In This Guide

A foreclosure condo can carry two layers of HOA risk a low price hides. First, the unit itself may owe back dues, special assessments, fines, and interest that can follow the title to you, depending on the state and how you buy. Second, a building with many foreclosures is usually financially distressed, which shows up as underfunded reserves, surprise assessments, and trouble getting a mortgage. The documents that reveal both, the estoppel certificate, the budget, and the delinquency rate, are exactly the ones you often cannot get before an auction.

The listing looks like a steal. A condo priced $60,000 under the others in the same building, flagged as a bank-owned or foreclosure sale. On paper it is the deal of the year. Then you start reading the fine print, and the reasons for the discount start to surface: unpaid HOA dues the previous owner walked away from, a special assessment the board levied last spring, and a building where a chunk of the units are in the same delinquent boat.

Foreclosure activity is climbing. US properties with foreclosure filings rose to 36,766 in October 2025, up 19% from a year earlier, the eighth straight month of annual increases, and completed foreclosures were up 32% (ATTOM). Florida had the worst foreclosure rate of any state. More distressed condos are hitting the market, and each one carries an HOA ledger the price tag does not show.

This guide explains how HOA liens are prioritized against a mortgage, what a buyer can actually inherit, the three ways you might buy a foreclosure condo and the diligence gap in each, the super-lien rules that vary sharply by state, and the building-level distress that makes many foreclosure condos hard to finance and resell. The goal is simple: know what you are buying before you bid, not after.

Why a Cheap Foreclosure Condo Is Rarely Just Cheap

A foreclosed unit is often a symptom of building-wide financial stress, not an isolated bargain, and that stress travels with the property.

When an owner stops paying a mortgage, they have usually stopped paying HOA dues too. In a healthy building that is one delinquent account the association absorbs. In a distressed building it is a pattern, and the pattern is what makes the unit cheap.

The broader condo market is already under pressure. The national median condo sale price fell to $354,100 in May 2025, down 2.2% year over year, the second-largest annual drop in Redfin's records going back to 2012, and there were roughly 80% more condo sellers than buyers nationally (Redfin). When supply outruns demand and financing gets harder, distressed units are the first to be dumped, and foreclosure condos land at the bottom of that pile.

A discount can be legitimate. But a foreclosure discount often prices in problems you will own the day you take title: an unpaid HOA balance, a levied assessment, or a building the lenders have quietly stopped approving. The rest of this guide is about telling one from the other.

How HOA Liens Work: Who Gets Paid First

An HOA lien is usually junior to the first mortgage, so a lender foreclosure clears most unpaid dues, except a protected slice in super-lien states.

An HOA or condo association assessment lien attaches automatically when an owner falls behind on dues. In most states the association's recorded declaration serves as notice of that lien, so no separate filing is required. The question that decides who pays is priority: when a property is sold at foreclosure, which liens get paid from the proceeds, and in what order.

The default rule in nearly every state is that the HOA lien is subordinate to the first mortgage. Because the mortgage outranks the HOA lien, a foreclosure of that first mortgage generally extinguishes the HOA's claim for pre-foreclosure dues. That is good news for a buyer of a bank-owned unit, up to a point.

The exception is the super-lien. About 20 states plus the District of Columbia flip a limited slice of the HOA lien, usually the most recent six months of assessments, so that it primes even the first mortgage (Nolo). That six-month figure comes from the model Uniform Common Interest Ownership Act, Section 3-116. A few states go further: Nevada and Connecticut protect nine months. That protected slice survives a mortgage foreclosure and has to be paid, usually by whoever ends up owning the unit.

So the same unpaid $12,000 dues balance can behave completely differently by state. In a non-super-lien state, a lender foreclosure clears almost all of it. In a super-lien state, six to nine months of it climbs above the mortgage and lands on the next owner. We will map the states below.

What You Can Inherit: Dues, Assessments, Fines, and Interest

Outside a lender foreclosure, a new owner is often jointly liable for the prior owner's unpaid assessments, plus interest, fines, and costs.

Absent the protection of a lender foreclosure, a new owner can be on the hook for the prior owner's debt. Under the model Uniform Common Interest Ownership Act, and in many states including Florida, a new owner is jointly and severally liable with the seller for the prior owner's unpaid assessments. Florida states it plainly. Under Fla. Stat. §718.116(1)(a), a unit owner, "regardless of how his or her title has been acquired, including by purchase at a foreclosure sale or by deed in lieu of foreclosure," is liable for assessments that come due while they own it, and is "jointly and severally liable with the previous owner for all unpaid assessments that came due up to the time of transfer of title."

The balance that follows the unit is rarely just back dues. It can include:

- Delinquent regular assessments the previous owner never paid.

- Special assessments that were levied but unpaid at the time of foreclosure.

- Interest. Florida assessment liens accrue up to 18% interest (§718.116(3)).

- Late fees, fines, and attorney or collection costs that the association added to the lien.

This is why the estoppel certificate (called a resale certificate or status letter in some states) matters so much. It is the association's written statement of exactly what is owed on the unit. A buyer who orders one before closing knows the number they are inheriting. A buyer who skips it, or who buys at an auction where getting one in time is impossible, does not. We cover the broader question of who pays the special assessment at closing in a dedicated guide.

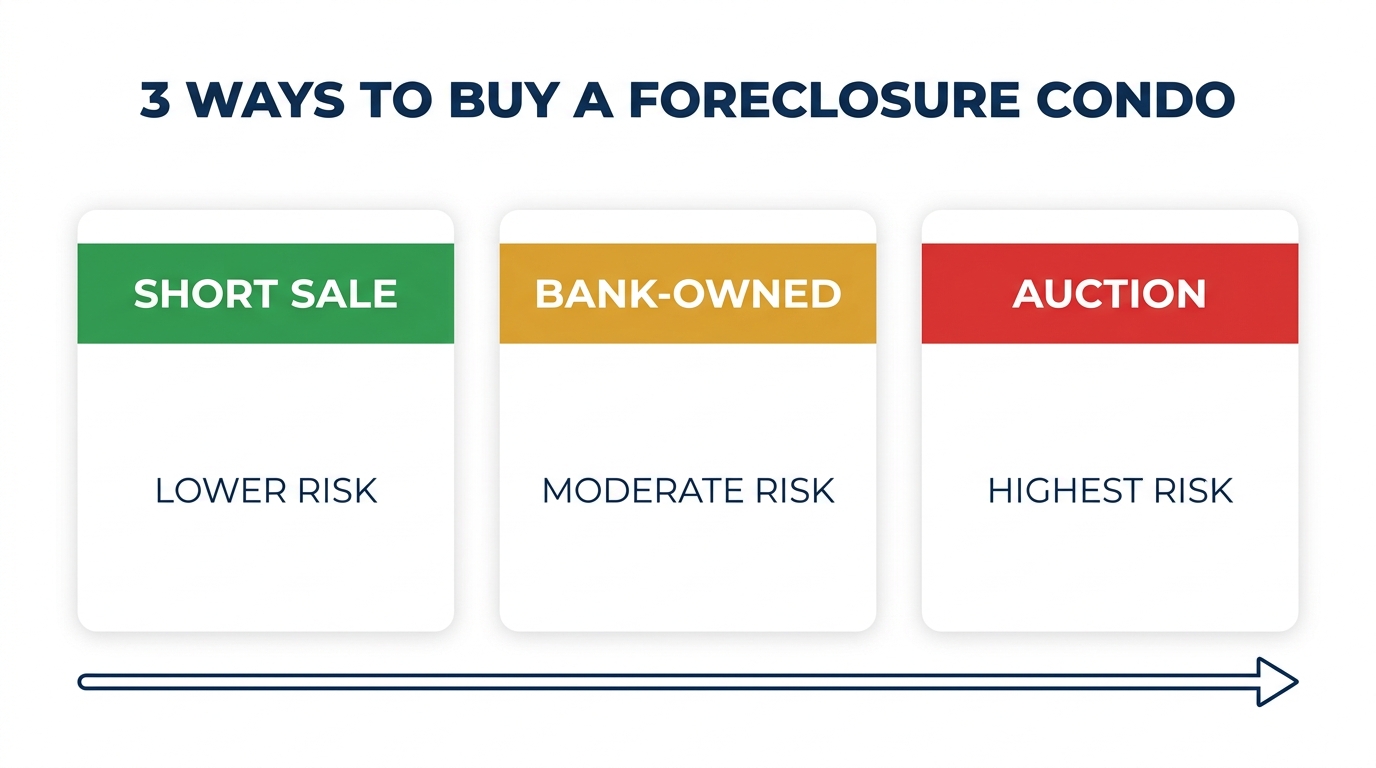

The Three Ways to Buy a Foreclosure Condo

Pre-foreclosure, bank-owned, and courthouse auction differ mainly in how much you can learn before you commit. Auctions give you the least.

"Foreclosure" covers three very different transactions. The single biggest difference for a buyer is the diligence gap: how much you can learn about the unit and the building before you are bound to buy.

Pre-foreclosure and short sale: lowest risk

The owner still holds title, so the sale closes like any other. You can order an estoppel certificate, read the CC&Rs, budget, and reserve study, inspect the unit, and arrange financing. Any unpaid HOA balance is disclosed and typically paid off at closing. The main drawback is friction: the lender has to approve a below-balance payoff on a short sale, so these deals can drag or collapse.

Bank-owned (REO): moderate risk

Here the lender has already foreclosed and taken title, which usually clears the defaulted borrower's junior liens. Two traps remain. In super-lien states, the protected six-to-nine-month slice can survive, and in Florida the foreclosing lender owes a safe-harbor amount it may not have fully paid. Whatever the bank did not clear can remain an open association balance that follows the unit. You can still order an estoppel certificate, buy an owner's title policy, and insist the HOA balance is cleared at closing, so REO is workable if you do the paperwork.

Courthouse auction and trustee sale: highest risk

This is where buyers get hurt. Auction units sell as-is, all-cash, with no inspection, often with no access to the interior, and usually with no way to obtain HOA documents, the reserve study, or an estoppel certificate before you bid. You can take title subject to unpaid assessments, special assessments, fines, interest, and collection costs. And as the next section explains, the safe-harbor protection that shields a foreclosing lender does not extend to a third-party buyer at the auction.

| Purchase channel | Can you get an estoppel / docs first? | HOA risk level |

|---|---|---|

| Pre-foreclosure / short sale | Yes, full diligence and financing possible | Lower |

| Bank-owned (REO) | Usually, order before closing | Moderate (super-lien / safe-harbor residue) |

| Courthouse auction / trustee sale | Rarely, sold as-is, no time for docs | Highest |

The Super-Lien Trap and the Florida Safe Harbor

State law decides how much of the old dues survive a foreclosure, and in a few states an HOA foreclosure can even wipe out the mortgage.

How much of the prior owner's HOA debt lands on you turns almost entirely on state law. Three patterns matter.

Super-lien states. About 20 states plus DC give the HOA a limited priority over the first mortgage, typically the last six months of assessments. Foreclosure of that slice survives even a lender foreclosure. In a handful of states the priority period is longer.

Florida's safe harbor. Florida is not a super-lien state. Instead of elevating dues above the mortgage, it caps how much a foreclosing first mortgagee owes. Under Fla. Stat. §718.116(1)(b), a lender that takes title by foreclosure is liable for the lesser of 12 months of assessments or 1% of the original mortgage debt. The critical trap: that cap protects the bank, not you. A third-party buyer at the foreclosure auction gets no safe harbor and takes the unit under the full joint-and-several liability of §718.116(1)(a).

HOA foreclosure that beats the mortgage. In a few true super-lien states, an association foreclosing its own super-priority lien can extinguish the first mortgage entirely. The landmark case is Nevada's SFR Investments Pool 1, LLC v. U.S. Bank, 334 P.3d 408 (Nev. 2014), where the state Supreme Court held that a proper foreclosure of the nine-month super-priority portion wiped out the bank's deed of trust. Investors bought units for the cost of a few months' dues. Nevada later tightened the notice rules with SB 306 (effective October 2015), but the nine-month super-lien remains on the books.

| State | Rule | Protected amount |

|---|---|---|

| Model act (UCIOA §3-116) | Super-lien primes first mortgage | 6 months of assessments |

| Colorado, Washington, Massachusetts, DC, and others | Super-lien | 6 months |

| Nevada, Connecticut | Super-lien (longer) | 9 months |

| Florida | Safe harbor caps lender liability (not a super-lien) | Lesser of 12 months or 1% of original mortgage |

| Most other states | HOA lien junior to first mortgage | Mortgage foreclosure clears most dues; HOA foreclosure takes subject to the mortgage |

Two takeaways. If you buy at an HOA foreclosure auction in an ordinary state, you likely take the unit subject to the existing mortgage, which means the lender can still foreclose and you can lose the property unless you pay off or reinstate that loan. And in Florida, buying at the auction as a third party strips you of the lender safe harbor entirely. Both are situations to run past a real estate attorney before bidding, not after.

The Bigger Risk: Buildings Where Everyone Stopped Paying

When too many owners are delinquent, the building becomes non-warrantable, financing dries up, and resale gets hard, however clean your own unit is.

The unit-level lien is the risk buyers think about. The building-level risk is the one that quietly costs more. When many owners in a building stop paying, the association runs short, defers maintenance, and eventually levies emergency special assessments. Past a threshold, the whole project stops qualifying for standard financing.

Fannie Mae will not back a loan in a project where more than 15% of units are 60 or more days past due on common expense assessments, and it applies the same 15% test separately to any special assessment (Selling Guide B4-2.2-02). FHA uses the same 15% delinquency ceiling for condo project approval. Fannie also requires the budget to fund reserves at at least 10% of assessment income, rising to 15% for loan applications dated on or after January 4, 2027 under Lender Letter LL-2026-03.

The cascade runs like this: foreclosures push delinquency past 15%, the project becomes non-warrantable, conventional and FHA buyers can no longer get loans, the buyer pool shrinks to cash investors, prices fall further, and the next owner has the same trouble reselling. A cheap foreclosure unit in that kind of building can become a unit you cannot sell to a financed buyer later. The HOA delinquency rate is the single number that tells you whether you are walking into this, which is why lenders and careful buyers ask for it first.

Florida shows the pattern at scale. Post-Surfside laws requiring milestone inspections and Structural Integrity Reserve Studies have forced boards to fund long-neglected reserves, and some have passed assessments owners cannot afford. At the Cricket Club in North Miami, the association levied roughly a $30 million assessment, about $134,000 per unit, and owners were forced to sell into a falling market, one unit listed near $350,000 and ultimately sold for around $110,000 (Axios Miami). That is the building-level distress a foreclosure buyer can inherit through unpaid assessments and lost financing, well before any individual lien is counted. Our Florida condo crisis guide covers the statutory drivers in depth.

How to Screen a Foreclosure Condo Before You Bid

Order the estoppel certificate, verify the building's delinquency rate and reserves, and confirm how your state treats surviving liens.

The whole game is getting the documents before you are committed. Work through this list, and treat any channel that will not let you complete it as a higher-risk purchase:

- Order the estoppel or resale certificate in writing. This is the association's statement of exactly what the unit owes. Fee caps and delivery windows vary by state, Florida caps the fee (currently around $299) and requires delivery within 10 business days under §718.116(8); Texas caps a resale certificate at $375 with 10 business days under Property Code §207.003; California allows only the association's actual cost under Civ. Code §4530.

- Ask for the building's delinquency rate. What percentage of units are 60-plus days behind? Above 15% and the project is likely non-warrantable. See our delinquency-rate guide.

- Read the reserve study and budget. Thin reserves plus deferred maintenance signal a special assessment ahead. Our reserve study guide and HOA budget red flags show what to look for.

- Check for levied and pending special assessments. An approved assessment can transfer with the unit even if it is not yet billed.

- Confirm how your state treats surviving liens. Super-lien, safe harbor, or junior lien changes what you owe. This is a question for a local real estate attorney, especially at auction.

- Buy an owner's title policy and clear all HOA balances at closing. Title insurance generally covers recorded liens, not unrecorded assessment balances known only from the association's books, so an estoppel plus a clean closing is the real protection.

- Confirm financeability early. If you plan to use a mortgage, have your lender review the project before you bid. A non-warrantable building can kill the loan regardless of your credit.

For a document-by-document walkthrough that applies to any condo purchase, foreclosure or not, see the complete condo buying checklist.

Frequently Asked Questions

Do I have to pay the previous owner's unpaid HOA dues on a foreclosure condo?

It depends on how you buy and which state you are in. In most states, a lender (mortgage) foreclosure wipes out the association's claim for pre-foreclosure dues, except a protected super-lien slice (usually 6 months, 9 in Nevada and Connecticut) in about 20 states plus DC. If you buy as a third party at an HOA foreclosure auction, or outside a foreclosure, you are often jointly liable for the prior owner's unpaid assessments. Always order an estoppel certificate to confirm the exact balance.

What is a super-lien and why does it matter for foreclosure condos?

A super-lien gives an HOA limited priority over the first mortgage for a set amount of recent assessments, typically 6 months. About 20 states plus DC have one. It matters because that protected slice survives a mortgage foreclosure and must be paid by the new owner, and in a few states (notably Nevada), foreclosure of the super-priority portion can even extinguish the first mortgage entirely.

Does Florida have an HOA super-lien?

No. Florida uses a safe harbor instead. Under Fla. Stat. §718.116(1)(b), a first mortgagee that forecloses is liable for the lesser of 12 months of assessments or 1% of the original mortgage debt. That cap protects the lender, not a third-party buyer at the auction, who takes the unit under full joint-and-several liability for all unpaid assessments under §718.116(1)(a).

Is buying a condo at a courthouse foreclosure auction risky?

It carries the highest HOA risk of the three foreclosure channels. Auction units sell as-is, all-cash, with no inspection and usually no way to obtain HOA documents, a reserve study, or an estoppel certificate before you bid. You can take title subject to unpaid assessments, fines, and interest, and in ordinary states an HOA-auction buyer takes the unit subject to the existing mortgage. Consult a real estate attorney before bidding.

Why are foreclosure condos hard to finance?

A building with many foreclosures usually has high dues delinquency. Fannie Mae and FHA will not approve financing in a project where more than 15% of units are 60 or more days past due on assessments, and Fannie also requires reserves funded at 10% of income, rising to 15% in January 2027. A foreclosure condo in a distressed building can be non-warrantable, limiting buyers to cash and making resale harder.

How do I find out what a foreclosure condo really owes the HOA?

Order an estoppel certificate (called a resale certificate or status letter in some states) in writing from the association. It is the official statement of unpaid dues, special assessments, fines, interest, and collection costs on the unit. Fee caps and delivery windows are set by state law, for example 10 business days in Florida and Texas. The catch is that you usually cannot get one in time before a courthouse auction, which is why auctions are the riskiest way to buy.

Get Your HOA Documents Analyzed

GoverningDocs analyzes CC&Rs, reserve studies, and meeting minutes, identifying red flags, restrictions, and financial risks so you can buy with confidence. Free. No signup required.

Your first full property report is also free. See what you'll get →

Or get your first full report free →Related Articles

Sources & References

- ATTOM October 2025 Foreclosure Market Report (36,766 filings, up 19% YoY; completed foreclosures up 32%; Florida worst state rate)

- Redfin condo price report, May 2025 (median $354,100, down 2.2% YoY; ~80% more condo sellers than buyers)

- Fla. Stat. §718.116 (joint-and-several liability, safe harbor, 18% lien interest, estoppel certificate)

- SFR Investments Pool 1, LLC v. U.S. Bank, 334 P.3d 408 (Nev. 2014) (HOA super-priority foreclosure extinguishes first deed of trust)

- Nolo (HOA/COA lien priority and super-lien states overview)

- Texas Property Code §207.003 (resale certificate: $375 cap, 10 business-day delivery)

- California Civil Code §4530 (association may charge only actual cost for the resale disclosure documents)

- Fannie Mae Selling Guide B4-2.2-02 (15% delinquency ceiling; 10% reserve requirement)

- Fannie Mae Lender Letter LL-2026-03 (reserve minimum rising from 10% to 15% Jan 4, 2027)

- Axios Miami (Cricket Club ~$30M assessment, ~$134,000 per unit; forced sales into a falling market)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. HOA lien priority, super-lien, foreclosure, and estoppel rules vary by state, by the specific community's governing documents, and by how the property is purchased, and the statutes referenced are amended frequently. Figures are current as of July 2026 and may be superseded. Consult a qualified real estate attorney before bidding on or buying a foreclosure condominium in your state.