In This Guide

A condo resale certificate is the statutory disclosure package the association produces when a unit changes hands. In a typical state it includes 15 documents covering governance, finances, reserves, insurance, and litigation, costs $250-$375 to produce, must be delivered within 10 business days (or, in Florida, before contract execution for the §718.503 package and within 10 business days for the separate §718.116(8) estoppel), and triggers a 3-7 day cancellation window depending on the state. The single most expensive omission buyers miss: the reserve-study summary is not the reserve study.

Most condo buyers sign their purchase contract before they have ever seen the resale certificate, then receive a 200-page PDF a week before closing and never open it. The package is treated as paperwork. It is not paperwork. It is the document that decides whether the building's reserves are funded, whether a $50,000 special assessment was scheduled in last month's board minutes, whether the master insurance policy has a $250,000 deductible that the unit owner is on the hook for, and whether the association is named in a pending construction-defect lawsuit that would render the building unfinanceable under Fannie Mae B4-2.1-03.

The cost of skipping it is measurable. Owners at the Isola Condominium on Brickell Key in Miami absorbed a $19 million special assessment in 2025 for pool-deck and garage repairs the prior years of board minutes had flagged as deferred maintenance. Buyers in Miami who closed before the January 1, 2026 Florida SIRS funding deadline are now absorbing per-unit assessments of $30,000 to $75,000, with worst cases over $100,000. In every documented case, the signal was visible in the resale package somewhere. The buyer either did not receive the package early enough to read it, or did not know what to look for once they did.

This guide is the buyer's map of what is actually inside a resale certificate, what state law requires the association to disclose (and what it lets the association leave out), how much you should expect to pay, how many days the statute gives you to cancel if you find something terrible inside, and how to read the document in the order that surfaces problems fastest.

What "Resale Certificate" Actually Means (It Differs by State)

"Resale certificate" is colloquial. Florida has two separate documents commonly merged in conversation. California, Colorado, and New York have no single statutorily-named resale certificate at all.

The phrase "condo resale certificate" covers very different documents depending on the state. Confusing them is the most common mistake buyers and even agents make.

- Florida has two documents. Fla. Stat. §718.503 is the condo purchase disclosure package the seller delivers (declaration, articles, bylaws, rules, current financials and budget, milestone inspection summary if applicable, SIRS, turnover inspection report, FAQ document, governance form). Fla. Stat. §718.116(8) is the estoppel certificate, a roughly dozen-data-point lien-clearance and assessment-status instrument. The estoppel is narrower (focused on what the owner owes today) and carries a statutory base fee of $250, CPI-adjusted by DBPR to a current schedule of $299 standard plus expedite and delinquency add-ons. The §718.503 package is what a buyer actually reads to make a decision.

- Virginia consolidated everything in 2023. The Virginia Resale Disclosure Act (Title 55.1, Chapter 23.1, effective July 1, 2023) replaced the separate condo (§55.1-1990, repealed) and POA frameworks with a single 30-item resale certificate covering both ( Va. Code §55.1-2310).

- California uses a contents list, not a named document. Cal. Civ. Code §4525 tells the association what it must deliver but does not name the bundle.

- Colorado relies on a contract disclosure. C.R.S. §38-35.7-102 requires a bold-faced statement in the purchase contract. Document delivery is governed by the Real Estate Commission contract form, not statute.

- New York has no resale-certificate statute. A buyer receives a board package determined by the individual condo's bylaws, plus a right-of-first-refusal waiver from the board, plus a managing-agent "condo questionnaire" that exists primarily to satisfy lender (Fannie/Freddie) underwriting.

- Massachusetts only has a 6(d) certificate. M.G.L. c.183A §6(d) is a narrow lien-clearance certificate, not a comprehensive disclosure package. Massachusetts buyers obtain governing documents and financials by contract negotiation, not statute.

The practical buyer takeaway: ask your agent, in writing, exactly which statutory document(s) the seller is delivering, when, and whether your state attaches a cancellation window to the delivery date. In Florida you should receive both §718.503 and the §718.116(8) estoppel. In Washington, Texas, Illinois, and Virginia you get one named resale certificate. In California, Colorado, and New York you assemble the picture from a bundle that has no statutory name.

The 15 Documents Inside a Typical Resale Certificate

A complete resale package covers 15 categories: governance, finance, reserves, insurance, litigation, violations, fees, and ROFR. Each has one or two red flags the buyer should check.

Across the states that publish a named contents list, the package consolidates into 15 standard document categories. The right-hand column is the buyer-actionable red flag for each.

| Document | Red flag to check |

|---|---|

| 1. Declaration / CC&Rs | Rental caps or short-term rental bans that conflict with the buyer's plan or lender's rules. |

| 2. Bylaws | Low quorum threshold (e.g., 10%) that lets a tiny board pass a large special assessment. |

| 3. Rules & regulations | Recent amendments tightening restrictions on rentals, pets, parking, or improvements. |

| 4. Current operating budget | No line item for insurance escalation; reserve contribution flat or declining year over year. |

| 5. Balance sheet / financial statements | Operating fund consistently negative; unrestricted cash below 2 months of expenses. |

| 6. Reserve study (or summary) | Percent funded below 30%. "Summary only" provided instead of the full component table. |

| 7. Recent meeting minutes | Executive session entries about "pending litigation" or "engineer's report" with no resolution in later months. |

| 8. Special assessment history + pending | An assessment voted within the prior 12 months but not yet billed, or one discussed in minutes but not yet voted. |

| 9. Current monthly assessment + building delinquency | Delinquency above 15% of units 60+ days past due triggers Fannie Mae non-warrantable status under LL-2026-03. |

| 10. Master insurance certificate (ACORD) | Deductible above $25,000 or above 5% of insured value. Owner's loss-assessment coverage gap is the exposure. |

| 11. Pending litigation list | Any safety, structural soundness, or habitability case is categorically ineligible under Fannie B4-2.1-03. The 10%-of-funded-reserves figure is a separate minor-litigation safe harbor for other case types. |

| 12. Violations on the subject unit | Open violations that survive closing and bind the new owner. Several states read the disclosure requirement narrowly (e.g., Maryland practitioners flag that informal warnings, as opposed to charged violations, often are not surfaced). |

| 13. Transfer / move-in fees and capital contribution | Capital contribution of 2-3 months of dues plus transfer fee often adds $1,500-$5,000 at closing depending on the association. |

| 14. Right of first refusal (ROFR) | Even unexercised ROFR causes lender objections and adds 10-30 days to closing. |

| 15. FHA / VA approval status | Project not on the FHA approved list means an FHA buyer cannot finance. Single-unit FHA approval has its own delinquency, owner-occupancy, and litigation tests. |

Three of these (reserve study, meeting minutes, financial statements) carry most of the predictive signal about future special assessments. The other twelve are screens that catch the disqualifying cases. The order in which to read them is in the final section of this guide.

What's Not in There (And What Buyers Think Is)

The most expensive omissions are: reserve-study summary instead of the full report, meeting minutes only as far back as the statutory floor, threatened (not filed) litigation, and the insurance claims history.

State statutes set a floor, not a ceiling. The association can legally provide the minimum and leave out everything else. The recurring omissions buyers should request explicitly:

- The full reserve study, not the executive summary. Washington (RCW 64.34.425) and Virginia statutes say "current reserve study, if any" or a "summary." The summary hides the component table where remaining-useful-life and replacement-cost figures live. A 2050 roof replacement that will trigger a $40K/unit assessment shows up in the component table, not the summary.

- Meeting minutes older than the statutory floor. Virginia requires the prior 6 months; California allows the prior 12 on request; Florida's Condo Rider treats a 12-month window as the disclosure floor; Arizona requires none. A 2024 engineer's report estimating $8M of garage repair can legally be omitted if it sits outside that window. Ask for 18-24 months.

- Threatened or pre-suit litigation. Most resale certificates require disclosure only of "filed" or "material" litigation. Demand letters, pre-suit notices, arbitration claims, and D&O insurance reservation-of-rights letters do not appear. Yet those are exactly the precursors to a B4-2.1-03 ineligibility event.

- Insurance claims history. The certificate of coverage is included. The loss-runs (often the actual reason premiums tripled) are not.

- Engineering or milestone inspection reports outside Florida. Florida SB 4-D made these mandatory for buildings 3 stories or higher. Most other states do not. In a coastal Texas, Colorado, or California building, the engineering report is the missing key signal.

- Aging-bucket delinquency detail. The total delinquency rate is reported. The 90+ day aging bucket (the metric lenders use under Fannie LL-2026-03) usually is not.

- Bank-loan covenants. If the association borrowed to fund capital repairs, the loan covenants (DSCR, required reserve balance, default triggers) usually are not disclosed.

- Rules adopted between meetings. Board-approved rules between recordings of the "rules and regulations" snapshot may not appear.

Write the request for these items explicitly into the purchase contract addendum. The association is generally not required to surface them but is usually willing to provide them when asked in writing.

State-by-State Contents, Delivery, and Cancellation Windows

Florida gives a 7-day rescission window. Washington and Virginia give 5 and 3 days. California, Texas, Illinois, Massachusetts, and New York have none tied to the document itself.

The cancellation window is the buyer's most useful piece of statutory leverage. It is the only thing in the resale process that the association cannot waive. The table below compares the nine highest-volume condo states.

| State | Statute | Delivery | Cancellation window |

|---|---|---|---|

| FL (§718.503 package) | Fla. Stat. §718.503 | Before contract execution | 7 days (excludes Sat/Sun/holidays) |

| FL (§718.116(8) estoppel) | Fla. Stat. §718.116(8) | 10 business days | n/a (separate document) |

| VA | Va. Code §55.1-2309; §55.1-2310; §55.1-2312 | 14 days per §55.1-2309 | 3 days post-receipt |

| CA | Cal. Civ. Code §4525 | "As soon as practicable" | None statutory |

| WA WUCIOA | RCW 64.90.640 | 10 days | 5 days from receipt (the certificate itself can be waived in writing if unavailable) |

| WA WUCA (older condos) | RCW 64.34.425 | 10 days | 5 days post-receipt |

| CO | C.R.S. §38-35.7-102 | Per Real Estate Commission contract | None statutory (damages remedy) |

| IL | 765 ILCS 605/22.1 | 10 business days | None statutory |

| TX (condos) | Tex. Prop. §82.157 | 10 days (affidavit-in-lieu if missed) | None statutory |

| MA | M.G.L. c.183A §6(d) | 10 business days | None statutory |

| NY | No statutory resale certificate | Per bylaws (~30 days from complete app) | None statutory |

2024-2025 statutory updates that matter. Florida HB 1021 (2024) and successor 2025-166/175 added §718.503(2)(e): contracts entered after December 31, 2024 must include conspicuous-type disclosure of milestone inspection, turnover inspection, and SIRS status. Virginia's July 1, 2024 amendments require the association to be registered with the Common Interest Community Board (and current on filings, and offering electronic delivery) before it can collect any fee. Illinois' 102nd General Assembly amendment indexed the $375 fee cap to annual CPI beginning 2024. Washington WUCIOA HB 1500-S is the change to watch in 2026.

How Much It Costs and How Long It Takes

Statutory fee caps run $250-$375 in the states that publish them. Florida and Texas both top out at $375 once expedite and update fees are included. Three states (CA, CO, MA, NY) have no statutory cap.

Fees are usually paid by the seller and built into closing costs, but they are contract-negotiable. Where a delivery deadline exists, the association forfeits the fee if it misses the deadline (Florida is explicit on this for the §718.116(8) estoppel certificate).

| State | Base fee | Expedite / rush | Notes |

|---|---|---|---|

| FL estoppel | $299 | +$119 (3-day expedite); +$179 (delinquent unit) | DBPR CPI-adjusted 2022, next adjustment 2027. Free if not delivered in 10 business days. |

| WA | $275 | $100 update within 6 months | RCW 64.90.640 and 64.34.425 both apply. |

| TX condos | No statutory cap | Market rate; rush varies | §82.157 sets contents and 10-day delivery; no fee cap. Practical market range $250-$400. |

| TX POAs | $375 original | $75 update (within 180 days) | Tex. Prop. §207.003. |

| IL | $375 (CPI-indexed annually since 2024) | +$100 (72-hour rush) | 765 ILCS 605/22.1. |

| VA | CIC Board CPI-set | ~$50-$100 rush typical | Association must be CIC-registered to collect. |

| CA | "Reasonable actual cost" | Negotiated | Civ. §4530. No cap. No extra fee for electronic delivery. |

| CO | Association "usual fee" | Per contract | No statutory cap. |

| MA | "Reasonable" | Per management | No cap. Mortgagees in foreclosure pay zero. |

For practical budgeting, expect $300-$500 in fee-cap states and $400-$800 in no-cap states once an expedite or update fee is added. Rush fees are common because association management companies typically operate on 10-day cycles even when the statute says 10 days; closing pressure usually requires a paid expedite.

Cases Where the Resale Certificate Failed Buyers

The Florida SIRS wave (2026), Isola Brickell Key ($19M assessment), and Champlain Towers (the $15M pre-collapse assessment) all share the same pattern: the signal was in the package, the buyer did not have time to read it.

Florida SIRS wave (January 2026 forward). January 1, 2026 was the deadline for Florida condos 3 stories or higher to have a funded Structural Integrity Reserve Study under Fla. Stat. §718.112(2)(g). Industry reporting cites a wave of per-unit assessments in the $30,000-$75,000 range, with worst cases exceeding $100,000. Buyers who closed in 2024-2025 inherited the assessment. In most documented cases, the building's 2024 milestone inspection or 2025 SIRS draft was visible in the resale package's 12-month meeting minutes window. The buyer did not have time to read the SIRS draft inside the rescission window.

Isola Condominium, Brickell Key, Miami (2025). A $19 million building-wide special assessment for pool deck and garage repairs. Owners who closed before the assessment was voted absorbed the bill. The deferred maintenance had been documented in board minutes outside the 12-month statutory disclosure window.

Champlain Towers South (pre-collapse, 2021). An April 9, 2021 board letter outlined a $15 million remedial-works program to address documented structural concerns, roughly 2.5 months before the June 24, 2021 partial collapse. Post-collapse litigation made the timing and adequacy of disclosure to incoming buyers a central question. The Surfside collapse drove the entire SB 4-D / SIRS framework that produced the 2026 wave above.

Texas 1st Court of Appeals docket 01-14-00556-CV (2015). A Texas appellate opinion in which buyers raised the theory that the resale certificate, properly delivered, would have disclosed assessments and pending litigation not otherwise communicated. The legal theory still surfaces in 2024-2025 Texas resale disputes ( Justia opinion).

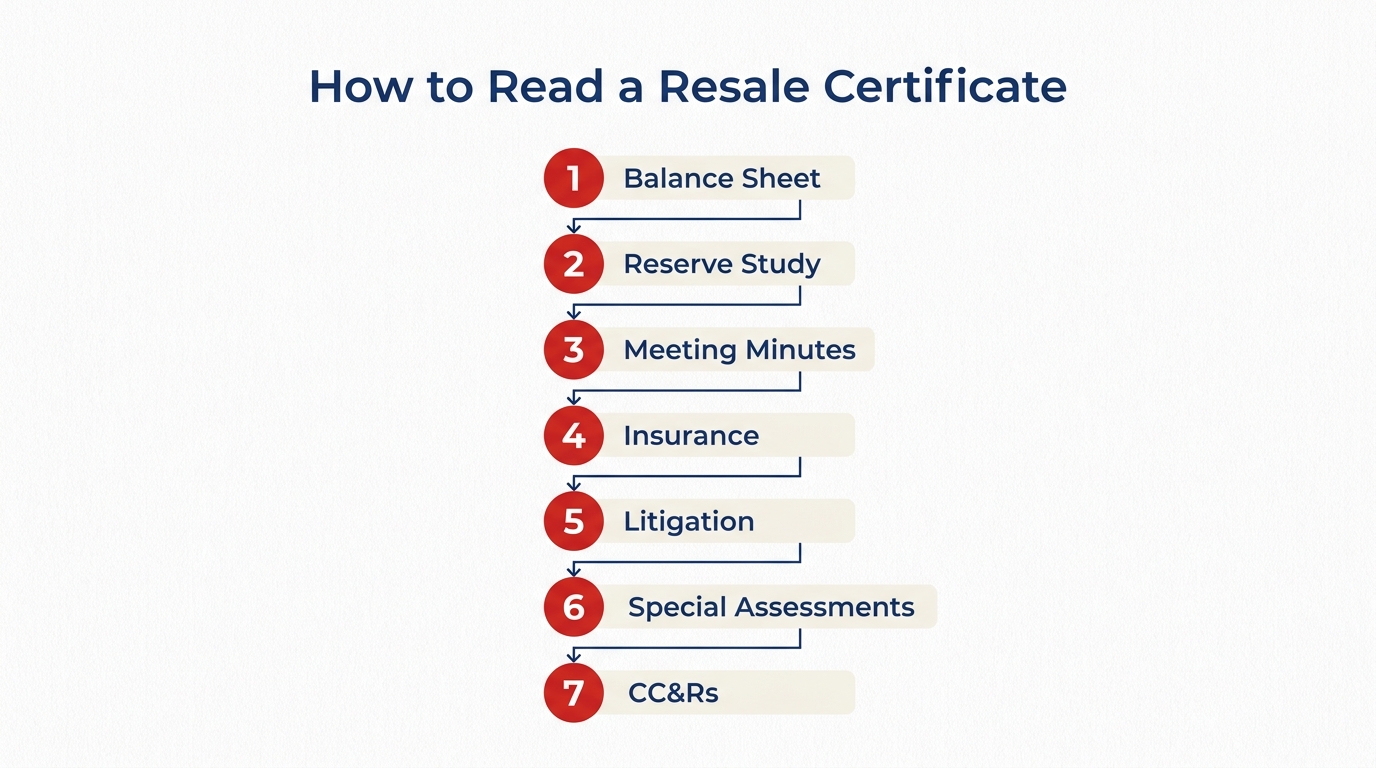

How to Read a Resale Certificate (In Order)

Read in this order: balance sheet first, then reserve study, then 12-24 months of meeting minutes, then insurance, then litigation, then governing documents last. Most disqualifying problems surface in the first three.

A 200-page package looks intimidating. In practice the disqualifying issues live in 4-6 documents. Read in this order and the package can be screened in 60-90 minutes.

- Balance sheet (current month) and prior year-end financial statement. Look for the cash position. Operating cash below 2 months of expenses is a yellow flag. Negative operating fund is red. Reserve cash should match the reserve study's "percent funded" figure.

- Reserve study (or summary, plus a request for the full report). Find the percent-funded number. Below 30% is the cutoff many state statutes flag and many lenders second-guess. Read the component table: any item with remaining-useful-life under 3 years and an unfunded balance is a near-term assessment.

- Meeting minutes, last 12-24 months. Search for "executive session," "litigation," "engineer," "assessment," "deferred," "insurance." Three or more executive-session entries about the same unnamed matter equals active litigation in practice. The meeting minutes analyzer flags these patterns across a multi-year archive in one pass.

- Master insurance certificate. Check the deductible. Above $25,000 or above 5% of insured value, you are buying into a loss-assessment exposure your HO-6 policy may not cover.

- Pending litigation disclosure. Cross-check against the Fannie B4-2.1-03 safe-harbor categories. A construction-defect, safety, or habitability suit can render the building unfinanceable regardless of damages size; other case types may still qualify for the minor-litigation safe harbor (one prong of which uses 10% of funded reserves). See how to surface HOA lawsuits before closing for the full discovery channels.

- Special assessment history and pending assessments. Anything voted in the prior 12 months but not yet billed is a closing cost. Anything discussed in minutes but not yet voted is a 30-90 day risk.

- Declaration / CC&Rs, bylaws, rules and regs. Read these last and focus only on rental restrictions, pet policies, ROFR, and quorum thresholds for assessments. The CC&R analyzer extracts these specific provisions in a single pass.

If anything in steps 1-5 is disqualifying, the rest of the package does not matter. Use the rescission window. In Florida that is 7 days, Washington 5, Virginia 3. In states with no statutory window, the leverage is in the financing contingency, the inspection contingency, and the appraisal contingency. Withdraw under one of those if the certificate surfaces a problem.

Frequently Asked Questions

Is a condo resale certificate the same as an estoppel certificate?

No. In Florida they are two separate statutory documents commonly conflated. Fla. Stat. §718.503 is the buyer's decision-making disclosure package (declaration, bylaws, financials, SIRS, milestone inspection summary). Fla. Stat. §718.116(8) is the estoppel certificate, a narrow lien-clearance and assessment-status instrument with a $250 statutory base fee (CPI-adjusted to $299 in the current DBPR schedule). Outside Florida, "resale certificate" usually means a single broader disclosure package; the term varies state by state.

Who pays for the resale certificate, buyer or seller?

By state custom the seller pays in most states (Florida, Washington, Maryland, Virginia, Illinois, California by management-company practice). In Texas it is often split. Every state allows the parties to negotiate this in the purchase contract, so it can be moved either way.

How long do I have to cancel after receiving the resale certificate?

Florida 7 days (excludes weekends and holidays). Washington 5 days from receipt for new WUCIOA communities. Virginia 3 days. California, Texas, Illinois, Massachusetts, Colorado, and New York have no statutory rescission window tied to the document itself; the remedy in those states is damages or a contingency-based contract withdrawal, not automatic rescission.

What's the most important document inside a resale certificate?

The reserve study, paired with the most recent balance sheet. Together they tell you whether the building can pay for its known future capital needs without a special assessment. Percent funded below 30% is the threshold many state statutes and most lenders treat as a warning. The component table inside the full reserve study shows which items will hit, and when, and for how much.

Why is the reserve-study summary not the same as the actual reserve study?

The executive summary typically shows percent funded and total recommended contribution. The full reserve study includes the component table: every common-element item, its remaining useful life, replacement cost, current balance, and contribution schedule. A 2050 roof replacement that will trigger a $40,000 per-unit special assessment shows up in the component table, not the summary. Always request the full report.

Can a seller refuse to give me the resale certificate?

Not in states where the statute requires it (FL, VA, WA, IL, TX, MA, CA contents list, CO contract disclosure). In Florida and Washington the contract becomes voidable if the package is not delivered. In Texas, if the association fails to furnish within 10 days, the owner may provide a sworn affidavit in lieu of the certificate. New York is the exception: the package is governed by individual condo bylaws, not statute.

What happens if the HOA misses the delivery deadline?

In Florida, the §718.116(8) estoppel certificate is free to the requestor if not delivered within 10 business days. In Washington, the contract is voidable until the certificate is delivered plus the 5-day rescission period. In other states, missed deadlines typically expose the association to damages claims rather than triggering automatic rescission, but you should escalate immediately and document the request in writing.

Are pending lawsuits required to be disclosed?

Filed and material litigation must be disclosed in nearly every state's resale certificate (FL, WA, VA, IL, TX, CA). Threatened or pre-suit matters (demand letters, arbitration claims, insurance reservation-of-rights letters) usually are not required. Yet those are exactly the precursors that lender questionnaires (Fannie Form 1076, HUD-9992) will surface during underwriting. If you can, request "all current and pending litigation, pre-litigation demands, mediation, and arbitration" in writing as part of the contract addendum.

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

- How to Get HOA Documents Before Making an Offer (State-by-State)

- Is Your HOA in a Lawsuit? How to Find Out Before You Buy

- Red Flags in HOA Meeting Minutes: What Buyers Should Spot

- Florida SIRS Report Explained: The 2026 Reserve Study Deadline

- HOA Financial Health: The 5-Number Check Before You Buy

- Fannie and Freddie Condo Rules 2026: The Warrantability Framework

Sources & References

- Fla. Stat. §718.503 (FL condo purchase disclosure package + 7-day rescission)

- Fla. Stat. §718.116 (FL estoppel certificate + 10-business-day delivery deadline)

- Berger Singerman: 2022 DBPR estoppel fee CPI adjustment ($299 / $119 / $179 in effect through 2027)

- Va. Code Title 55.1 Chapter 23.1 (Virginia Resale Disclosure Act, July 1, 2023 consolidation)

- Cal. Civ. Code §4525 (CID disclosure documents)

- RCW 64.34.425 (Washington WUCA resale certificate)

- RCW 64.90.640 (Washington WUCIOA resale certificate)

- 765 ILCS 605/22.1 (Illinois condo seller disclosures, $375 CPI-indexed)

- Tex. Prop. Code §82.157 (Texas condo resale certificate)

- Tex. Prop. Code §207.003 (Texas POA resale certificate)

- M.G.L. c.183A §6(d) (Massachusetts 6(d) certificate)

- C.R.S. §38-35.7-102 (Colorado CIC disclosure statement)

- Fannie Mae Selling Guide B4-2.1-03 (Ineligible Projects, eff. Aug 6, 2025)

- Biscayne Times: Isola Brickell Key $19M assessment (2025)

- LuxuryDade: Florida condo reserve law (Miami buyer impact, 2026)

- ULI Urban Land: After Surfside, Florida condo regulations

- Tex. 1st Court of Appeals docket 01-14-00556-CV (2015)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. State resale-disclosure statutes, fee caps, delivery deadlines, and rescission windows change frequently. Statute subsections referenced are current as of May 2026 and may be superseded. Consult a qualified real estate attorney in your state before acting on any specific resale-package issue.