A non-warrantable condo is a unit in a building that does not meet Fannie Mae or Freddie Mac guidelines for conventional mortgage financing. Buyers need portfolio loans with higher rates and larger down payments.

When a lender reviews your mortgage application for a condo, they don't just look at your credit score and income. They also evaluate the building itself. If the condo project fails Fannie Mae or Freddie Mac eligibility criteria, the building is classified as "non-warrantable." That means conventional 30-year fixed-rate mortgages are off the table for every unit in the building.

This matters because most buyers rely on conventional financing. When that option disappears, the pool of eligible buyers shrinks significantly. The result: harder sales, longer time on market, and often lower prices.

What Makes a Condo Non-Warrantable?

Fannie Mae evaluates six project-level criteria. Failing any single one makes the entire building non-warrantable.

These are the six Fannie Mae criteria that determine warrantability. The reserve funding threshold will increase from 10% to 15% in the January 2027 Fannie/Freddie guideline update.

Reserve funding below 10% of annual budget. Increasing to 15% in January 2027. The HOA must allocate at least 10% of its annual operating budget to reserves (15% starting January 2027).

More than 15% of owners 60+ days delinquent on dues. High delinquency signals financial instability. Lenders treat this as a serious risk factor.

Single entity owns more than 20% of units. High investor concentration suggests the building may be rental-heavy, which increases lender risk.

More than 25% of building is commercial space. Mixed-use buildings with too much commercial area don't qualify for conventional condo financing.

Active or pending litigation against the HOA. Material lawsuits (construction defect claims, large financial judgments) can disqualify a project. Routine liability claims typically do not.

Inadequate insurance coverage. The master policy must provide replacement cost coverage, not actual cash value (ACV). Coverage gaps or non-renewal also disqualify a building.

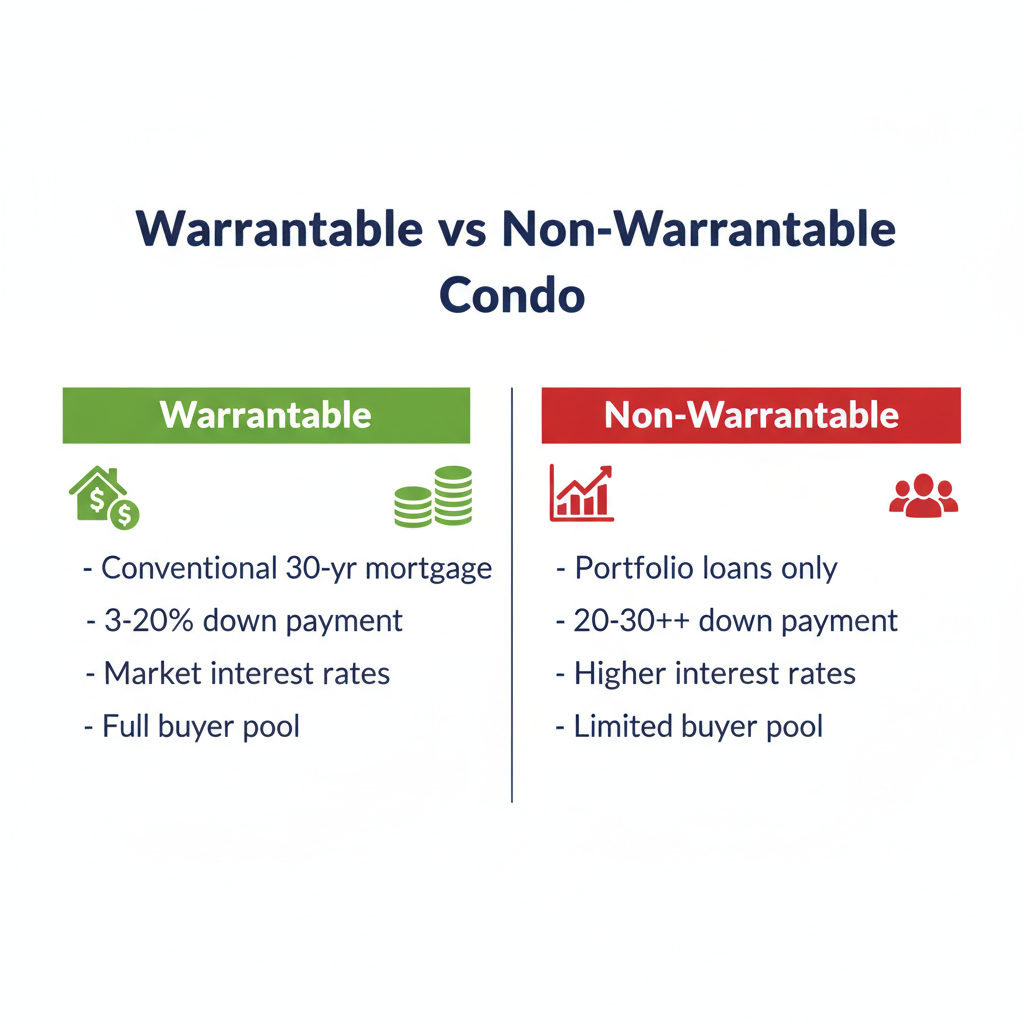

Warrantable vs Non-Warrantable: Key Differences

| Warrantable | Non-Warrantable | |

|---|---|---|

| Financing | Conventional 30-yr fixed | Portfolio/jumbo only |

| Down payment | 3-20% | 20-30%+ |

| Interest rate | Market rate | 0.5-2% higher |

| Buyer pool | All qualified buyers | Cash + portfolio borrowers |

| Resale value | Standard | Typically discounted |

How Non-Warrantable Status Affects Buyers

Non-warrantable status limits financing options, shrinks the buyer pool, and can reduce resale value. But it is not permanent.

The most immediate impact is on financing. Conventional lenders cannot approve loans for units in non-warrantable buildings. Buyers must use portfolio loans, which come with higher interest rates (typically 0.5% to 2% above market) and larger down payments (20-30% or more). Some buyers simply walk away when they learn the building doesn't qualify.

The smaller buyer pool creates a ripple effect on pricing. Fewer eligible buyers means less competition for your unit. Sellers often need to discount their asking price to attract cash buyers or portfolio borrowers who expect a better deal to offset their higher financing costs.

The good news: non-warrantable status can change. Buildings can regain warrantable status by fixing the specific issue that caused the classification. If reserves are increased, delinquency drops below the threshold, or litigation resolves, a lender can reassess the project and reclassify it.

How to Check If a Condo Is Warrantable

Three ways to check: ask your lender for a warrantability review, look up the building in the Fannie Mae Condo Project Manager, or review the HOA documents yourself.

Ask your lender. The simplest approach. Any mortgage lender can run a warrantability check on a condo project as part of the loan process. This is free and typically takes a few business days.

Check the Fannie Mae Condo Project Manager (CPM). Fannie Mae maintains a searchable database of condo projects that have been reviewed. Not all buildings are listed, but if yours is, you can see its current eligibility status.

Review HOA documents yourself. Pull the reserve study to check funding levels, ask for the current delinquency rate, and review board minutes for litigation. Upload your CC&Rs to GoverningDocs' free CC&R analyzer to extract rental restrictions, assessment language, and maintenance obligations. Upload your reserve study to the free reserve study analyzer to find percent funded, budget allocation, and components at end of useful life.

Frequently Asked Questions

Can you get a mortgage on a non-warrantable condo?

Yes, but not a conventional mortgage. You'll need a portfolio loan or jumbo loan from a lender that keeps the loan on its own books instead of selling it to Fannie Mae or Freddie Mac. Expect higher interest rates and a larger down payment (typically 20-30%).

What makes a condo non-warrantable?

Six Fannie Mae criteria: reserve funding below 10% of annual budget (increasing to 15% in January 2027), more than 15% of owners delinquent on dues, single entity owning 20%+ of units, over 25% commercial space, active litigation against the HOA, or inadequate insurance coverage. Failing any one disqualifies the building.

Can a non-warrantable condo become warrantable?

Yes. Non-warrantable status is not permanent. If the HOA fixes the failing criteria (increases reserves, reduces delinquency, settles litigation, restores insurance coverage), a lender can reclassify the building as warrantable after a new project review.

How do I check if a condo is warrantable?

Ask your mortgage lender to run a warrantability check (free, takes a few days). You can also search the Fannie Mae Condo Project Manager. For a DIY approach, review the reserve study, delinquency rate, and board minutes for red flags.

Check Your Building's Warrantability

Upload your HOA documents for free analysis. No signup required.

Want the full deep dive? Read our detailed blog post on non-warrantable condos →

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. HOA documents, reserve funding requirements, and lender criteria vary significantly by state, lender, and association. Consult a qualified professional for guidance specific to your situation.