In This Guide

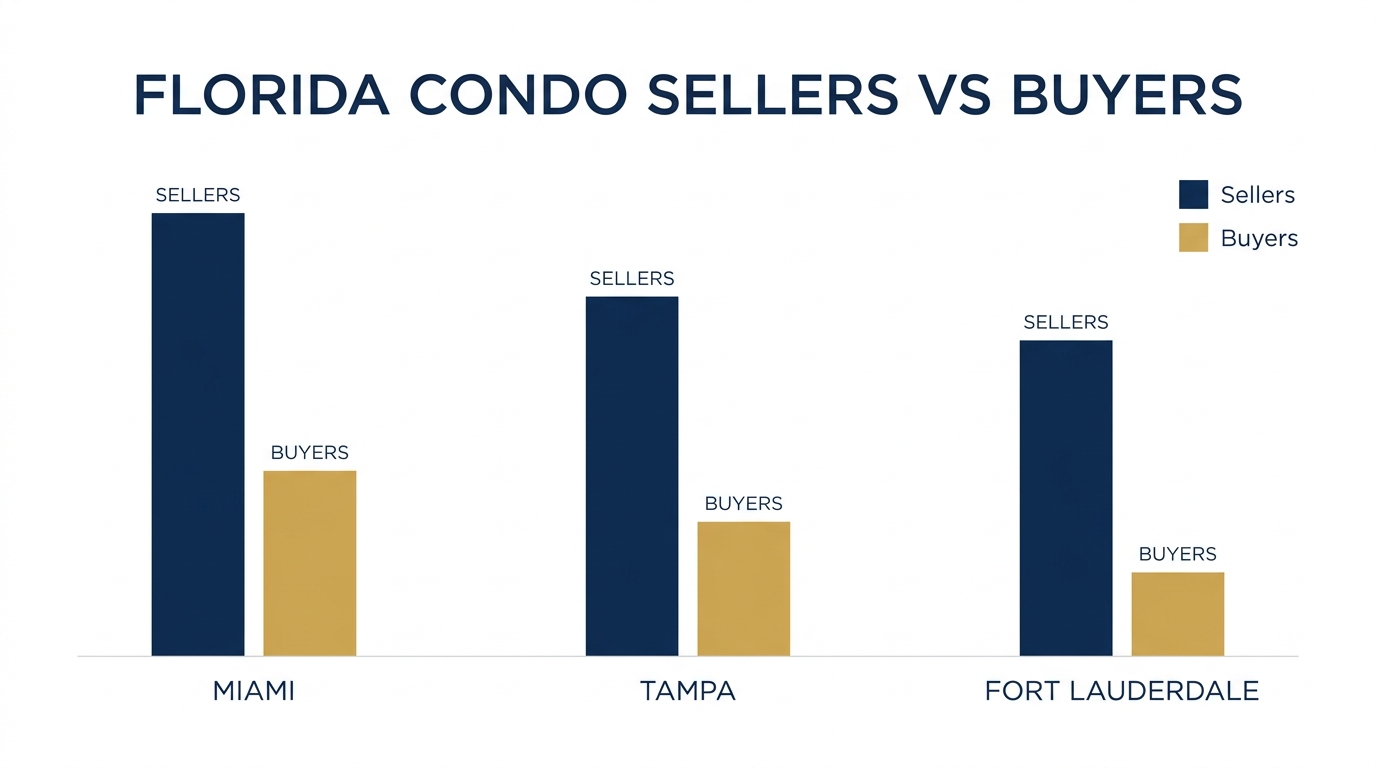

In Florida's biggest condo markets, sellers now outnumber buyers by roughly three to one. In Miami there were about 11,486 condo sellers against 3,270 buyers in August 2025, a 251% gap, and Tampa and Fort Lauderdale are close behind. That hands buyers real negotiating leverage. It also means many of those listings are being dumped because the building is facing a structural assessment, an insurance spike, or financing problems. The price is the easy part. Reading the building is the part that protects you.

A viral Redfin report put a number on what Florida agents have felt for two years: there are far more people trying to sell condos than buy them. The headline figure is national, but the imbalance is most extreme in Florida, where five of the ten worst seller-to-buyer ratios in the country sit. If you are a buyer, that sounds like good news, and in many ways it is.

The trap is assuming a soft market means every deal is a deal. A Florida condo can be 20% off its 2022 price and still be the worst purchase you ever make, because the discount is often the market pricing in a repair bill the seller already knows about. After the 2021 Surfside collapse, Florida forced aging buildings to inspect their structures and fund their reserves, and the resulting assessments can run into six figures per unit. The seller is not always fleeing a bad market. Sometimes they are fleeing a bad building.

This guide breaks down what the data really shows, why the glut is happening, how much leverage you actually have, and the exact documents that separate a genuine bargain from a money pit.

What the Redfin Data Actually Says

Nationally, sellers outnumber buyers by about 72%. In Miami the gap is 251%, Tampa 241%, and Fort Lauderdale 219%, all roughly three to one.

The widely shared statistic comes from Redfin's analysis of August 2025 data: across the U.S., there were about 72% more condo sellers than buyers, with the surplus topping 70% for months on end. For context, the seller surplus for single-family homes was only about 30%, and for townhouses 38%. Condos are a category apart, and Florida is the reason.

The "three to one" framing is a Florida-metro figure, not a national one. Here is how the worst markets actually break down:

| Metro | Sellers vs Buyers | Surplus |

|---|---|---|

| Miami | 11,486 vs 3,270 | 251% more sellers |

| Tampa | 5,183 vs 1,519 | 241% more sellers |

| Fort Lauderdale | 10,517 vs 3,300 | 219% more sellers |

| Jacksonville | 1,808 vs 578 | 213% more sellers |

| West Palm Beach | 6,847 vs 2,359 | 190% more sellers |

The pressure shows up in prices. Florida ended 2025 with a condo-townhouse median of $310,000, down 4.7% year over year, while single-family prices held nearly flat, according to Florida Realtors. Condo inventory hit 8.8 months of supply against just 4.6 months for single-family homes, a clear buyer's market by the standard four-to-six-month benchmark. Some metros fell much harder: Redfin recorded condo price drops of more than 30% in Deltona and 19% in Tampa in a single year. We dig into the broader slide in why condo prices are falling in 2026.

Why Florida Condo Sellers Are Flooding the Market

Post-Surfside inspection and reserve laws, an aging building stock, and soaring insurance have pushed owners to sell before the bills land.

This is not an ordinary downturn driven by interest rates. It is a regulatory and cost shock hitting an old building stock all at once. Roughly 60% of Florida's 1.5 million condos are 30 or more years old, and about two-thirds of units fall under the state's new inspection laws, per TD Economics. Three forces are converging:

- Mandatory structural inspections. After the Champlain Towers South collapse killed 98 people in 2021, Florida required milestone inspections for buildings three or more stories tall once they reach 30 years of age (25 near the coast). These inspections routinely uncover deterioration that triggers major repairs.

- Reserves that can no longer be waived. For decades owners voted to keep dues low by underfunding reserves. The Structural Integrity Reserve Study (SIRS) law ended that for structural components, with the first studies due December 31, 2025. Underfunding now converts directly into dues hikes or assessments.

- Insurance costs. Florida condo-unit insurance premiums rose more than 50% in four years, reaching about $2,000 statewide and $2,300 in Miami-Dade by the end of 2024, according to research from Florida International University's Metropolitan Center. Association master policies climbed even faster.

Stack rising dues, surprise assessments, and insurance spikes on top of each other, and many owners decided to sell before the bill arrived. That is the supply side of the imbalance. The demand side is buyers who have read the headlines and are wary of inheriting someone else's repair bill. For the full picture, see the 2026 Florida condo crisis.

What a Buyer's Market Means for Your Leverage

With months of supply well above normal, buyers can negotiate on price, ask for concessions, and take time on due diligence without losing the deal.

When inventory runs at nearly nine months and listings sit, the leverage shifts hard toward buyers. In May 2025, Redfin found condos in West Palm Beach were selling about 7% below asking after an average of 107 days on the market. Nationally, condos took 46 days to sell, the slowest May since 2015. A property that sits is a property whose seller is getting nervous.

Practically, that means you can:

- Negotiate below asking. Under-asking offers that would have been laughed off in 2021 are now normal, especially on units that have been listed for months.

- Ask for assessment credits. If the building has a pending or approved special assessment, you can ask the seller to pay it at closing or credit you the amount. Knowing it exists is what gives you the standing to ask.

- Take your time on due diligence. You are not competing with ten other offers. Use the breathing room to actually read the building's documents before you remove contingencies.

- Use Florida's resale cancellation window. For non-developer resales, 2025's HB 913 extended the buyer's rescission period to 7 days to review the declaration, financials, and governance documents.

Leverage on price is only half the win. The other half is using that same leverage to walk away from the wrong building entirely.

The Catch: A Cheap Condo Can Hide a Six-Figure Liability

A discounted unit can hide a special assessment far bigger than the savings. Some Florida buildings assessed owners $100,000+ per unit.

Here is the math that catches buyers. A unit listed $60,000 below its old peak looks like a bargain. But if the building just approved a $134,000-per-unit structural assessment, you did not save $60,000. You bought a $74,000 problem.

That figure is not hypothetical. At The Cricket Club, a roughly 220-unit building in North Miami built in 1975, owners were hit with an estimated $30 million building-wide special assessment, roughly $134,000 per unit, to fund roof replacement and facade waterproofing, as reported by the Wall Street Journal and Axios Miami. One owner who bought his unit for $190,000 in 2019 ended up selling for $110,000 in 2024, a 42% loss, rather than pay the assessment. That is exactly the kind of unit that shows up in the discount listings driving these seller-to-buyer numbers.

The reason this risk is rising, not falling, is the no-waiver rule. For budgets adopted on or after December 31, 2024, an owner-controlled association that needs a SIRS can no longer vote to underfund its structural reserves. A building that historically kept dues artificially low by skipping reserves now faces funding it cannot avoid, and that money has to come from somewhere: higher dues, a loan, or a special assessment. A clean-looking, low-dues budget on an older building is now a question to investigate, not a reassurance. We cover the mechanics in what owners can do about a SIRS assessment and special assessment red flags.

How to Tell a Discounted Condo From a Distressed One

Pull and read the SIRS, milestone inspection, reserve study, recent meeting minutes, budget, and estoppel certificate before you remove contingencies.

The documents tell you whether the discount reflects a soft market or a sick building. For any Florida condo three or more habitable stories tall, work through this list:

- SIRS report (Fla. Stat. §718.112(2)(g)). Required by December 31, 2025. Confirm it exists, check its completion date, and see which of the eight structural components are underfunded. A missing or overdue SIRS is a red flag by itself.

- Milestone inspection report (Fla. Stat. §553.899). Look for a Phase Two finding, which means an engineer identified substantial structural deterioration and major repairs are likely. See Florida milestone inspections in 2026.

- Reserve study and current balances. Compare reserves to what the study recommends. A wide gap signals coming dues increases or an assessment. Our free reserve study tool flags percent funded and special-assessment risk automatically.

- Meeting minutes, 12 to 24 months. This is where assessment votes, loan discussions, litigation, and insurance non-renewals show up before they hit the budget. See 7 meeting-minutes red flags.

- Current budget and any pending or approved special assessments. Read the line items, not just the bottom-line dues figure.

- Estoppel certificate (Fla. Stat. §718.116(8)). The association must issue it within 10 business days of a request, and it discloses every amount owed on the unit, including special assessments.

If reading a 60-page reserve study or a year of meeting minutes feels like too much, that is the gap our tools were built to close. For a buyer-side walkthrough of the whole process, see the complete condo buying checklist for 2026.

The Financing Trap: Fannie Mae's Ineligible List

A distressed building can fail Fannie Mae's standards, making conventional financing hard to get. New 2026 and 2027 rules tighten the screws further.

Even if you are comfortable with the building, your lender may not be. Fannie Mae maintains an internal list of condo projects it considers ineligible for the loans it backs, flagged for things like critical structural repairs, inadequate reserves, deferred maintenance, high delinquencies, or insufficient insurance. Attorneys tracking that confidential list have counted roughly 1,400-plus Florida buildings on it, with nearly half in Miami-Dade, Broward, and Palm Beach, per Mortgage Professional America. Fannie does not publish the list, so a building's status is something your lender or condo-approval specialist has to check.

The rules are also getting stricter. Fannie Mae's Lender Letter LL-2026-03 retires the streamlined "Limited Review" for projects over 10 units as of August 3, 2026, and raises the minimum reserve allocation from 10% to 15% of budgeted income for loan applications dated on or after January 4, 2027. A building with thin reserves that squeaked through before may not qualify next year. That affects your financing now and your future buyer's financing when you sell. We break it down in the 2026 Fannie and Freddie condo rules and what a non-warrantable condo means.

Frequently Asked Questions

Do Florida condo sellers really outnumber buyers 3 to 1?

In the biggest Florida metros, yes. In August 2025 Miami had about 11,486 condo sellers against 3,270 buyers, a 251% surplus, with Tampa at 241% and Fort Lauderdale at 219%, all close to three to one. Nationally the figure is lower, around 72% more sellers than buyers. The three-to-one ratio is a Florida-metro statistic, not a national one.

Is now a good time to buy a Florida condo?

The market favors buyers, with condo inventory at 8.8 months of supply and prices down about 4.7% year over year statewide at the end of 2025. That gives you room to negotiate. But a low price can mask a large special assessment or financing problem, so the bargain depends entirely on the building's documents, not just the listing price.

Why are so many Floridians selling their condos?

Mandatory post-Surfside milestone inspections and Structural Integrity Reserve Study (SIRS) requirements are forcing aging buildings to fund long-deferred structural repairs, often through six-figure special assessments. Insurance premiums have also risen more than 50% in four years. Many owners are selling to avoid the rising dues and assessments.

How big can a Florida condo special assessment be?

They vary widely, but can reach six figures per unit on older buildings needing major structural work. The Cricket Club in North Miami assessed owners roughly $134,000 each as part of an estimated $30 million repair. Buildings that deferred maintenance for years are the most exposed to large structural assessments once a milestone inspection or SIRS comes due.

What documents should I review before buying a Florida condo?

Request the SIRS report, the milestone inspection, the reserve study and current reserve balances, the last 12 to 24 months of meeting minutes, the current budget with any pending special assessments, and the estoppel certificate. Together these reveal whether a discounted unit is a genuine bargain or a building in financial distress.

Can I get a mortgage on a distressed Florida condo?

It can be difficult. Fannie Mae flags buildings with critical repairs, inadequate reserves, high delinquencies, or insufficient insurance as ineligible for its backed loans, and attorneys estimate more than 1,400 Florida buildings are on that internal list. New rules in 2026 and 2027 raise reserve requirements further, so check a building's financing status with your lender before you commit.

Get Your HOA Documents Analyzed

GoverningDocs analyzes CC&Rs, reserve studies, and meeting minutes, identifying red flags, restrictions, and financial risks so you can buy with confidence. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

Sources & References

- Redfin (condo sellers vs buyers, national 72% surplus and metro-level Miami/Tampa/Fort Lauderdale figures, Aug 2025 data)

- Florida Realtors (year-end 2025: condo-townhouse median $310,000, down 4.7%; 8.8 months of supply)

- Redfin (national condo days on market; West Palm Beach 7% below asking; FL metro price declines, May 2025)

- TD Economics (60% of Florida condos 30+ years old; ~two-thirds of units under inspection laws)

- WLRN / FIU Metropolitan Center (condo-unit insurance up 50%+ in four years to ~$2,000 statewide)

- Axios Miami (The Cricket Club: ~$30M assessment, ~$134,000 per unit, citing Wall Street Journal reporting)

- Fla. Stat. §718.112 (SIRS requirement, $25,000 threshold, no-waiver rule, estoppel under §718.116(8))

- Fla. Stat. §553.899 (milestone inspection: 30-year trigger, Phase One and Phase Two)

- Mortgage Professional America (~1,400+ Florida buildings on Fannie Mae's confidential ineligible list)

- Fannie Mae Lender Letter LL-2026-03 (Limited Review retired Aug 3, 2026; reserve minimum 10% to 15%, effective Jan 4, 2027)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. Market data reflects the periods cited and changes constantly, and Florida's condo statutes have been amended repeatedly since 2022. Statutes and rules referenced are current as of June 2026 and may be superseded. Consult a qualified real estate attorney and your lender for guidance specific to your situation and the specific building.