In This Guide

Low HOA fees are not a bargain. Over 70% of HOAs are underfunded, and the buildings with the lowest fees are often the ones deferring the most maintenance. That deferred maintenance eventually arrives as a special assessment that can reach $100,000 or more per unit.

You're comparing two condos. Same neighborhood, similar square footage. One has HOA dues of $450 a month. The other is $175. The cheaper one looks like the obvious winner.

Until it isn't. Six months after closing, the board announces a special assessment of $85,000 per unit. The roof needs replacing. The elevator is past its useful life. The reserve fund is nearly empty because fees were kept artificially low for years.

This is not a hypothetical. It's happening right now in hundreds of condo buildings across Florida, California, and the Northeast. Low HOA fees feel like a win at the closing table. But they're often a signal that the real costs have been pushed into the future. Here's how to spot the difference between genuinely affordable dues and a financial time bomb.

What HOA Fees Actually Pay For

HOA fees fund two buckets: day-to-day operating expenses and long-term reserve savings for major repairs like roofs, elevators, and plumbing.

Every HOA budget has two parts. The operating fund covers daily expenses: landscaping, insurance, management fees, utilities, and routine maintenance. The reserve fund is savings for big-ticket items that wear out over time: roofs, elevators, parking structures, plumbing systems, and exterior painting.

A healthy HOA allocates 15% to 40% of total assessment income toward reserves. When boards cut fees to keep owners happy, the reserve contribution is almost always the first thing that gets slashed. The operating costs are fixed. You can't skip the electric bill. But you can skip saving for a roof that won't fail for another decade.

The problem is that the roof does eventually fail. And when it does, there's no money to fix it.

The Reserve Funding Crisis: Over 70% of HOAs Are Underfunded

Industry data from 100,000+ reserve studies shows over 70% of HOAs fall below the 70% funded threshold considered adequate.

Association Reserves, one of the largest reserve study firms in the country, analyzed over 100,000 reserve studies from 1986 to 2025 and found that 74% of associations were below 70% funded. That number has gotten worse over time, rising from 62% in the early 1990s.

A separate 2026 report from HOAstart found that roughly one-third of associations report reserves below 50% funded (high risk), and 48% report below 60% funded or don't know their funding level at all.

What does percent funded mean? It's the ratio of actual reserve dollars on hand versus what the association should have saved by now based on the age of its components. Here's how industry professionals read the number:

| Percent Funded | Rating | Special Assessment Risk |

|---|---|---|

| 70% or higher | Strong | Rare. Enough reserves to do projects on schedule. |

| 30% to 69% | Fair | Possible. Funding gap needs attention before it grows. |

| Below 30% | Poor / Critical | High. Major repairs likely deferred. Assessment probable. |

The connection to low fees is direct. Associations that keep monthly dues low are almost always doing it by shortchanging the reserve fund. A building that should be contributing $200 per unit per month to reserves but only contributes $50 will look cheaper on paper. The gap grows every year until a major repair forces the board's hand.

How Low Fees Lead to Six-Figure Special Assessments

Boards keep fees low by deferring maintenance for years. When repairs can't wait any longer, the full cost lands on owners as a lump-sum assessment.

The mechanism is straightforward. The board holds fees steady (or even reduces them) to avoid complaints from owners. Reserve contributions get cut. Maintenance gets pushed back. A roof that should have been replaced at year 20 limps along to year 30.

Then the roof fails. Or the elevator breaks. Or the building fails an inspection. Suddenly the board needs $5 million and the reserve fund has $300,000. The only option is a special assessment split across all owners.

Cedar Management Group calls low HOA fees "an association's enemy" that "will certainly backfire." They identify five risks: deferred maintenance, property value decline, legal compliance failures, economic unsustainability, and eventual special assessments.

Communities that update their reserve studies more frequently than once every five years see 35% lower subsequent special assessments, according to Association Reserves. Regular studies force boards to confront the gap between what they're collecting and what they actually need.

Real Buildings That Kept Fees Low (and What It Cost)

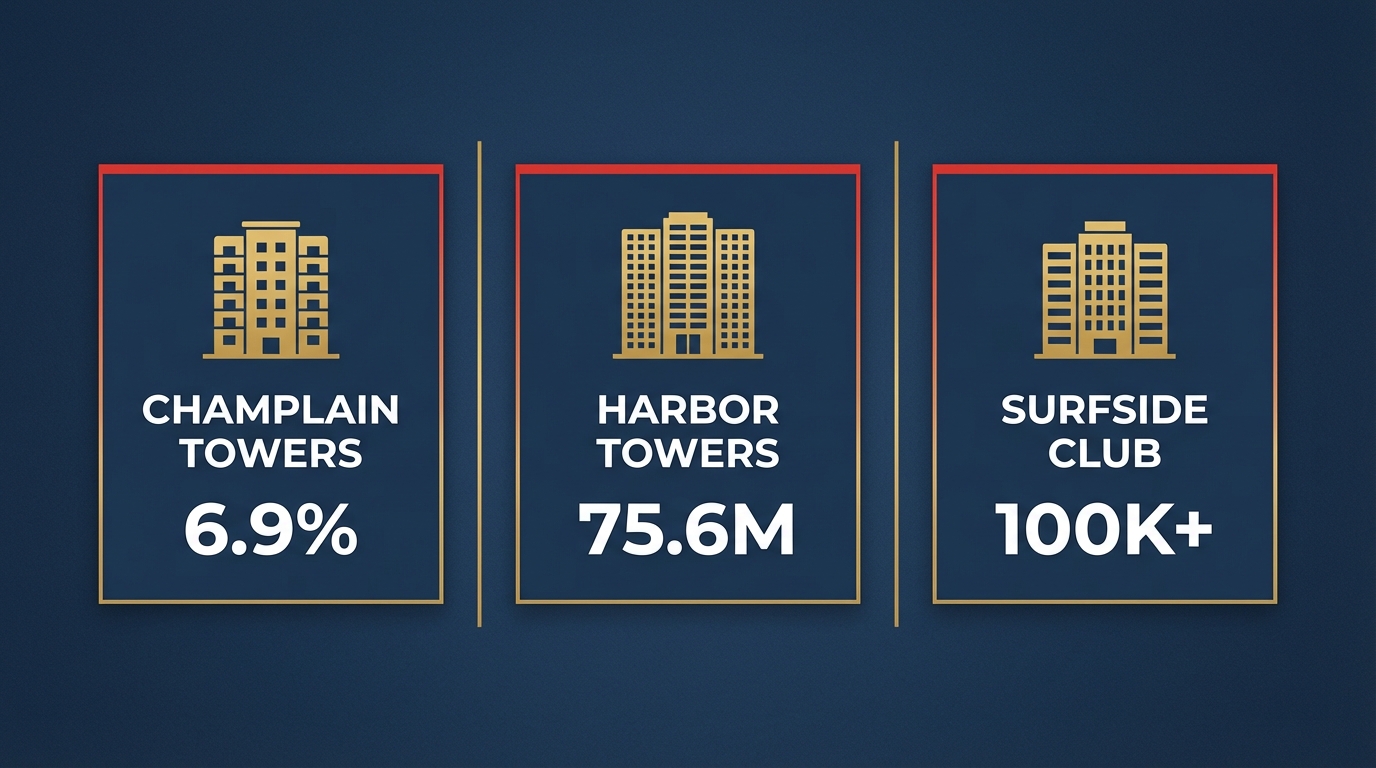

Champlain Towers was 6.9% funded. Harbor Towers hit owners with $120K+ per unit. SurfSide Club South forced a retired teacher back to work.

| Building | Assessment Per Unit | What Happened |

|---|---|---|

| Champlain Towers South, Surfside FL | $80K – $336K | 6.9% funded. $15M assessment levied April 2021. Building collapsed June 2021. 98 killed. |

| Harbor Towers, Boston MA | ~$120K (avg); up to $400K+ | Built 1971. No major renovations for decades. $75.6M total assessment. |

| SurfSide Club South, Ormond Beach FL | $100K+ | Driven by FL SB 4-D safety requirements. Owners forced back to work. |

Champlain Towers South is the most extreme example. The 12-story Surfside building had $777,000 in reserves against $16.2 million in needed repairs. Its reserve study showed just 6.9% funded. A 2018 engineering assessment by Morabito Consultants found "major structural damage" including cracking in columns, beams, and walls. The board delayed repairs for years. In April 2021 they levied a $15 million special assessment. The building collapsed two months later.

Harbor Towers in Boston told a similar story without the tragedy. Two 40-story waterfront high-rises built in 1971 went decades without major renovations. The eventual bill: $75.6 million, believed to be the largest special assessment in Boston history. Average per-unit cost hit $120,000, with larger units exceeding $400,000. Many residents moved out rather than pay.

At SurfSide Club South in Ormond Beach, Florida, retired teacher Janet Stone told Yahoo Finance: "I'm a retired teacher so we don't have hundreds of thousands of dollars set aside somewhere that we can contribute so it put me in a position where I had to return to work."

The common thread: years of artificially low fees that avoided the political pain of raising dues. By the time the bills came due, the gap was too large for gradual increases to close.

What Fannie Mae and Freddie Mac Require

Currently 10% of budget must go to reserves. Increasing to 15% on January 4, 2027. Buildings below the threshold become non-warrantable.

Fannie Mae and Freddie Mac set minimum standards for condo buildings to qualify for conventional mortgages. If a building doesn't meet the standard, it's classified as non-warrantable and buyers lose access to conventional financing.

The current rule: at least 10% of total annual budgeted assessment income must be allocated to reserves. Starting January 4, 2027, that minimum jumps to 15%.

There's one exception to the 15% rule. If the condo has a reserve study conducted or updated within the past three years and the association is following the highest recommended funding level (not baseline funding), the 15% minimum doesn't apply.

For buildings with low fees and thin reserves, this creates a squeeze. A building allocating only 5% to reserves is currently non-warrantable. After January 2027, buildings at 10% to 14% will also fail unless they have a recent reserve study proving adequate funding.

IQRate Mortgages warns that a building with a low HOA fee today could see it "double or triple in the next year" to comply with new lending standards and state safety laws.

How to Tell If HOA Fees Are Too Low

Request the reserve study, check percent funded, compare reserve allocation to the 10-15% minimum, and look for assessment history.

Not every building with low fees is a problem. A small townhome community with no pool, no elevator, and a new roof may genuinely have low expenses. The red flags show up when you look at the documents.

Eight red flags that fees are too low

- No reserve study, or a study older than 5 years. If the board hasn't commissioned a study, they may not know how underfunded they are. If the study is stale, the numbers are meaningless.

- Percent funded below 30%. This is the "critical" range. Special assessments are not a question of if, but when.

- Reserve allocation below 10% of budget. Below the Fannie Mae minimum. The building is already non-warrantable.

- History of special assessments. Recurring "emergency" assessments signal chronic underfunding, not bad luck.

- No dues increases in 5+ years. Operating costs and construction costs rise every year. Flat fees mean the gap is growing.

- Borrowing from reserves for operating expenses. This is a sign the operating budget is also underfunded. Reserves are being raided to keep the lights on.

- Deferred maintenance visible on inspection. Peeling paint, cracked parking lots, aging roofs, and rusted railings tell you where the money isn't going.

- High delinquency rate. If owners aren't paying current (low) fees, they definitely won't pay higher ones. Revenue is below even budgeted amounts.

Upload the reserve study and budget to the free reserve study analysis tool to get a percent-funded score and flag any of these issues automatically.

What Healthy HOA Fees Look Like

The national median is $135/month (2024 Census). Healthy fees rise gradually each year and allocate 15-40% of the total budget toward reserves.

The first national HOA fee data from the U.S. Census Bureau (2024 American Community Survey) gives us real benchmarks. The national median is $135 per month. About 26% of fee-paying households pay less than $50. At the high end, 3 million households pay more than $500.

Fees vary dramatically by state and property type (state data from Florida Realty Marketplace):

| Location | Median HOA Fee |

|---|---|

| National median | $135/month |

| Florida statewide | $230/month |

| New York (highest state) | $739/month |

| Miami high-rises | $835/month (median, all condos) |

A condo with fees significantly below comparable buildings in the same market should trigger further investigation. If every similar high-rise in the neighborhood charges $600 and one charges $250, the question isn't "why are those buildings so expensive?" The question is "what is this building not paying for?"

Healthy HOA fees share a few characteristics:

- Gradual, regular increases that keep pace with inflation and rising construction costs (typically 3-5% per year)

- 15% to 40% of total assessments allocated to the reserve fund

- Reserve study updated every 3 years with the board following the recommended funding plan

- Percent funded at 70% or higher based on the most recent study

Frequently Asked Questions

What is a normal HOA fee?

The national median HOA fee is $135 per month according to the 2024 U.S. Census American Community Survey. However, fees vary widely by location and property type. Florida condos average $230, New York leads at $739, and Miami high-rises commonly exceed $800. Compare fees against similar buildings in the same market, not national averages.

Are low HOA fees always bad?

Not always. Small communities with limited common areas (no pool, no elevator, no parking garage) may genuinely have low expenses. The red flag is low fees combined with underfunded reserves, no recent reserve study, deferred maintenance, or a history of special assessments. Always check the reserve study and percent funded level before assuming low fees are a bargain.

How much should HOA reserves be funded?

Industry professionals consider 70% funded or higher to be adequate. Below 30% is considered critical, with a high likelihood of special assessments. Fannie Mae and Freddie Mac currently require at least 10% of annual assessment income to go toward reserves, increasing to 15% on January 4, 2027.

Can HOA fees go up after I buy?

Yes. HOA boards can increase fees and levy special assessments at any time, subject to state law and the association's governing documents. In Florida, new laws (SB 4-D, HB 913) now prohibit associations from waiving reserve funding for structural components, which is forcing fee increases across the state. Buildings that kept fees artificially low for years are seeing the largest increases.

How do I check if an HOA's reserves are underfunded?

Request the most recent reserve study and look for the percent funded level. Also review the operating budget to see what percentage goes to reserves (should be at least 10-15%). Check board meeting minutes for discussions about deferred maintenance or special assessments. You can upload reserve studies to GoverningDocs' free analysis tool for an instant assessment.

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Related Articles

Sources & References

- Association Reserves (100,000+ reserve study analysis, percent funded data)

- U.S. Census Bureau, 2024 American Community Survey (national median HOA fee, $135/month)

- HOAstart 2026 Reserve Report (one-third of associations below 50% funded)

- Cedar Management Group ("Low HOA fees are an association's enemy")

- CAI Advocacy Blog (Fannie/Freddie reserve requirement increase to 15%)

- CNN Investigation (Champlain Towers South reserve fund analysis)

- Boston City Properties (Harbor Towers $75.6M special assessment)

- Yahoo Finance (SurfSide Club South owner stories)

- AllPropertyManagement (35% lower assessments with regular reserve study updates)

- Florida Realty Marketplace (Florida HOA fee data by city)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. HOA fee adequacy depends on the specific building, its age, amenities, location, and reserve study results. Consult a qualified real estate attorney or financial advisor for guidance specific to your situation.