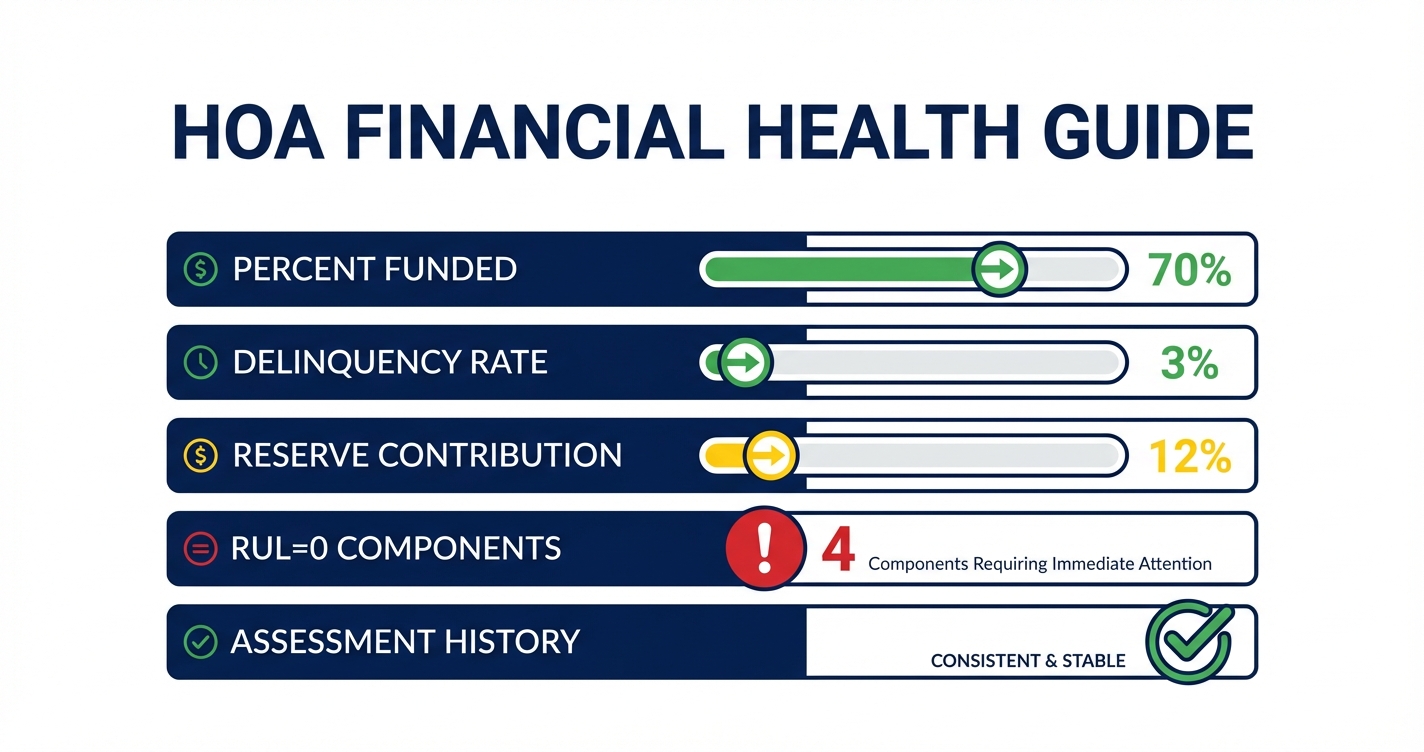

Five metrics in HOA documents predict financial health: percent funded, delinquency rate, reserve contribution percentage, RUL=0 component count, and special assessment history.

You don't need to read every page of every document. These five numbers give you 80% of the picture. Each one tells you something different, and together they reveal whether the building is financially sound or headed for trouble.

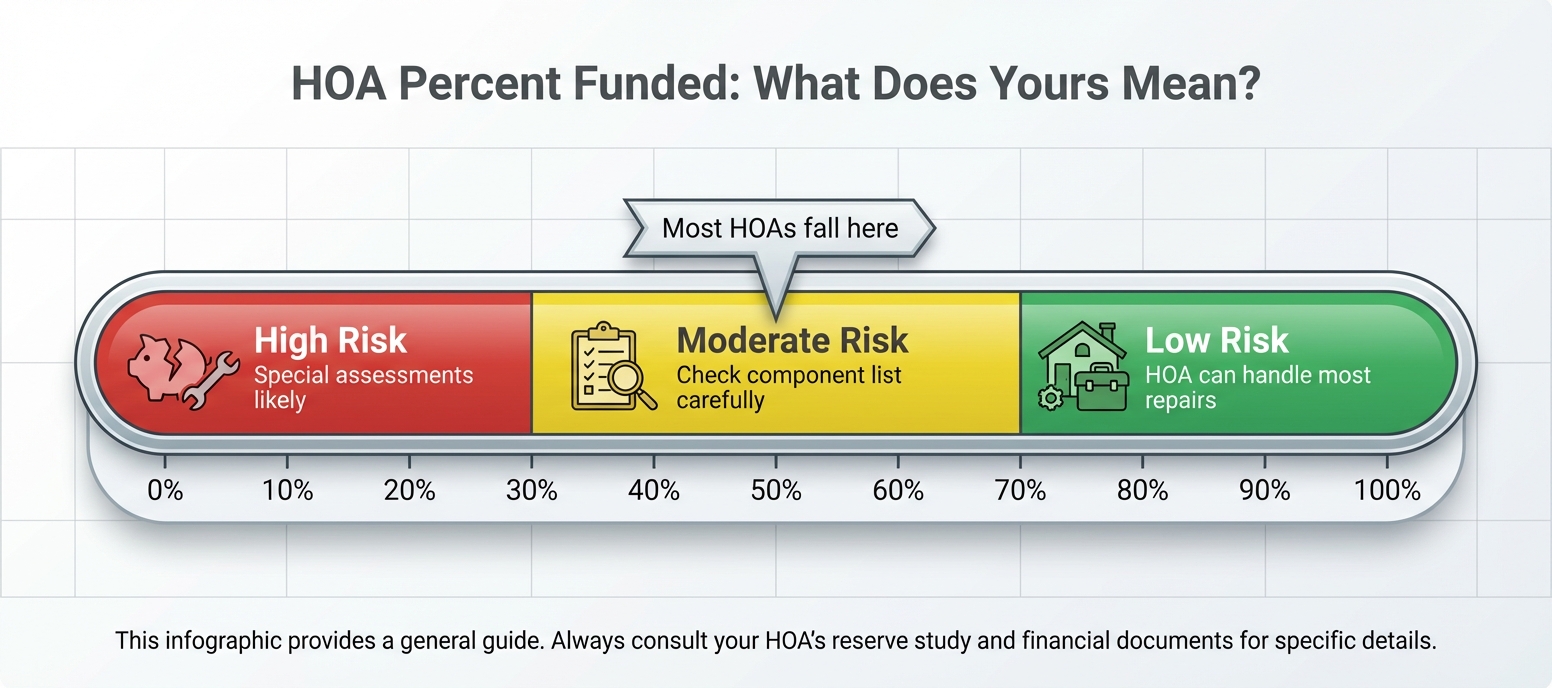

1. Percent Funded: The Single Most Important Number

What it is: The ratio of the money currently in the reserve fund to the money that should be there based on the age and condition of building components. Calculated as (Current Reserve Balance ÷ Fully Funded Balance) × 100.

Where to find it: Page 2-3 of the reserve study, under headings like "Percent Funded," "Funding Level," or "Reserve Fund Status."

Industry benchmarks for percent funded levels (source: Community Associations Institute)

What the numbers mean:

- 70%+ (Strong): The building is saving adequately. Special assessment risk is low.

- 30-70% (Fair): Some shortfall exists. Check how fast contributions are closing the gap. Special assessments are possible.

- Below 30% (Weak): Critically underfunded. Special assessments are likely. Proceed with extreme caution.

Important caveat: Percent funded alone doesn't tell the full story. A building at 40% funded with no major components due for replacement in the next decade is in better shape than one at 75% funded with a $1.2 million elevator replacement due next year. Always check what's coming due alongside the funding level.

For a deeper breakdown of funding thresholds and how context changes the picture, see our full guide: What Is a Good Percent Funded for an HOA? For the basics, see What Is Percent Funded?

2. Delinquency Rate: The Financing Killer

What it is: The percentage of units that are 60+ days past due on HOA assessments.

Where to find it: The HOA questionnaire (sometimes called a "condo questionnaire" or "lender questionnaire"), accounts receivable aging report, or by asking the management company directly.

The critical threshold: 15%. When delinquency hits 15%, Fannie Mae, Freddie Mac, FHA, and VA all classify the building as non-warrantable. That means no conventional mortgages. Buyers need cash or portfolio loans with higher rates and larger down payments. As of 2024, 1,438 Florida buildings had already crossed this line.

Delinquency below 5% is healthy. Between 5-10% warrants investigation. At 10-14%, proceed with caution. At 15%+, the building is non-warrantable and conventional financing may not be available to your future buyer when you go to sell.

For the full mechanics of how delinquency kills deals, see: HOA Delinquency Rate: The Number That Can Kill Your Condo Purchase. For the definition, see What Is the HOA Delinquency Rate?

3. Reserve Contribution Percentage: Is the Building Saving Enough?

What it is: The percentage of the annual operating budget allocated to the reserve fund.

Where to find it: The operating budget, usually a line item for "Reserve Contribution" or "Transfer to Reserves."

What to look for: A healthy building allocates 15-40% of its annual budget to reserves. Currently, Fannie Mae and Freddie Mac require at least 10%, but that minimum is rising to 15% on January 4, 2027. Buildings below the new threshold will face financing restrictions.

This number matters because percent funded is a snapshot. Contribution percentage tells you the trend. A building at 50% funded but contributing 25% annually is recovering. A building at 60% funded but contributing 8% is falling further behind. The reserve study should show a recommended contribution level. Compare the actual contribution to that recommendation.

When a building keeps fees low by shortchanging reserve contributions, you end up in Stage 1 of the cascade described above. For more on how this plays out, see: Are Low HOA Fees a Red Flag?

4. Components Past End of Useful Life (RUL=0)

What it is: The count of building components that have exceeded their estimated useful life and are due for replacement now.

Where to find it: The component inventory section of the reserve study. Look for "Remaining Useful Life" (RUL) columns showing 0 years.

What it tells you: Every component at RUL=0 is a ticking clock. It hasn't been replaced yet, which usually means the money wasn't there, or the board chose to defer it. One or two items at RUL=0 is common, especially minor items. Three or more suggests a pattern of deferred maintenance. In our analysis of 38 Florida SIRS reports, buildings with lower percent funded levels consistently had more components past their useful life.

The key question is cost. A $5,000 pool resurfacing at RUL=0 is different from a $500,000 roof at RUL=0. Check the replacement cost estimate alongside the count. For a walkthrough of reading the full reserve study, see: How to Read a Reserve Study in 5 Minutes. For the basics, see What Is an HOA Reserve Study?

5. Special Assessment History: What the Building Has Already Asked For

What it is: The record of past special assessments, including amounts, reasons, and frequency.

Where to find it: Board meeting minutes, the estoppel certificate, and by asking the management company. The estoppel letter will list any pending or recently completed assessments.

What to look for: A building with no special assessments in the last 10 years and strong reserves is the ideal. One large assessment tied to a specific event (like a storm) is different from a pattern of assessments every few years. Repeated assessments signal chronic underfunding.

Also check whether any assessment is currently pending or has been discussed but not yet voted on. Board minutes are the best source for this. A board that's been discussing a $50,000 per unit assessment for three meetings is close to levying it, even if the vote hasn't happened yet.

For more on how assessments work, what they cost, and who pays at closing, see: Understanding HOA Special Assessments and Who Pays the HOA Special Assessment at Closing? For the definition, see What Is an HOA Special Assessment?

Special Assessments: The Biggest Financial Risk for Condo Buyers

Special assessments range from $5,000 to over $400,000 per unit. They are mandatory, often due within 90 days, and may not show up on a standard home inspection.

Of all the financial risks in HOA properties, special assessments are the most consequential. They can hit without warning, require large payments on short timelines, and are legally enforceable. The HOA can place a lien on your unit and, in many states, initiate foreclosure if you don't pay.

Five warning signs that a special assessment is coming

Cost ranges depend on the repair:

- $5,000-$25,000: Roof replacement, painting, pool resurfacing

- $10,000-$50,000: Plumbing overhauls, parking garage repairs, elevator modernization

- $50,000-$400,000+: Concrete restoration, structural remediation, full SIRS compliance in Florida

Who pays when you're buying? The general rule is that assessments levied before closing are the seller's responsibility, and assessments levied after closing are the buyer's. But the purchase contract can override this, and three states (Florida, Hawaii, and Washington) have joint liability laws that create additional complexity. The estoppel certificate is your best protection. It documents exactly what the seller owes at closing.

For the full state-by-state breakdown of who pays and how to protect yourself, see: Who Pays the HOA Special Assessment at Closing?

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

When Low HOA Fees Are Actually a Red Flag

Artificially low HOA fees are the most common starting point for financial distress. The national median is $135/month, but adequacy depends on building age, size, and amenities.

Low fees feel like a benefit when you're shopping. They're often presented as a selling point. But low fees in a building with a pool, elevator, underground parking, and a 40-year-old roof should raise questions, not excitement.

HOA budgets have two parts: the operating fund (day-to-day expenses like landscaping, insurance, management) and the reserve fund (long-term savings for major repairs). When boards keep fees low, the reserve fund is usually what gets cut. The building still looks fine today. The crisis shows up 5-10 years later when major components fail and there's no money to fix them.

Real-world examples:

- Champlain Towers South (Surfside, FL): Reserves funded at just 6.9% before the 2021 collapse. Board had repeatedly deferred maintenance to keep fees low. Estimated remediation costs were $80,000-$336,000 per unit before the building fell.

- Harbor Towers (Boston): $75.6 million assessment for deferred mechanical and structural repairs. Individual owner assessments of $120,000-$400,000.

The red flag isn't low fees by themselves. It's low fees combined with aging infrastructure, underfunded reserves, no recent reserve study, or a history of deferred maintenance votes in meeting minutes. For the full breakdown of what to watch for, see: Are Low HOA Fees a Red Flag?

How HOA Finances Affect Your Mortgage

Lenders evaluate HOA finances as part of condo mortgage approval. Buildings that fail financial thresholds become non-warrantable, eliminating conventional financing.

When you apply for a mortgage on a condo, the lender isn't just evaluating you. They're evaluating the building. Fannie Mae, Freddie Mac, FHA, and VA each have financial requirements the HOA must meet for the loan to be approved.

What lenders check:

- Delinquency rate: Must be under 15% (hard cutoff for all agencies)

- Reserve budget allocation: Currently 10% minimum, rising to 15% on January 4, 2027

- Insurance coverage: Adequate master policy with required coverage types

- Litigation status: Active lawsuits can trigger additional underwriting scrutiny

- Single-entity ownership: No more than 20% of units owned by one entity (Fannie Mae) or 10% for FHA

Key changes in 2026-2027: Fannie Mae is eliminating the Limited Review process, which previously allowed some loans to bypass full project approval. Starting August 3, 2026, all condo loans will require full project review. And the reserve allocation minimum jumps to 15% on January 4, 2027. Buildings currently hovering at 10-14% will need to increase contributions or risk losing financing eligibility.

For the complete breakdown of how HOA documents affect loan approval, see: Can Your Condo Get Financed? and 2026 Fannie Mae Condo Rules.

The Florida Factor: A Case Study in What Goes Wrong

Florida's post-Surfside SIRS mandate is forcing thousands of buildings to confront decades of deferred maintenance. The result: assessments up to $400,000 per unit and condo values down 9.9% statewide.

Florida is the most extreme example of the financial health cascade playing out in real time. After the Champlain Towers South collapse in 2021, the state passed Senate Bill 4-D requiring Structural Integrity Reserve Studies (SIRS) for all buildings three stories or taller. Reserve fund waivers were banned starting January 1, 2026.

The result: buildings that had been waiving reserves for decades suddenly had to fund them. Our analysis of 38 Florida SIRS documents covering approximately 2,000 units found:

- 30.8% of associations were underfunded below 50%

- 26.9% were critically underfunded below 30%

- Average building age: 41 years, with 79% over 30 years old

- 45% of components were due for replacement within 10 years

- $10.1 million in total replacement costs across analyzed associations

The market impact has been severe. Florida condo values dropped 9.9% in 12 months. Over 90% of South Florida condos are selling below asking price. Nearly 70% close below their original list price. Buildings with the largest assessment burdens have seen the steepest declines.

This isn't just a Florida story. It's a preview of what happens when decades of deferred maintenance meet mandatory compliance. Other states are watching Florida closely. Similar legislation has been proposed in several markets.

For the full Florida analysis, see: Florida Condo Crisis 2026. For SIRS report details, see: Florida SIRS Reports Explained.

Red Flags That Predict Financial Trouble

After analyzing 1,900+ HOA documents, five patterns consistently predict financial distress: underfunded reserves, deferred maintenance, low fees, vague CC&R language, and active litigation.

Some problems show up in the numbers. Others show up in the language and patterns across multiple documents. Here are the red flags we see most often:

In the reserve study:

- Percent funded below 30%

- Three or more components at RUL=0

- Actual contributions significantly below the study's recommended contributions

- Study is more than 5 years old (or no study exists at all)

In the meeting minutes:

- Repeated votes to defer maintenance

- Discussion of special assessments across multiple meetings

- Manager or vendor turnover

- Owner complaints about deferred repairs

In the CC&Rs and budget:

- Vague special assessment language with no spending caps or vote requirements

- Reserve contribution below 10% of annual budget

- Insurance premiums spiking (often a sign of claims history or aging infrastructure)

- Active or threatened litigation

One red flag is a concern. Two is a pattern. Three or more means you should negotiate hard on price or walk away. For the full data-driven analysis, see: 5 HOA Red Flags That Predict Special Assessments.

Your HOA Financial Health Checklist

Use this checklist during your due diligence period to evaluate any condo or HOA property before closing.

Documents to Request

- Most recent reserve study (should be less than 3 years old)

- Operating budget for the current year

- Board meeting minutes from the last 12-24 months

- CC&Rs (Covenants, Conditions & Restrictions)

- Estoppel certificate (shows what the seller owes and any pending assessments)

- HOA questionnaire / lender questionnaire (includes delinquency rate)

- Insurance declarations page (master policy coverage and premiums)

Numbers to Check

| Metric | Healthy | Caution | Danger |

|---|---|---|---|

| Percent Funded | 70%+ | 30-70% | Below 30% |

| Delinquency Rate | Under 5% | 5-14% | 15%+ |

| Reserve Contribution | 15-40% of budget | 10-14% | Below 10% |

| RUL=0 Components | 0-1 (minor) | 2 (check cost) | 3+ or any major system |

| Special Assessments | None in 10 years | One (event-driven) | Repeated or pending |

| Reserve Study Age | Under 3 years | 3-5 years | Over 5 years or none |

Questions to Ask

- Are there any special assessments currently pending or under discussion?

- What was the last special assessment, and how much was it?

- When was the most recent reserve study completed? Who did it?

- Is the building compliant with all state structural inspection requirements?

- What major repairs or capital projects are planned in the next 3-5 years?

- Has the board voted to waive or reduce reserve contributions in the last 5 years?

- Are there any active lawsuits involving the HOA?

If you want to speed up this process, our free tools can analyze CC&Rs, reserve studies, and meeting minutes in minutes. They flag exactly these issues automatically.

Get Your HOA Documents Analyzed

GoverningDocs analyzes CC&Rs, reserve studies, and meeting minutes — identifying red flags, restrictions, and financial risks so you can buy with confidence. Free. No signup required.

Related Articles

Deep Dives (Spoke Articles)

- Understanding HOA Special Assessments: $5K to $400K Risks

- How to Read a Reserve Study in 5 Minutes

- HOA Delinquency Rate: The Number That Can Kill Your Condo Purchase

- Who Pays the HOA Special Assessment at Closing?

- Are Low HOA Fees a Red Flag?

- What Is a Good Percent Funded for an HOA?

- 5 HOA Red Flags That Predict Special Assessments

Quick Reference

- What Is Percent Funded?

- What Is the HOA Delinquency Rate?

- What Is an HOA Special Assessment?

- What Is an HOA Reserve Study?

Financing & Market

- Can Your Condo Get Financed? How HOA Documents Affect Mortgage Approval

- 2026 Fannie Mae Condo Rules: Reserves Up to 15%, Limited Review Gone

- Florida Condo Crisis 2026

Frequently Asked Questions

How do I check an HOA's financial health before buying?

Request the reserve study, operating budget, meeting minutes, and estoppel certificate during your due diligence period. Check the five key numbers: percent funded (target 70%+), delinquency rate (must be under 15%), reserve contribution percentage (should be 15-40% of budget), RUL=0 component count (fewer is better), and special assessment history (none is ideal).

What percent funded is considered healthy for an HOA?

The industry standard is 70% or higher. Below 30% is considered critically underfunded with a high likelihood of special assessments. However, context matters. Check what major components are coming due in the next 5-10 years alongside the funding percentage. A building at 50% funded with nothing major due soon may be safer than one at 65% with a $2 million roof replacement next year.

Can an HOA's financial problems affect my mortgage?

Yes. Fannie Mae, Freddie Mac, FHA, and VA all evaluate HOA finances before approving condo mortgages. If the building's delinquency rate exceeds 15%, it becomes non-warrantable and conventional financing is unavailable. Starting January 4, 2027, buildings must also allocate at least 15% of their budget to reserves (up from the current 10% minimum).

What is the HOA delinquency death spiral?

When large special assessments cause some owners to stop paying, delinquency rises. If it crosses 15%, the building becomes non-warrantable. Conventional financing disappears, property values drop 10-25%, which causes more owners to default or sell at a loss. The remaining owners bear a larger share of expenses. This cycle can accelerate rapidly once it starts.

Are low HOA fees a good thing?

Not necessarily. Low fees often mean the building is underfunding its reserves. Over 70% of HOAs are underfunded according to industry data. The national median fee is $135 per month, but adequacy depends on building age, size, amenities, and location. Low fees in a building with aging infrastructure and minimal reserve contributions is a major red flag.

Who pays if a special assessment is levied during a sale?

Generally, assessments levied before closing are the seller's responsibility and those after closing are the buyer's. But the purchase contract can override this. Three states (Florida, Hawaii, Washington) have joint liability provisions. Always request an estoppel certificate, which documents exactly what is owed at the time of closing.

What documents should I request for HOA due diligence?

At minimum: the reserve study (less than 3 years old), current operating budget, 12-24 months of board meeting minutes, CC&Rs, estoppel certificate, HOA/lender questionnaire, and insurance declarations page. Together, these documents contain all five financial health metrics and reveal any red flags.

Sources & References

- Community Associations Institute (CAI) : National Reserve Study Standards

- Association Reserves : National Database of 100,000+ Reserve Studies (1986-2025)

- Fannie Mae Selling Guide B4-2.1-03 : Project Eligibility: Delinquency and Budget Allocation Requirements

- Freddie Mac Seller/Servicer Guide Section 5701.5 : Condominium Project Requirements

- FHA Single Family Housing Policy Handbook (HUD 4000.1) : Condominium Project Approval

- Florida Senate Bill 4-D (2022) : Structural Integrity Reserve Study Requirements

- GoverningDocs Analysis of 38 Florida SIRS Documents (2025-2026) : 1,730 pages, ~2,000 units

- GoverningDocs Analysis of 1,900+ HOA Documents (2024-2026)

- HOAstart Annual Report (2026) : National HOA Funding Levels Survey

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. HOA financial conditions vary by building, location, and management. Consult a qualified real estate attorney or financial advisor for guidance specific to your situation.