Condo prices are falling because of rising HOA fees, insurance costs, and special assessments. Savvy buyers can find real deals in this market, but only by checking HOA documents to separate discounted buildings from distressed ones.

A two-bedroom condo in Tampa listed at $280,000 just dropped to $240,000. The listing says "motivated seller." You run the numbers and monthly payments look great. This could be the deal you've been waiting for.

Or it could be a building about to hit every owner with a $40,000 special assessment.

Condo prices are falling across the country, and the discounts are real. But not every discount is a deal. Some buildings are cheap because the market is soft. Others are cheap because the building is in trouble. The difference is in the HOA documents. Here's how to tell which is which.

What's Happening to Condo Prices Right Now?

Condo prices fell 2.2% nationally while single-family homes rose 0.5%. Florida condos are down 4.7-6.1% statewide, with some metros down 19-32%.

The national median condo price dropped 2.2% year-over-year in mid-2025. That's the second-largest decline on record, according to Redfin data going back to 2012. Single-family homes rose 0.5% over the same period. That 2.7-percentage-point gap is the widest divergence in years.

Condos are also sitting on the market significantly longer than houses. In August 2025, the typical condo took 58 days to go under contract, roughly two weeks longer than the year before and the highest August level in 12 years.

Florida is the epicenter. Statewide condo prices fell 4.7-6.1%, but individual metros are far worse. Tampa is down 19%. Deltona and Crestview are down over 30%. In Miami, there are 13.7 months of condo inventory on the market. In South Florida, over 90% of condo sales are closing below original asking price. In Fort Lauderdale, sellers are taking an average 10.3% discount. Nationally, 68% of condos sold below list price in 2025.

For context, a balanced market has 4-6 months of inventory. Florida condos have two to three times that. Buyers have leverage they haven't had in years.

Why Condos Are Falling While Houses Hold Steady

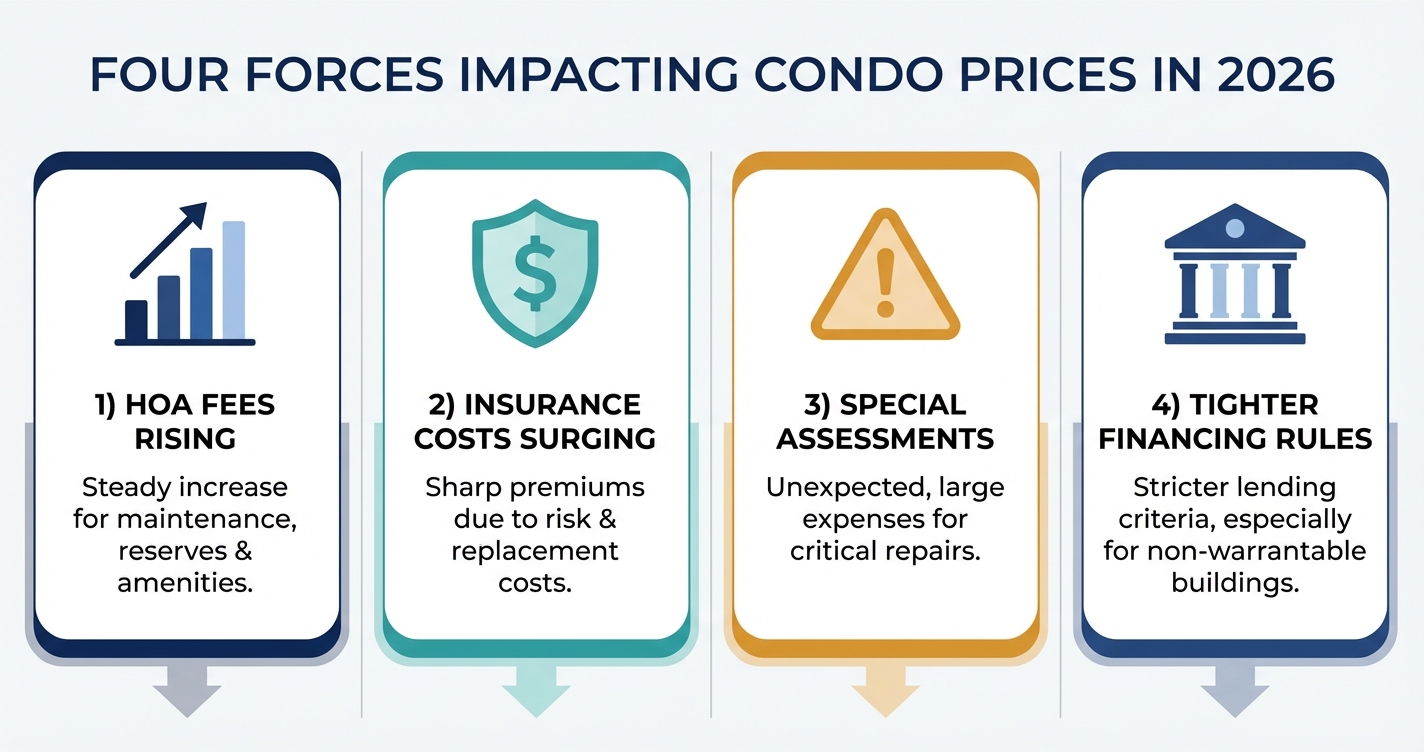

A perfect storm of rising HOA fees, insurance costs, special assessments, and tighter lending rules is hitting condos. Houses don't have these problems.

Single-family homes and condos are diverging because condos carry costs that houses don't. Four forces are compounding at once.

HOA Fees Nearly Doubled

Since the Surfside condo collapse in 2021, HOA fees have surged across Florida. In Miami-Dade County, median monthly condo fees jumped nearly 60% between 2019 and 2023. Florida led the way after SB 4-D required structural inspections and mandatory reserve funding. Tampa HOA fees jumped 17.2% in a single year. Orlando rose 16.7%. Fort Lauderdale rose 16.2%. Those are the biggest increases in the country.

As of January 1, 2025, Florida condo associations can no longer waive reserve contributions. Every building must fund reserves. For buildings that deferred maintenance for years, fees had to spike to catch up.

Insurance Is More Than Double the National Average

Florida condo insurance averages $1,049 per year. The national average is $455. That's 2.3 times the national rate. In Miami, average condo insurance hits $2,570 per year. Some buildings have lost coverage entirely, forcing owners into the state's insurer of last resort.

Florida home insurance spiked another 18% in 2025 alone. When insurance costs rise, monthly ownership costs rise. When monthly costs rise, what buyers can afford to pay for the unit itself drops.

Special Assessments for Deferred Maintenance

Buildings that skipped maintenance for decades are now paying for it all at once. Special assessments of $20,000 to $100,000+ per unit are showing up across Florida. In our analysis of 1,900+ HOA documents, special assessment language is one of the most common red flags. The buildings that deferred the most are getting hit the hardest.

Financing Is Getting Harder

Fannie Mae and Freddie Mac tightened condo financing rules in 2026. Reserve minimums are rising from 10% to 15%. Buildings with too many investor-owned units, high delinquency rates, or active litigation can be flagged as non-warrantable. Non-warrantable means no conventional mortgage. Buyers need cash or a portfolio lender at higher rates. That shrinks the buyer pool and pushes prices down further.

Mortgage rates sit near 6.4% as of March 2026. Fannie Mae projects they could drop to 5.9% by year-end, but that's not guaranteed. Higher rates compound the affordability squeeze for condo buyers already facing rising HOA fees and insurance.

The Two-Tier Market: Deals vs. Traps

Well-funded, compliant buildings hold value and attract financing. Underfunded, non-compliant buildings trade at deep discounts with major hidden risks.

Not all condo discounts are created equal. The market is splitting into two tiers, and the difference comes down to what's in the HOA documents.

Tier 1: Compliant, well-funded buildings. These buildings completed structural inspections early. Reserves are above 70% funded. Insurance is current. Maintenance is on schedule. Prices in these buildings are softer because of general market conditions, not building-specific problems. These are the real deals.

Tier 2: Non-compliant, underfunded buildings. These buildings are behind on inspections, have reserves below 30%, face pending special assessments, or have insurance issues. The deep discount isn't a deal. It's a warning. The price is low because informed buyers are walking away.

The problem is that both tiers look the same on Zillow. The listing doesn't tell you whether the building is 80% funded or 15% funded. It doesn't mention the $50,000 assessment the board discussed at last month's meeting. You have to read the documents.

How to Calculate the True Cost of a Discounted Condo

Add the purchase price, likely assessments, HOA fee trajectory, insurance increases, and any financing premium. The "true cost" is often $30-50K more than the sticker price.

A $240,000 condo is not a $240,000 purchase if the building has problems. Here's how to calculate what you're actually paying.

| Cost Component | Healthy Building | Distressed Building |

|---|---|---|

| Purchase price | $280,000 | $240,000 |

| Likely special assessment | $0 | $25,000 |

| HOA fee increase (3 years) | $1,800 | $5,400 |

| Insurance premium rise (3 years) | $600 | $2,000 |

| Financing premium (non-warrantable) | $0 | $10,000 |

| True 3-year cost | $282,400 | $282,400 |

Same true cost. Completely different risk profile. The "discount" disappears once you factor in the hidden costs that the HOA documents would have revealed.

5 Things to Check Before Buying a Discounted Condo

Check percent funded, meeting minutes for assessment discussions, insurance status, SIRS compliance (Florida), and HOA fee history over the past 3 years.

1. Reserve Study: Percent Funded

This is the single most important number. It tells you how much the building has saved compared to what it should have saved. Under 30% means the building is significantly underfunded and a special assessment is likely. Over 70% means the building is in good shape.

Fannie Mae is raising the minimum from 10% to 15% in 2026. A building below that threshold may lose conventional financing eligibility, shrinking the buyer pool when you want to sell.

Upload a reserve study here to get percent funded, deferred maintenance items, and major expenses coming in the next 5 years.

2. Board Meeting Minutes: Assessment Discussions

Special assessments don't appear overnight. They get discussed in board meetings for months before they're voted on. If the minutes mention "deferred maintenance," "engineering report," "special assessment options," or "reserve funding shortfall," an assessment may be coming.

Ask for the last 12 months of board meeting minutes. Read them. Or check our guide to red flags in meeting minutes.

3. Insurance: Coverage Status and Premium Trends

Is the building's master policy current? Has any carrier dropped the building? What's the deductible? If the building lost its primary insurer, owners may be on a last-resort policy with worse coverage and higher costs. This affects your HO-6 policy costs too.

4. SIRS Report (Florida Buildings)

If you're buying in Florida, check whether the building has completed its Structural Integrity Reserve Study (SIRS). Buildings 30 years or older must complete this by December 31, 2026. A building that hasn't started is behind. A building that completed it early is ahead of the curve. The SIRS report will reveal exactly what structural work needs funding.

5. HOA Fee History: 3-Year Trend

A single HOA fee number tells you nothing. The trend tells you everything. Ask for the fee schedule from the past three years. If fees jumped 15-20% annually, more increases are coming. If fees have been stable with gradual 3-5% increases, the building is managing costs well.

Red Flags That Turn a "Deal" Into a Disaster

Deep discounts combined with low reserves, pending litigation, SIRS non-compliance, or insurance non-renewal are warning signs, not buying opportunities.

Any one of these alone might be manageable. Two or more together means the discount is probably not enough.

- Price below market + reserves under 30%. An assessment is coming. The seller knows it. That's why they're selling.

- Long time on market + litigation in meeting minutes. Active lawsuits scare lenders and buyers. If the building is suing its developer or being sued by owners, financing becomes harder and resale value drops.

- "Motivated seller" + SIRS non-compliance. In Florida, a building that hasn't started its SIRS process is facing mandatory reserve funding and potential structural repairs. The seller may be trying to get out before the bill arrives.

- Deep discount + recent insurance non-renewal. A building that lost its insurance carrier is in trouble. Premiums will spike on any replacement policy. Some buyers won't be able to get a mortgage at all.

Green Flags: When the Discount Is Actually a Deal

Buildings with 70%+ reserves, completed inspections, recently paid assessments, and sellers relocating for personal reasons offer genuine buying opportunities.

Not every discounted condo is a trap. Some buildings are priced down purely because of market conditions. Here's what "good discount" looks like.

- Building completed SIRS or structural repairs early. The pain is behind them. Costs are known. No surprises.

- Reserve funding over 70%. The building has been saving responsibly. Special assessments are unlikely.

- Recent assessment already paid. If the building just went through a major assessment and completed repairs, you're buying after the correction, not before it.

- Seller relocating for personal reasons. Job transfer, family situation, downsizing. The building is fine. The seller just needs to move.

- Market timing only. Soft demand, high inventory, buyer leverage. No underlying building problems. These are the deals that look obvious in hindsight.

Market Outlook: When Will Condo Prices Recover?

TD Economics projects Florida's condo market could stabilize by late 2026. Miami leads recovery with luxury condos forecast positive (2-4%). Recovery depends on rates and compliance progress.

TD Economics sees "scope for Florida's condo market to begin finding firmer footing by late 2026." That depends on mortgage rates cooperating and continued migration inflows.

Miami is leading the recovery among Florida metros, with luxury condo forecasts projecting 2-4% appreciation this year. Luxury condos in Miami are outperforming. Most of the rest of the state is still correcting.

For buyers, this means the window is open but not forever. Compliant buildings with strong financials will recover first. Distressed buildings may take years to stabilize. If prices rise while HOA costs also rise, the window to buy a genuinely well-managed building at a discount narrows.

How to Check Before You Buy

Every data point in this article comes from HOA documents. Reserve studies reveal percent funded and upcoming expenses. Meeting minutes reveal assessment discussions and litigation. CC&Rs reveal rental restrictions, amendment processes, and insurance requirements.

The problem is that these documents are 200-400 pages of dense legal text. Most buyers don't read them. The ones who do often don't know what to look for.

Upload your CC&Rs or reserve study to GoverningDocs. The tool extracts the key numbers, flags red flags, and tells you what's actually in the documents. Free. No signup.

In a market where over 90% of South Florida condos are selling below asking, the question isn't whether you can find a discount. It's whether the discount is hiding something.

Frequently Asked Questions

Why are condo prices falling but house prices aren't?

Condos carry shared costs that houses don't: HOA fees, insurance on common areas, reserve fund obligations, and special assessments. All four have risen sharply since 2021, especially in Florida. These rising costs reduce what buyers can afford to pay for the unit itself, pushing condo prices down while single-family homes hold steady.

Is now a good time to buy a condo?

It depends on the building. Well-funded buildings with reserves above 70%, completed inspections, and stable insurance are genuinely discounted right now. Underfunded buildings with assessments looming are cheap for a reason. The key is checking the HOA documents before making an offer.

How do I know if a condo discount is a real deal or a trap?

Check the reserve study (percent funded), meeting minutes (assessment discussions), insurance status, and SIRS compliance (Florida). If the building is well-funded and the discount is due to market conditions, it's a deal. If the building is underfunded and the seller is motivated, the discount may not cover the costs coming your way.

Will condo prices recover in 2026?

TD Economics projects Florida's condo market could begin stabilizing by late 2026. Miami leads recovery with luxury condos forecast at 2-4% appreciation. But recovery will be uneven. Compliant, well-managed buildings will recover first. Buildings with deferred maintenance and low reserves may take years.

Check the HOA Documents Before You Buy That "Deal"

Upload CC&Rs or a reserve study for free analysis. See percent funded, special assessment risk, rental restrictions, and other red flags in minutes. No signup required. Based on our analysis of 1,900+ HOA documents.

Related Articles

Sources & References

- Redfin: Condo Prices Drop the Most in Over a Decade (May 2025)

- Florida Realtors: 2025 Housing Market Year-End Report

- TD Economics: Peeling Back the Layers to the Florida Condo Market Weakness

- Redfin: 68% of Condos Now Sell Below List Price (2025)

- Insurify: Florida 2026 Home Insurance Report

- Fannie Mae: Mortgage Rate Forecast (2026)

Disclaimer: This article is for educational purposes only and does not constitute financial or real estate advice. Market data is sourced from public reports and may have changed since publication. Specific metro statistics reflect data available at time of writing. Consult a qualified real estate professional for guidance specific to your market and situation.