FHA and VA condo approval means the building meets government-backed lending requirements. FHA requires 50% owner-occupancy, 10% reserve funding, and under 15% delinquency. VA prohibits Right of First Refusal clauses and has no single-unit approval fallback. Both programs evaluate the building, not just the borrower.

If you're buying a condo with an FHA or VA loan, the lender doesn't just check your credit. They check the building. The condo project itself must meet specific financial and governance requirements, or the loan gets denied. This is true regardless of how qualified you are as a borrower.

The requirements differ between FHA and VA, and some of the differences are significant. Knowing what each agency looks for helps you avoid wasting time on buildings that can't be financed.

FHA Condo Approval Requirements

FHA evaluates project-level financials, owner-occupancy, insurance, and litigation. Projects can be approved through full project review (HRAP or DELRAP) or Single Unit Approval.

Owner-occupancy: 50% minimum. At least half the units must be owner-occupied primary residences. Can be reduced to 35% if the project is over 12 months old, has 3+ years of financial documents, under 10% delinquency, and allocates at least 20% of budget to reserves.

Reserve funding: at least 10% of annual budget. The HOA must allocate at least 10% of total budgeted income to reserves for capital repairs. Fannie Mae is raising its threshold to 15% in January 2027, but FHA's minimum remains at 10%.

Delinquency: no more than 15% of units 60+ days past due. Does not include late fees or administrative charges. Only counts units, not dollar amounts.

Single-entity concentration: 10% cap. No single investor or entity can own more than 10% of units in projects with 20+ units. For smaller projects, no entity can own more than 1 unit.

Commercial space: 35% max of total floor area. Updated from 25% in the 2019 HUD Final Rule. Exceptions up to 49% are possible on a case-by-case basis.

Insurance and litigation. Adequate master hazard (100% replacement cost), general liability ($1M minimum), and fidelity bond coverage required. No pending litigation that threatens financial solvency or structural soundness.

Single Unit Approval (SUA): Introduced in October 2019, SUA allows FHA loans on individual units in buildings that don't have full project approval. The building must still meet the core financial requirements, but the approval is per-unit rather than project-wide. SUA is not available for new construction or buildings with fewer than 5 units.

Check FHA approval status: Search the HUD Condo Lookup tool to see if a project is currently approved, expired, or not listed. FHA approvals last 3 years and must be recertified.

VA Condo Approval Requirements

VA requires full project approval with no single-unit fallback. Right of First Refusal and super-lien clauses are automatic dealbreakers that FHA does not specifically prohibit.

Owner-occupancy: 50% minimum. No flexibility. Unlike FHA, VA does not offer a reduced threshold for financially strong projects.

Right of First Refusal: prohibited. If the CC&Rs give the HOA the right to buy or lease a unit before outside buyers, VA will deny approval. This is the most common VA-specific dealbreaker. It must be removed or waived for VA borrowers.

Super-lien provisions: prohibited. The CC&Rs cannot give the HOA lien priority over the VA mortgage. VA views this as a risk to loan recovery in default.

Commercial space: 25% max. Stricter than FHA's 35% limit.

No single-unit approval. The entire project must be VA-approved before any unit can be purchased with a VA loan. There is no spot approval or per-unit workaround.

Insurance and leasing. Adequate hazard, liability, and fidelity bond coverage required. Complete rental bans and seasoning clauses are not allowed. VA protects military members' ability to lease during PCS (Permanent Change of Station).

Check VA approval status: Search the VA Condo Report tool to check if a project is approved. VA approvals are lifetime and do not expire, though they can be revoked if governing documents change or major compliance issues arise.

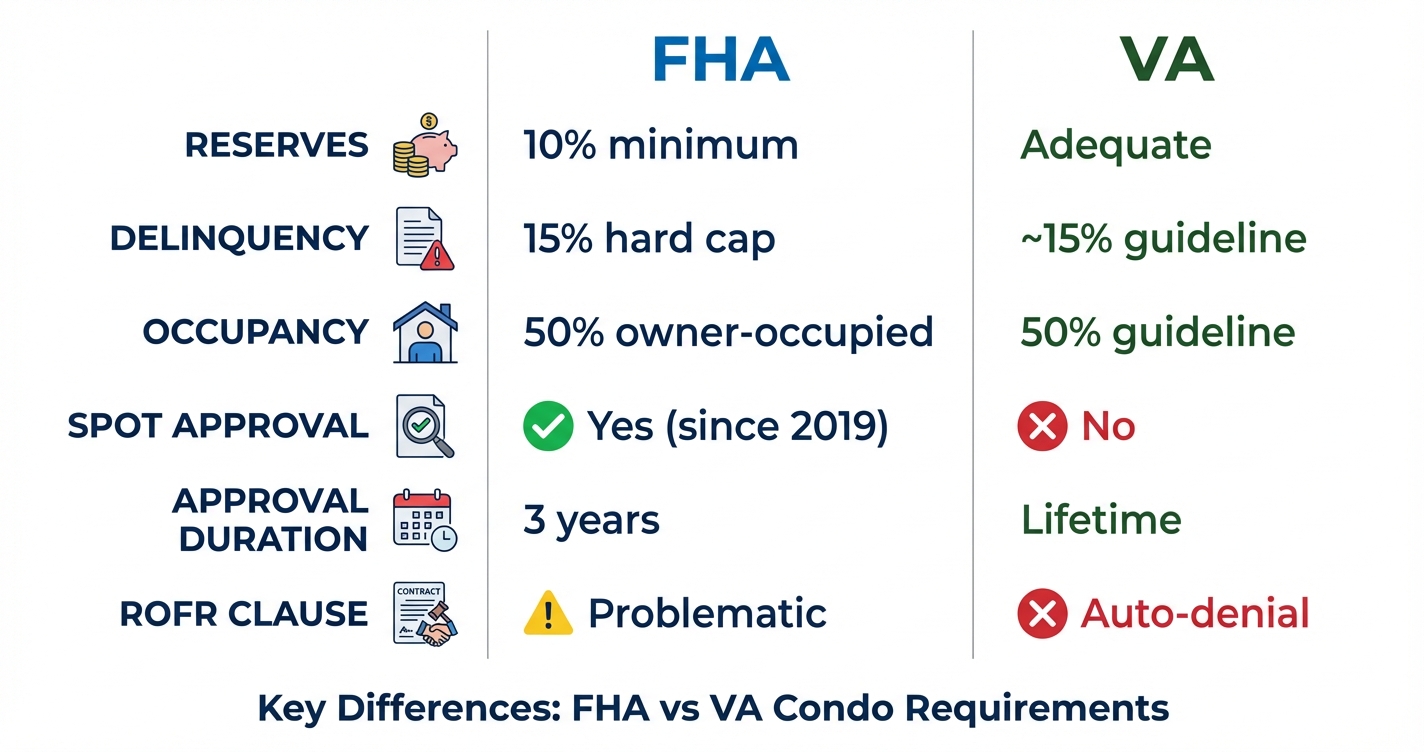

FHA vs. VA: Key Differences

VA is stricter on CC&R language (ROFR, super-liens) and has no spot approval. FHA is more prescriptive on financial thresholds and requires recertification every 3 years.

| Requirement | FHA | VA |

|---|---|---|

| Owner-occupancy | 50% (reducible to 35%) | 50% (no reduction) |

| Commercial space | 35% max | 25% max |

| Delinquency cap | 15% hard cutoff | Flagged during review (no published hard cutoff) |

| Reserve funding | 10% of budget minimum | Adequate reserves (no specific %) |

| Right of First Refusal | Not specifically prohibited | Automatic dealbreaker |

| Super-lien provisions | Not specifically prohibited | Automatic dealbreaker |

| Single-unit approval | Yes (SUA, since Oct 2019) | No |

| Approval duration | 3 years (must recertify) | Lifetime |

How to Check Before You Buy

Check the FHA or VA lookup tools first. If the building is not listed, review the CC&Rs and reserve study for red flags before your lender submits for approval.

Step 1: Check the lookup tools. Search the HUD Condo Lookup for FHA or the VA Condo Report for VA. If the building is listed and approved, you're in good shape.

Step 2: Review the CC&Rs. For VA buyers specifically, search for Right of First Refusal and super-lien language. These are the most common VA-specific dealbreakers and they're buried in the governing documents, not visible from the listing.

Step 3: Check the financials. Pull the reserve study for funding levels and the HOA questionnaire for delinquency rates. Both FHA and VA (through Fannie Mae/Freddie Mac) will flag buildings with under 10% reserve funding or over 15% delinquency.

Upload your CC&Rs to GoverningDocs' free CC&R analyzer to extract ROFR clauses, assessment language, and rental restrictions automatically. Upload your reserve study to the free reserve study analyzer to check percent funded, budget allocation, and components at end of useful life.

Frequently Asked Questions

What is FHA condo approval?

FHA condo approval means a building meets HUD requirements for FHA-insured mortgages. The project must have at least 50% owner-occupancy, 10% reserve funding, under 15% delinquency, adequate insurance, and no disqualifying litigation. Approval lasts 3 years and must be recertified. Buildings can also qualify through Single Unit Approval (SUA) on a per-unit basis.

What is VA condo approval?

VA condo approval means the entire project has been reviewed and approved by the VA for VA-backed home loans. The building must meet owner-occupancy, insurance, and governance requirements. Right of First Refusal clauses and super-lien provisions in the CC&Rs are automatic disqualifiers. VA approval is lifetime and does not expire.

Can I get a VA loan on a condo that isn't VA-approved?

No. The VA does not offer single-unit or spot approval. The entire condo project must be on the VA approved list before any unit can be purchased with a VA loan. If the building is not approved, a lender or the HOA can submit for approval, which typically takes 30 to 60 days.

What is the difference between FHA and VA condo approval?

FHA offers Single Unit Approval (per-unit) while VA requires full project approval. VA prohibits Right of First Refusal and super-lien clauses, which FHA does not specifically block. FHA has stricter financial thresholds (10% reserves, 15% delinquency) while VA is less prescriptive on exact percentages but stricter on CC&R language. FHA approval expires after 3 years. VA approval is lifetime.

Check Your Building's Eligibility

Upload your HOA documents for free analysis. Automatically flags ROFR clauses, reserve funding, delinquency, and other approval red flags. No signup required.

Want the full breakdown? Read our detailed guide to FHA and VA red flags →

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. FHA and VA approval requirements are subject to change. Consult a qualified lender or real estate professional for guidance specific to your situation.