In This Guide

An HO-6 policy's loss assessment coverage (Coverage E) has two gaps most condo owners never see until they get a six-figure assessment. First, carrier-filed "special limit" endorsements quietly re-cap the master-policy deductible passthrough at $1,000 to $2,000, regardless of the total endorsement purchased. Second, assessments tied to planned reserves, milestone inspections, SIRS funding, or deferred maintenance generally don't trigger Coverage E at all, because there's no covered peril.

Marisa O'Malley, a homeowner in the Gold Hill Mesa community of Colorado Springs, did everything an insurance broker would tell her to do. She bought $50,000 of loss assessment coverage on her HO-6 policy. When her HOA levied a $17,000-plus per-unit special assessment after a 2025 hailstorm, she filed a claim. Her carrier offered $1,000.

KRDO13 broke the story on March 19, 2026. "They responded and said, 'We can give you a thousand dollars,'" O'Malley told the station. "It's just a way for them to be off the hook." The Colorado Division of Insurance confirmed it had received more than 200 loss-assessment complaints since 2019 and signaled it was "trying to prohibit these endorsements."

Most condo owners assume HO-6 protects them. It usually doesn't, and there are two distinct reasons why. One is the "special limit" loophole O'Malley ran into. The other is bigger, and quieter: HO-6 loss assessment only pays when the underlying assessment is tied to a covered peril, which excludes the entire wave of milestone-inspection and SIRS-driven assessments hitting Florida condos right now. This guide explains both gaps, walks through what real six-figure assessments look like, and gives buyers and owners a concrete checklist before the next certified-mail notice lands.

For the master-policy side of the same crisis, see our piece on the master-policy side of the condo insurance crisis. This post is the unit-owner-policy side.

What an HO-6 Policy Actually Covers

HO-6 is the ISO unit-owner policy covering walls-in improvements, personal property, liability, and loss assessment, separate from the master policy.

HO-6 is the ISO-standard homeowners form designed specifically for condominium and cooperative unit owners. It assumes the building itself is covered by the association's master policy and fills in everything the master policy leaves out. The six coverage parts:

- Coverage A, Dwelling. Improvements, betterments, and "walls-in" build-out the unit owner is responsible for under the declaration.

- Coverage B, Other structures. Limited; typically only relevant for detached storage owned by the unit.

- Coverage C, Personal property. Contents of the unit.

- Coverage D, Loss of use. Additional living expense if the unit is uninhabitable.

- Coverage E, Loss Assessment. Pays the unit owner's share of an association assessment, subject to the gaps explained below.

- Coverage F, Liability and medical payments. Personal liability for events on the unit owner's premises.

The HO-6 is the companion to the association's master policy, not a replacement. The two policies are designed to dovetail, which is why master-policy decisions (deductible amount, walls-in vs. bare-walls coverage form) directly affect what the HO-6 has to fill.

| Policy | Insures | Held by |

|---|---|---|

| HO-3 (single-family) | Entire dwelling + contents + liability | Single-family homeowner |

| HO-6 (unit owner) | Walls-in + contents + liability + loss assessment | Condo or co-op unit owner |

| Master policy | Common elements, building shell, association liability | Association (allocated to owners via dues) |

Average HO-6 premiums run around $490 per year nationally. In Florida, premiums range from $500 to over $2,000 per year, with Citizens approving a 14.2% condo rate increase for 2025 and statewide HO-6 rates up roughly 28.8% since the 2022 reforms.

Coverage E: Loss Assessment Mechanics

Coverage E pays the unit owner's share of an assessment from a covered peril or master deductible. ISO default $1K-$2K; HO 04 35 raises it.

Loss assessment coverage was added to the HO-6 form to handle two specific scenarios:

- The unit owner's share of a covered-peril loss to common elements when the master policy's limit is exhausted. Example: a covered fire damages the lobby, the master policy pays out to its cap, and the association assesses owners for the shortfall.

- The unit owner's share of the master policy deductible when the association passes it through to owners after a covered loss. This is the most common real-world trigger.

ISO's standard HO-6 form provides $1,000 of loss assessment coverage by default in older editions, or $2,000 in newer ISO editions. To raise the limit, the unit owner buys the HO 04 35 Unit-Owners Coverage E Special Coverage endorsement, typically in tiers of $25,000 or $50,000, with specialty markets offering up to $100,000.

On paper, that's the protection. In practice, two structural features of how Coverage E is written and underwritten mean the headline limit on your declarations page is often not what the carrier actually owes when an assessment lands.

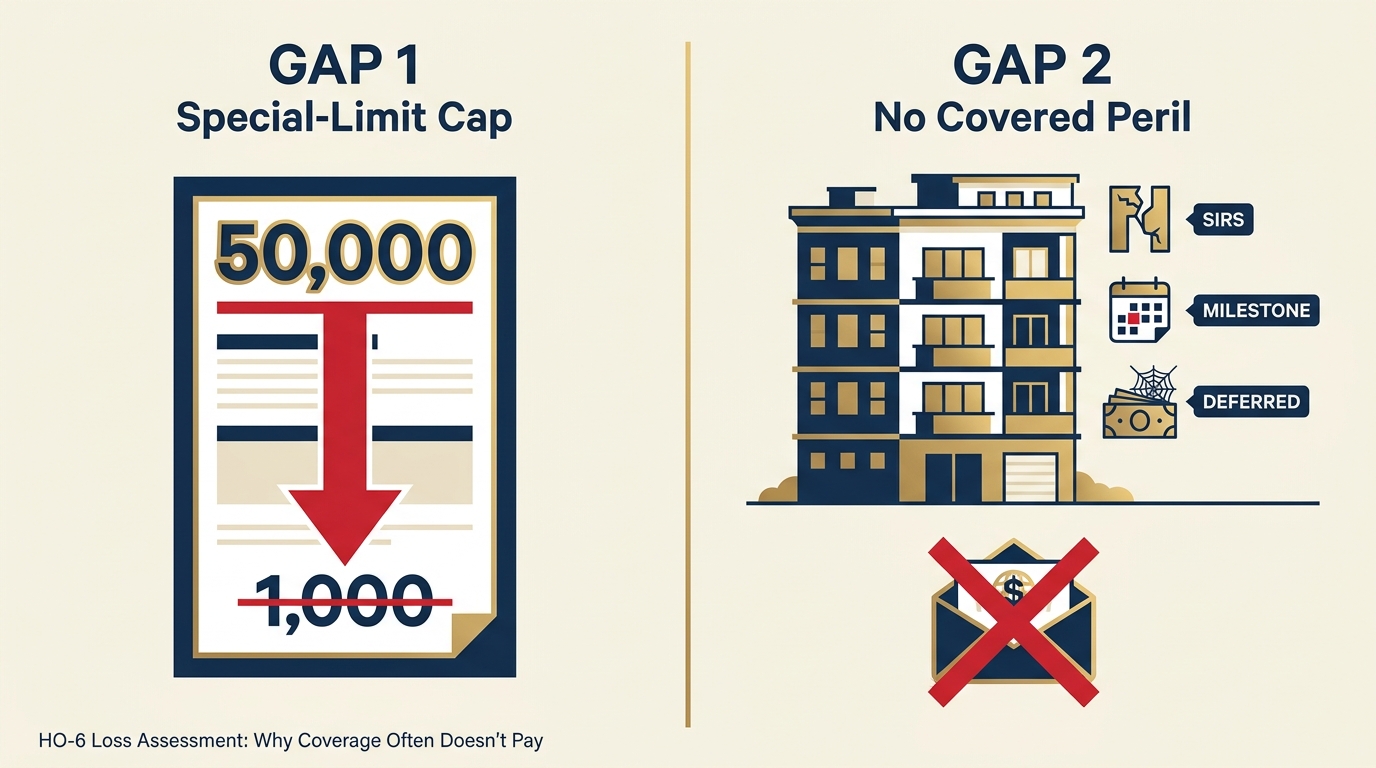

Gap #1: The "Special Limit" Loophole

Carrier "special limit" endorsements cap master-deductible passthrough at $1K to $2K regardless of the headline endorsement limit. The KRDO loophole.

The 05/11 edition of the ISO HO 04 35 form removed the ISO-level sublimit on the deductible-passthrough component. But carriers responded by re-introducing the cap through their own proprietary endorsements, often buried in the policy as a "special limit" clause. The effect is the same: the policyholder buys $50,000 of loss assessment coverage, and the carrier's endorsement quietly says that when the assessment is the master-policy deductible passthrough specifically, the payout is capped at $1,000 or $2,000.

That's exactly what happened in the KRDO investigation. Marisa O'Malley's Gold Hill Mesa HOA passed a $17,000-plus per-unit assessment to cover the master policy's deductible after a 2025 hailstorm. She had $50,000 of loss assessment coverage. Her carrier, identified by KRDO as Progressive, offered $1,000.

Robert Schifferdecker, the attorney featured in the KRDO segment, framed the pattern bluntly: "They're auto-renewing policies, but instead of raising your premiums, they're lowering what they're actually going to cover." The Colorado Division of Insurance confirmed it had received more than 200 loss-assessment complaints since 2019 and told KRDO it was "trying to prohibit these endorsements." Rep. Jeff Crank, R-CO, added: "It's sad you almost need a lawyer to read your policy before you sign up."

How to check if your policy has this carve-out: read the endorsement form itself, not the declarations page. Look for language that limits the master-policy-deductible-assessment portion separately from the total Coverage E limit. The phrase "special limit," a separate sublimit number, or a reference to "deductible assessment" capped lower than the main limit are the tells. If you can't find the form, request it in writing from your agent; carriers are typically required to provide endorsement forms on request.

Gap #2: The "No Covered Peril" Exclusion

HO-6 loss assessment only pays when tied to a covered peril. SIRS, milestone, and deferred-maintenance assessments generally pay $0.

This is the bigger gap, and the one buyers in milestone-inspection states most often miss. Coverage E pays only when the assessment is for a loss that would have been covered if the unit owner had owned the entire building. That ties Coverage E to the Section I/II perils on the underlying form: fire, wind, hail, theft, certain water events, and liability claims.

The HO 04 35 endorsement explicitly excludes several categories that account for the six-figure Florida assessment wave:

- Earthquake assessments (requires the separate HO 04 36 endorsement).

- Assessments levied by a governmental body, including code-enforcement actions.

- Assessments unrelated to a covered occurrence: planned capital improvements, scheduled reserve catch-up, routine deferred maintenance.

- Structural defect and construction-defect assessments, because there's no fortuitous peril event.

- SIRS-driven assessments in Florida, which are by definition planned reserves to meet a statutory funding schedule under Fla. Stat. §718.112(2)(g), not a sudden covered loss.

Apply this to the real cases. Palm Bay Yacht Club's $48.6 million assessment was for structural-repair work driven by the building's milestone inspection findings. Cricket Club's $30 million was for deferred capital work and SIRS catch-up. Mediterranean Village's assessment was for milestone-inspection-driven repairs and a substantial consultant line item. Under a strict reading of the HO 04 35 form, none of those would trigger Coverage E payouts, because there's no covered peril behind the levy. The owner with $50,000 of endorsement gets the same payout as the owner with the ISO default $2,000: zero.

That's the structural problem. The headline limit on your declarations page is a ceiling that rarely binds; what binds is the "caused by a covered peril" gate at the front of the coverage. For more on the underlying inspection and reserve regime driving these assessments, see the milestone inspections driving these assessments and Florida's SIRS funding requirements.

Real Six-Figure Florida Assessments

Three Florida 2024-2025 cases show what HO-6 won't cover: Palm Bay Yacht Club ($175K/unit), Cricket Club ($134K), Mediterranean Village (up to $400K).

| Building | Per-unit assessment | Total | Trigger |

|---|---|---|---|

| Palm Bay Yacht Club (Miami) | ~$175,000 upfront, OR up to $5,000/month for 20 years | $48.6 million | Milestone-driven structural repairs; $6.3M jury verdict Dec 10, 2025 against management and contractor |

| Cricket Club (North Miami) | ~$134,000 per owner | ~$30 million | Deferred capital work + SIRS catch-up |

| Mediterranean Village (Aventura, Williams Island) | Reportedly up to $400,000 per unit | Not publicly disclosed | Milestone-inspection repairs + $700K consultant line item |

The Cricket Club case has a human anchor that puts the HO-6 gap in concrete terms. Ivan Rodriguez bought a unit at the Cricket Club in 2019 for $119,000. Faced with the ~$134,000 assessment, he sold for $110,000, against an original listing of $350,000. The lender, the title company, and the buyer's agent all looked at his HO-6 declarations page. None of them caught that his loss assessment endorsement wouldn't pay a dollar against this kind of assessment.

The Palm Bay verdict matters here too. On December 10, 2025, a Miami-Dade jury awarded $6.3 million to Palm Bay Yacht Club owners on claims of fiduciary breach, negligence, and fraudulent misrepresentation against the management firm SFCM and contractor D&R. The verdict apportioned 60% fault to SFCM, 20% to D&R, and 20% comparative fault to the Association. The takeaway for owners is that even when the underlying assessment isn't reachable through HO-6, there can be a litigation path against the management chain. See your legal options once an assessment is levied.

State by State: Where the Floor Is

Florida sets a $2,000 minimum and $250 deductible cap under Fla. Stat. §627.714. California, Colorado, and Washington have no statutory minimum.

| State | Statutory minimum | Statute |

|---|---|---|

| Florida | $2,000 minimum loss assessment + $250 deductible cap on every HO-6 issued or renewed after July 1, 2010. HO-6 acts as excess over any other coverage. | Fla. Stat. §627.714 |

| California | No statutory loss-assessment minimum. Master coverage required for the association at Cal. Civ. §5800 (Davis-Stirling Act); unit-owner endorsement is optional. Cal. Ins. Code §10103 separately governs residential property insurance declarations-page disclosures. | Cal. Civ. §5800; Cal. Ins. Code §10103 |

| Colorado | No statutory minimum. DOI publicly signaled it is "trying to prohibit these endorsements" (KRDO, Mar 19, 2026); 200+ complaints since 2019. | DOI consumer protection authority |

| Washington | No specific HO-6 loss-assessment minimum identified. WUCIOA governs association reserves, not unit-owner HO-6 policies. | WUCIOA (reserves only) |

The Florida floor is the highest in the country, and it's still only $2,000. That number was set in 2010, before the milestone-inspection regime, before SIRS, and before the current wave of six-figure assessments. Even with maximum statutory protection, a Florida unit owner without an HO 04 35 endorsement is $2,000 deep on a $175,000 assessment.

Buyer's Checklist Before Closing

Pull five docs before closing: master policy declarations, master deductible, current reserve study, 3 years of minutes, HO-6 endorsement form.

- The HOA master policy declarations page. Confirm the building is insured, the limits are adequate to rebuild, and the named insured matches the association. The declarations page is the document the loss-assessment endorsement is designed to dovetail with; you can't evaluate your HO-6 in isolation.

- The master-policy deductible amount. A $100,000 master deductible across 50 units is a $2,000 passthrough per unit on any major loss. A $500,000 deductible is $10,000 per unit. The higher the master deductible, the more loss-assessment coverage you need, and the more important Gap #1 becomes.

- The current SIRS (Florida) or reserve study. The reserve schedule tells you which structural components are funded and which are not. Unfunded items become candidates for what a special assessment is, and those assessments are precisely the type Coverage E will NOT cover. For Florida specifically, see Florida SIRS reports.

- Three years of board meeting minutes. Look for discussions of milestone inspections, structural assessments under review, contractor bids, reserve catch-up plans. These are the leading indicators of an imminent assessment. See document patterns that predict a special assessment.

- Your own HO-6 endorsement form (HO 04 35) and any "special limit" clauses. Don't rely on the declarations page. Request the endorsement form from your agent and read for sublimits on the master-deductible-passthrough portion.

What Current Owners Should Do

Four moves: raise endorsement to $25K-$50K, get the carrier's form, ask the HOA broker about passthrough language, document scheduled assessments.

- Raise your loss-assessment endorsement. Standard tiers are $25,000 and $50,000. Specialty markets go up to $100,000. The marginal premium cost is typically modest, often roughly $25-$75 per year per $25,000 of additional limit, depending on carrier and state.

- Request the carrier's endorsement form in writing. Ask specifically: "Does the policy contain a 'special limit' or sublimit on the portion of Coverage E attributable to a master-policy deductible passthrough?" Get the answer in writing on carrier letterhead, not from an agent's recollection.

- Ask the HOA insurance broker about the master-policy deductible. Know the deductible figure, know how the board allocates a passthrough (per-unit, by share-of-ownership, by floor), and know whether the master policy is on a guaranteed-replacement-cost basis. The HOA's broker is required to provide a declarations page on request.

- Document any scheduled SIRS or milestone-driven assessments. If the board has acknowledged an upcoming assessment in minutes or correspondence, your Coverage E is unlikely to help, but other levers (refinance, payment plans, statutory rights) may. See your legal options once an assessment is levied.

For the broader frame on how insurance, reserves, and assessments interact in a building's financial profile, our pillar guide on the full HOA financial health framework walks through the diagnostic numbers buyers and owners should track before, during, and after closing.

Frequently Asked Questions

What is HO-6 loss assessment coverage?

Loss assessment is Coverage E on a standard ISO HO-6 condo unit-owner policy. It pays the unit owner's share of an association assessment when that assessment is caused by a peril covered under the policy (fire, wind, hail, liability) or by a master-policy deductible passthrough following a covered loss. The ISO default limit is $1,000 in older form editions or $2,000 in newer editions. The HO 04 35 endorsement raises the limit, typically to $25,000 or $50,000.

How much loss assessment coverage do I need?

It depends on the master-policy deductible divided by the number of units, and on your building's structural-reserve picture. As a rough guide, the endorsement should be at least 1x the master-policy-deductible passthrough per unit, and ideally 2-3x. In Florida, where the statutory minimum is only $2,000 under §627.714, most buyers and brokers recommend $25,000 to $50,000. Note that even maximum coverage does NOT protect against assessments not tied to a covered peril, like SIRS funding or milestone-inspection repairs.

Does HO-6 cover a special assessment for milestone inspection repairs?

Generally no. HO-6 Coverage E pays only when the underlying assessment is caused by a peril covered under Section I or II of the policy (fire, wind, hail, liability). Milestone-inspection-driven structural repairs, SIRS-funded reserves, deferred maintenance, and capital improvements do not involve a covered peril, so the endorsement does not trigger regardless of limit. The HO 04 35 form explicitly excludes assessments unrelated to a covered occurrence and structural-defect assessments.

Why did my carrier only pay $1,000 on a $50,000 endorsement?

The most likely reason is a carrier-filed "special limit" endorsement that re-caps the master-policy-deductible-passthrough portion of Coverage E at $1,000 or $2,000, separate from the headline limit. The ISO 05/11 edition of HO 04 35 removed the ISO-level sublimit, but many carriers reintroduced it through their own proprietary endorsement forms. Read the actual endorsement (not the declarations page) for a separate sublimit on deductible-assessment claims. The KRDO13 March 19, 2026 investigation documented this pattern at Progressive in Colorado.

Does Florida require minimum loss assessment coverage?

Yes. Fla. Stat. §627.714 requires every HO-6 unit-owner policy issued or renewed after July 1, 2010 to include at least $2,000 of loss assessment coverage with a deductible no greater than $250. The HO-6 coverage acts as excess over any other available coverage. Florida is currently the only major condo state with a statutory minimum; California, Colorado, and Washington have no equivalent statutory floor.

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

Sources & References

- Fla. Stat. §627.714 (Florida $2,000 loss-assessment minimum + $250 deductible cap)

- KRDO13: Hidden Insurance Loophole, Colorado (Mar 19, 2026; Marisa O'Malley case, 200+ DOI complaints)

- ISO HO 04 35 Unit-Owners Coverage E Special Coverage (form reference)

- IIABL Technical Advisory TA 342 (Homeowners Loss Assessment Endorsement)

- PropertyCasualty360: Standard Homeowners Endorsements Discussed, Part 2 (Oct 2024)

- Merlin Law Group: Loss Assessment Coverage Under the HO-6

- Cal. Civ. §5800 (Davis-Stirling Act, HOA master-coverage requirement)

- Cal. Ins. Code §10103 (CA residential property insurance disclosure regime)

- NBC Miami: Palm Bay Yacht Club $6.3M verdict (Dec 10, 2025)

- J. Muir & Associates: Palm Bay verdict detail

- Axios Miami: Cricket Club $134K assessment

- Brosda & Bentley: Mediterranean Village assessments (Aventura)

- NerdWallet: HO-6 Condo Insurance Guide (2026)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, real estate, or insurance advice. State insurance regulations, ISO form editions, and carrier endorsement language change frequently. Consult a qualified insurance broker and your state Department of Insurance for guidance specific to your policy and association.