In This Guide

A real estate attorney typically charges $300 to $1,500 to review a condo or HOA document package, billed at roughly $150 to $500 per hour for one to three hours, or folded into a flat closing fee. That buys legal expertise on restrictions and liability, but most attorneys do not analyze reserve funding or special-assessment risk in depth. This guide breaks down the real cost, what the fee does and does not cover, and the cheaper options, from a $595 financial-review service to free AI to a $39 purpose-built tool.

You are under contract on a condo, and a few days later the disclosure packet lands: CC&Rs, bylaws, a budget, a balance sheet, a reserve study, two years of meeting minutes, an insurance certificate, and a resale or estoppel certificate. It can run several hundred pages. Your agent says you should "have someone look at it." A local real estate attorney quotes you something in four figures.

So you face a real question with a ticking clock behind it. Many states give the association only days to deliver these documents, which leaves you a short window to review them before contingencies expire. Do you pay an attorney to read the whole stack? Skim it yourself and hope? There is a sensible middle, but it helps to first understand exactly what an attorney costs, what that money does and does not buy, and where the cheaper options actually stand.

How Much Does an Attorney Review Actually Cost?

Expect $300 to $1,500. Real estate attorneys bill about $150 to $500 per hour, and a focused document review usually takes one to three hours, or is bundled into a flat closing fee.

Real estate attorneys generally bill one of two ways. The first is hourly. National rates run roughly $150 to $500 per hour, with an average around $377, lower for simpler matters and higher in expensive metros like New York, San Francisco, and Washington, D.C. A focused review of an HOA document package typically takes one to three hours, which puts a standalone review in the low hundreds to around $600.

The second is a flat fee. In states where an attorney handles the closing, residential representation is commonly quoted at $500 to $1,500, often $750 to $1,250, and a document review may be included in that package rather than priced separately. So the honest range for a buyer is about $300 to $1,500, depending on whether you are paying for a standalone review or one bundled into full representation, and on where you live.

Geography drives whether you even cross paths with an attorney. In roughly a dozen to fifteen states, including New York, Georgia, South Carolina, Massachusetts, Connecticut, North Carolina, and Virginia, an attorney is customary or required at closing, so adding a document review is natural. In escrow and title states like California, Arizona, Florida, Texas, Washington, Nevada, and Colorado, no attorney is required, so you would have to seek one out and pay for the review as a separate, deliberate step. That extra friction is a big reason buyers in those states often skip professional review entirely.

What an Attorney Review Does and Does Not Cover

Attorneys focus on legal exposure: restrictions, owner obligations, and litigation. Reserve adequacy and special-assessment math are a different skill set and often fall outside the review.

An attorney earns the fee on the legal side of the package. A good one reads the governing documents for use and leasing restrictions, pet and architectural rules, owner rights and obligations, amendment and voting provisions, and any language that could limit how you use or finance the property. They flag pending or threatened litigation and the legal exposure that comes with it, and they can interpret an ambiguous covenant in a way a layperson cannot.

What a legal review frequently does not include is a rigorous read of the association's finances. Judging whether a reserve fund is dangerously thin, whether the contribution rate keeps pace with the reserve study, or whether a special assessment is quietly building in the minutes is actuarial and financial analysis, not legal work, and many real estate attorneys neither do it nor price for it. That gap matters, because for most buyers the expensive surprises are financial: a special assessment, an underfunded reserve, or a building that no longer qualifies for a conventional loan. An attorney can tell you whether the rules are enforceable. Whether the money is there is a separate question you still have to answer.

What You Are Really Trying to Catch

The costly risks hide in the financials: underfunded reserves, looming special assessments, rental caps, and loss of conventional financing, often telegraphed pages before they become official.

Before you decide what to pay, it helps to know what a review is supposed to find. The risks that actually cost buyers money cluster in a few places:

- Underfunded reserves. Check percent funded, the reserve balance divided by the fully funded balance. By the standards Association Reserves uses, above 70% is strong, 30% to 70% is fair, and below 30% is weak and at real risk of a special assessment. Roughly 34% of associations sit in that weak band.

- Looming special assessments. A major one rarely appears out of nowhere. It is usually discussed in board minutes and foreshadowed in the budget for months before it is formally levied. The worst case is a cautionary tale: Champlain Towers South in Surfside was about 6.9% funded, and the special assessment it faced ran from roughly $80,000 to over $336,000 per unit.

- Rental restrictions. A cap on rentals or owner-occupancy can limit your ability to rent the unit later and can affect financing.

- Loss of conventional financing. If a project lands on the Fannie Mae and Freddie Mac ineligibility list, around 5,175 projects as of early 2025, conventional loans dry up for you and for every future buyer. The bar is also rising: Fannie's reserve-funding requirement climbs from 10% to 15% of budgeted assessment income for loan applications dated on or after January 4, 2027, and the Limited Review path closes August 3, 2026.

Notice how many of these are financial rather than strictly legal. That is the core reason the most expensive option is not automatically the most complete one. For more depth, see our complete guide to HOA financial health and the new Fannie Mae 15% reserve rule.

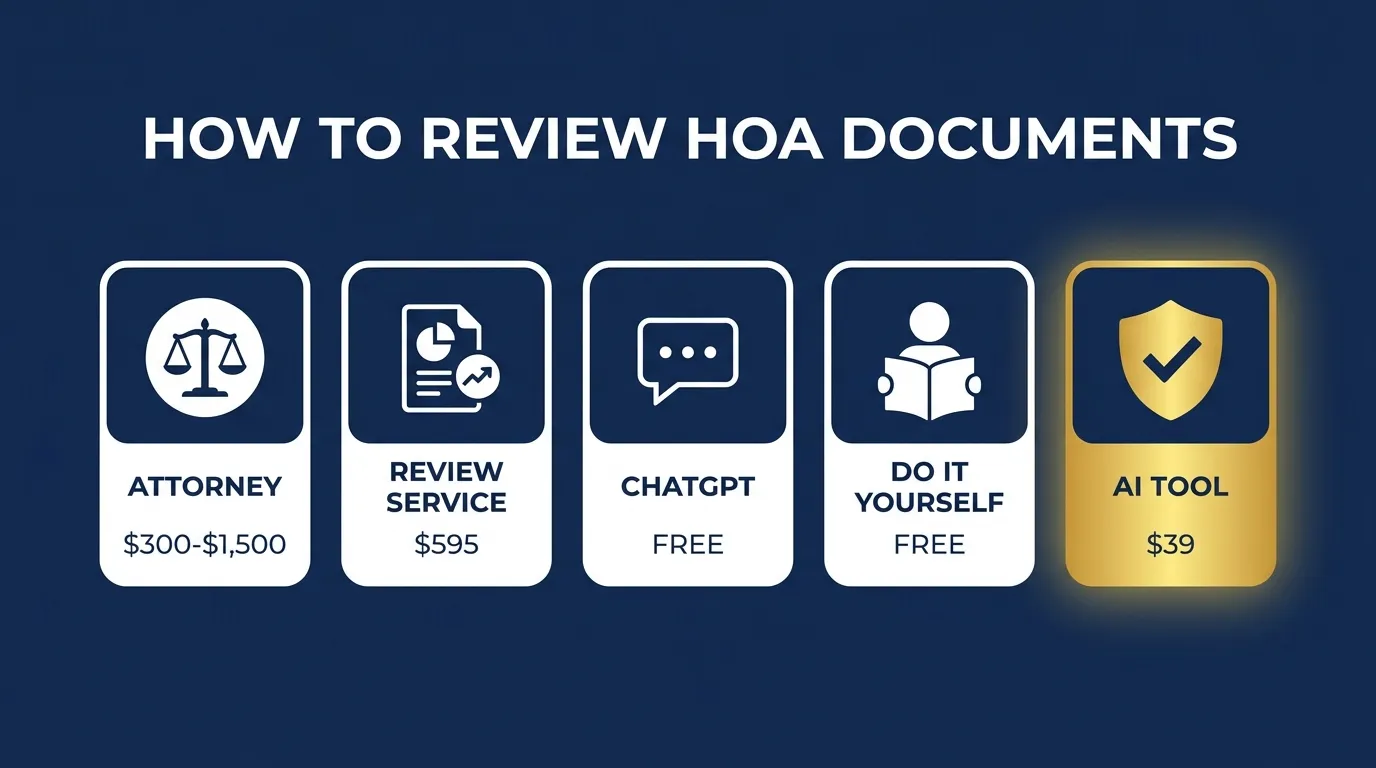

The Cheaper Alternatives, Compared

Options range from a $595 financial-review service to free ChatGPT to a $39 AI tool built for HOA documents. They differ sharply in cost, speed, and whether they cover legal and financial risk.

An attorney is not the only way to get a second set of eyes on the package. Here is how the realistic options compare:

| Option | Typical cost | Speed | Covers legal restrictions? | Covers financial risk? |

|---|---|---|---|---|

| Real estate attorney | $300–$1,500 | Days | Yes, the strength | Usually limited |

| Condo financial review service | ~$595 | ~5 days | No, financial focus | Yes, the strength |

| ChatGPT or a free chatbot | Free | Minutes | Partial, unreliable | Partial, unreliable |

| Read it yourself | Free (your time) | Hours | If you know what to look for | Hard for a layperson |

| Purpose-built AI tool | $39 one-time | Minutes | Yes | Yes |

A useful thing to notice: the attorney and the dedicated financial-review service attack different halves of the problem. A condo financial-review report benchmarks reserves, budgeting, and governance but does not parse your CC&R restrictions; an attorney parses the restrictions but rarely runs the reserve math. Buying both gets you past two thousand dollars. That gap, full coverage at a fraction of the price, is the wedge for tools built specifically to read HOA documents.

Is ChatGPT Good Enough?

Free chatbots are fast and cheap but unreliable on legal and financial documents, with measured hallucination rates high enough to make them risky for a six-figure decision.

It is tempting to paste the documents into a free chatbot and ask what to worry about. As a first pass it can surface obvious themes, but the reliability is the problem. A 2024 Stanford study found general-purpose models hallucinated on a majority of legal queries, and even purpose-built legal research tools produced incorrect or unsupported answers a sizable share of the time. Real lawyers have been sanctioned for filing briefs full of citations a chatbot invented.

The deeper issue is that a general chatbot does not know what a good condo looks like. It has no benchmark for a healthy percent-funded ratio, no awareness of the Fannie Mae warrantability rules, and no reliable way to tell you what is missing from the packet, which is often the most dangerous signal of all. For a quick orientation, free AI is fine. For a decision worth hundreds of thousands of dollars, an unverifiable answer is not something to lean on. We compare the options in more detail in our roundup of HOA document analysis tools.

When It Is Still Worth Paying an Attorney

Hire an attorney for genuine legal questions: ambiguous covenants, active litigation, unusual amendments, or any state where attorney representation at closing is required.

None of this means skipping the lawyer when you actually need one. There are clear situations where an attorney's judgment is worth every dollar:

- You live in a state where an attorney is required or customary at closing, so the marginal cost of adding a document review is small.

- The package shows active or threatened litigation, and you need to understand your exposure and how it affects financing.

- A covenant is ambiguous or unusual, and the difference between two readings affects how you can use the property.

- There are recent or pending amendments to the governing documents whose legal effect is unclear.

- Something in a screening pass flags a legal issue you want a professional to interpret before you remove a contingency.

The point is to spend the legal budget where legal expertise is the thing you are buying, rather than paying attorney rates to confirm that a reserve fund is thin, which a much cheaper tool can tell you in minutes.

A Smarter Workflow: Screen First, Escalate Second

Screen the whole package with an inexpensive tool first, then spend attorney dollars only on the specific legal questions the screen surfaces. You get full coverage and a smaller bill.

For most buyers, the efficient path is a two-step sequence. First, run the full document package through an inexpensive screening pass that reads everything and surfaces the financial and structural risks: percent funded, reserve adequacy, special-assessment signals in the minutes, rental restrictions, insurance gaps, and warrantability concerns. This is fast, cheap, and covers the financial ground an attorney typically does not.

Second, if the screen turns up a genuine legal question, an ambiguous restriction, a litigation reference, an amendment you do not understand, take that specific issue to an attorney. You are now paying for an hour of targeted legal judgment instead of several hours of someone reading routine documents from scratch. The total is often a fraction of a full review, and you have covered both the legal and the financial side rather than one or the other.

That is exactly what GoverningDocs is built to do: read the entire package, grade the property, and link every finding to the page it came from, so you and, if needed, your attorney know precisely where to look. You can start free with the CC&R analysis tool, reserve study analyzer, and meeting minutes tool, then run a full property report when you are under contract.

Frequently Asked Questions

Do I need a lawyer to review HOA documents before buying?

Not always. In states where an attorney handles the closing, adding a document review is inexpensive and sensible. Elsewhere, the legal review is optional, and the risks that most often cost buyers money are financial rather than legal. A practical approach is to screen the full package with an inexpensive tool first, then hire an attorney only for specific legal questions it surfaces.

How much does it cost to have an attorney review condo documents?

Roughly $300 to $1,500. Real estate attorneys bill about $150 to $500 per hour, averaging around $377, and a focused document review usually runs one to three hours. In states where an attorney handles the closing, the review may be folded into a flat fee of about $750 to $1,250 rather than billed separately.

Can I just use ChatGPT to review my HOA documents?

You can use it for a rough first pass, but do not rely on it for the decision. A 2024 Stanford study found general-purpose chatbots hallucinated on a majority of legal queries, and even legal-specific tools were wrong a meaningful share of the time. A general chatbot also has no benchmark for healthy reserves or Fannie Mae warrantability and cannot reliably tell you what is missing from the packet.

What does an HOA document review include?

A thorough review covers the CC&Rs, bylaws, articles, rules, current and proposed budgets, balance sheet and financial statements, the reserve study, several years of meeting minutes, special-assessment notices, the master insurance certificate, and the resale or estoppel certificate. The goal is to identify restrictions, financial weaknesses, pending litigation, and anything that affects financing.

How long does an attorney take to review HOA documents?

It varies by attorney and is rarely guaranteed, which can be a problem when state law gives the association only days to deliver the package and you have a short window before contingencies expire. Florida allows 10 business days to deliver an estoppel certificate and Virginia 14 days for a resale certificate, so build review time into your timeline and confirm turnaround before you engage anyone.

Is a $39 AI tool really comparable to an attorney?

They do different jobs. An attorney provides legal judgment on restrictions, litigation, and ambiguous language. A purpose-built AI tool reads the entire package quickly and flags financial and structural risk with citations to the source pages. The efficient approach uses the tool to screen everything inexpensively, then reserves attorney time for genuine legal questions, rather than treating one as a full substitute for the other.

Get Your HOA Documents Analyzed

GoverningDocs analyzes CC&Rs, reserve studies, and meeting minutes, identifying red flags, restrictions, and financial risks so you can buy with confidence. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

Sources & References

- iBuyer (real estate attorney hourly and flat-fee ranges, 2026)

- CID Analytics (CIDA condo financial-review report, $595, ~5-day turnaround)

- Stanford HAI / RegLab (legal AI hallucination benchmarking study, 2024)

- Association Reserves (percent-funded tiers: weak, fair, strong)

- Association Reserves 2026 Industry Insights Report (34% of communities in the 0–30% weak band; 74% under 70% funded)

- CNN (Champlain Towers South, ~6.9% funded, $80,190–$336,135 per-unit assessment)

- National Mortgage News (Fannie Mae condo ineligibility list, ~5,175 projects, 2025)

- Condo-Approval (Fannie LL-2026-03: reserve allocation 10% to 15% effective January 4, 2027; Limited Review retired August 3, 2026)

- Fla. Stat. §718.116 (estoppel certificate, 10 business days)

- Va. Code §55.1-2309 (resale certificate, 14-day delivery)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. Attorney fees, document-delivery deadlines, and reserve and disclosure requirements vary by state and by the specific transaction, and the figures cited are general ranges and reported examples, not quotes for your situation. Statutes referenced are current as of June 2026 and may be superseded. Consult a qualified real estate attorney for guidance specific to your situation.