In This Guide

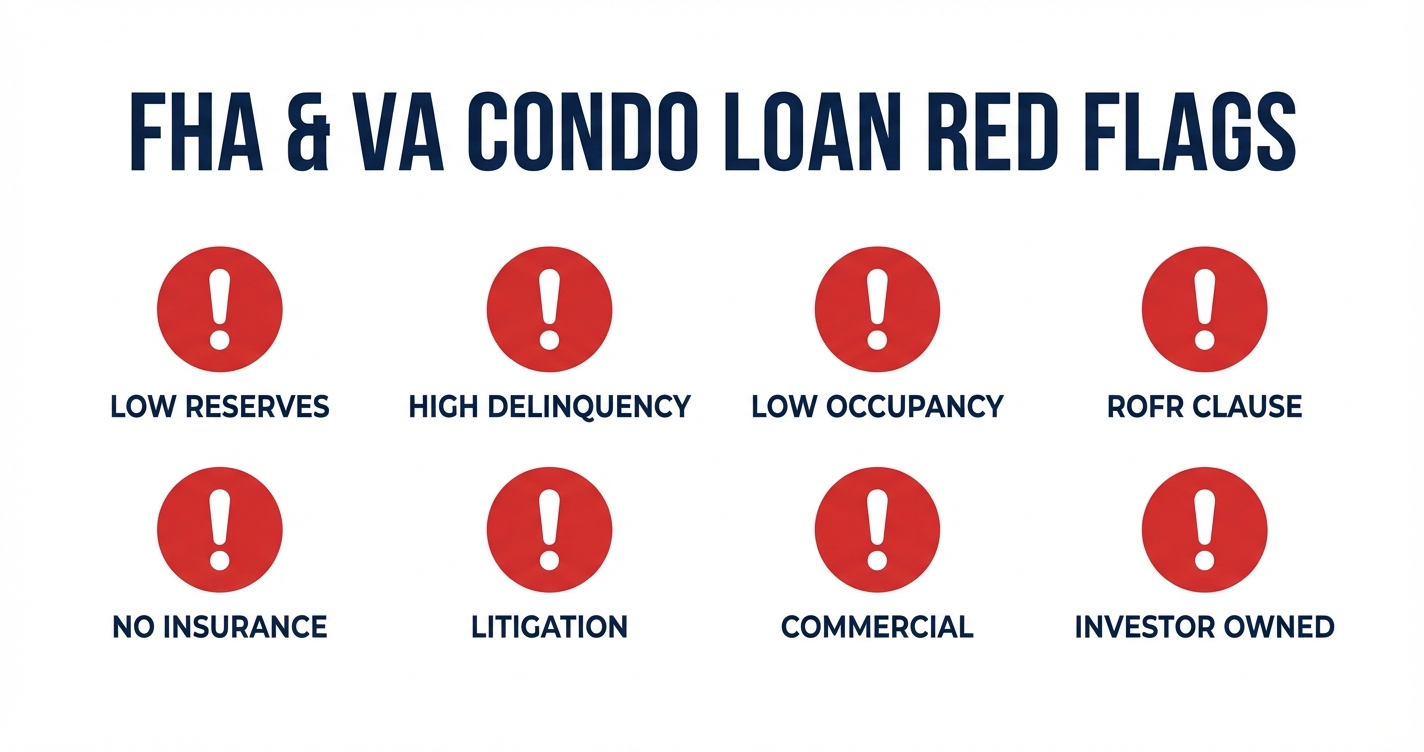

As of 2019, only 6.5% of US condos had full FHA project approval. Eight specific HOA document red flags cause most government loan denials: low reserves, high delinquency, low owner-occupancy, right of first refusal clauses, insurance gaps, active litigation, excessive commercial space, and single-entity ownership concentration.

Your buyer found the perfect condo. They're pre-approved for an FHA or VA loan. The offer gets accepted. Then the lender pulls the HOA documents and everything falls apart.

The building isn't approved. The reserves are too low. The delinquency rate is too high. The CC&Rs have a right of first refusal clause that automatically disqualifies VA financing. Three weeks of due diligence, gone. Your buyer either walks away or scrambles for a portfolio loan at 20% down.

This happens constantly. According to HUD, only about 6,591 condo projects out of more than 150,000 nationwide had active FHA approval as of 2019. That meant roughly 93.5% of US condos lacked FHA project approval at that time (Single Unit Approval, introduced the same year, has since expanded access for individual units). The problem isn't just paperwork. It's what the documents reveal about the building's financial health, governance, and legal structure. Here are the eight red flags that kill deals before closing.

Why Most Condos Can't Get FHA or VA Loans

Most condo associations never apply for government loan approval, and those that do often fail the financial requirements.

FHA and VA loans aren't just about the borrower. The building itself must meet a separate set of requirements. FHA requires either full project approval or individual Single Unit Approval (SUA). VA requires full project approval with no single-unit alternative.

FHA condo lending dropped from 8.4% of all FHA loans in 2001 to just 2.1% by 2018, according to HUD Cityscape research. Even after HUD restored single-unit approvals in October 2019 to expand access, the vast majority of condo buildings remain outside the system.

The reasons stack up. Many HOA boards never bother applying. FHA approval lasts only three years and requires recertification. Some buildings simply can't pass the financial thresholds. And VA approval, while it lasts a lifetime once granted, has even stricter requirements around lease restrictions and lien priority that most condo CC&Rs violate.

For agents, this creates a recurring problem. Your buyer qualifies for the loan. The building does not. Understanding which HOA financial health indicators to check before writing an offer saves weeks of wasted effort.

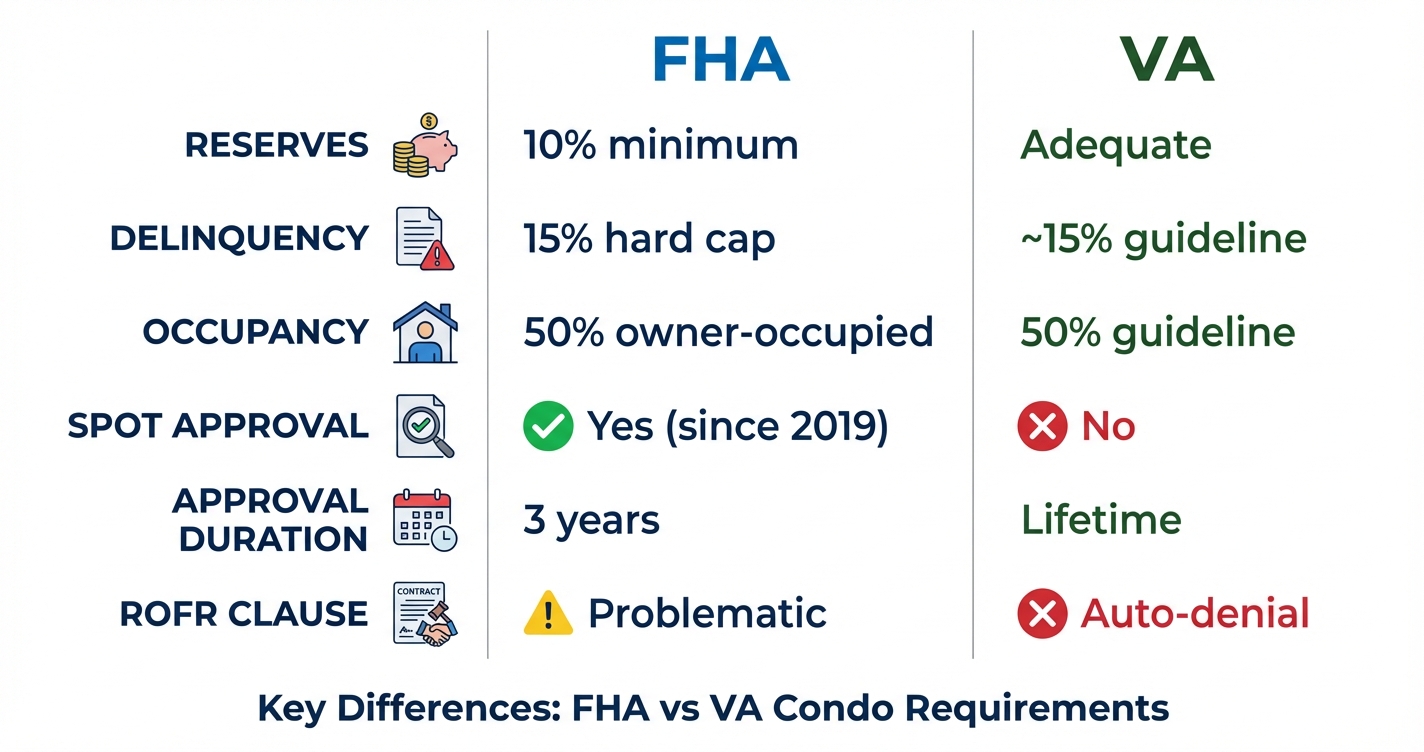

FHA vs VA: What Each Program Requires

FHA and VA overlap on reserves and delinquency but diverge sharply on spot approvals, lease restrictions, and lien priority.

Both programs evaluate the same HOA documents, but they weigh different factors. Here's a side-by-side comparison based on HUD 4000.1 (FHA) and 38 CFR 36.4362 (VA):

| Requirement | FHA | VA |

|---|---|---|

| Owner-occupancy | 50% minimum (can reduce to 35% if project is 12+ months old and <10% delinquent) | ~50% (guideline, VA has discretion) |

| Delinquency rate | 15% hard cap (60+ days past due) | ~15% commonly triggers denial |

| Reserve funding | 10% of annual budget minimum | "Adequate" (no specific %) |

| Commercial space | 35% max of total floor area (exceptions to 49%) | Must be "primarily residential"; lenders commonly apply 25% overlay |

| Single-entity ownership | 10% max (projects with 20+ units) | 10% max |

| Right of first refusal | Problematic, not always fatal | Almost always automatic denial |

| Super-lien clauses | Problematic | Deal killer (lien must be subordinate) |

| Rental restrictions | Must allow leasing | Stricter: no seasoning, no board screening |

| Approval duration | 3 years (must recertify) | Lifetime (unless revoked) |

| Spot/single-unit approval | Yes (since October 2019) | No. Entire project must be approved. |

| Insurance concentration | Max 50% of units with FHA mortgages (full approval); 10% for SUA | N/A |

The biggest difference: FHA offers a Single Unit Approval (SUA) path that lets individual units qualify even if the full project isn't approved. VA has no equivalent. If the building isn't on the VA approved condo list, the veteran cannot use their VA loan. Period.

The 8 HOA Document Red Flags That Kill Government Loans

Eight issues in CC&Rs, reserve studies, budgets, and insurance declarations can each independently block FHA or VA approval.

1. Reserve Funding Below 10%

The requirement: FHA mandates that at least 10% of total annual budgeted assessment income goes to the reserve fund. VA requires "adequate" reserves without specifying a number, but lenders interpreting VA guidelines commonly use a similar threshold.

Where to find it: The annual operating budget shows the reserve allocation as a line item. The reserve study shows the percent funded level. Both matter. A building could contribute 10% of its budget but still be critically underfunded if it deferred contributions for years.

What happens if it fails: FHA project approval and SUA both require 10% minimum. No exceptions. Fannie Mae and Freddie Mac are raising their threshold to 15% on January 4, 2027, which means buildings barely clearing 10% today will soon fail conventional lending standards too.

Champlain Towers South in Surfside, Florida was 6.9% funded at the time of its collapse. That building would have failed every government lending standard in place. Buildings with artificially low HOA fees are the most likely to fall short on reserves.

2. Delinquency Rate Above 15%

The requirement: HUD 4000.1 sets a hard cap: no more than 15% of units can be 60+ days delinquent on assessments. For VA, 15% is not a bright-line regulatory rule, but lenders commonly treat it as the threshold that triggers denial.

Where to find it: The HOA's financial statements or the lender questionnaire (HUD Form 9991 for FHA, Fannie Mae Form 1076 for conventional). Some associations bury this number. If the board won't provide an aging report of receivables, that's a red flag in itself.

What happens if it fails: Automatic denial for FHA project approval and SUA. Our analysis found 1,438 Florida buildings crossed the 15% delinquency threshold in 2024. High delinquency signals that the association can't collect enough revenue to maintain the building, which cascades into deferred maintenance, insurance lapses, and further decline.

3. Owner-Occupancy Below 50%

The requirement: FHA requires at least 50% of units to be owner-occupied (with a possible reduction to 35% if the project is 12+ months old, less than 10% of units are in arrears, and reserves are funded at 20% of the budget). VA uses a similar ~50% guideline, though it has more discretion.

Where to find it: The lender questionnaire asks directly. You can also cross-reference property records with the unit registry. Buildings in vacation markets, resort areas, and investor-heavy neighborhoods are the most likely to fail.

What happens if it fails: FHA denies project approval. SUA also requires 50% (or 35% with the same qualifying conditions). This is one of the most common failures in markets like South Florida, Las Vegas, and resort areas where rental and investment units dominate the building. A building with 60% investor-owned units is effectively locked out of government financing.

4. Right of First Refusal Clauses

The requirement: 38 CFR 36.4362 states that VA-financed units "shall not be subject to any right of first refusal." This is the single most common reason for VA condo denial.

Where to find it: The CC&Rs. Look for language giving the HOA board the right to match any purchase offer, approve buyers, or block sales. This clause exists in the governing documents of a large share of US condo associations. It applies to documents recorded after December 1, 1976.

What happens if it fails: VA approval denied. No workaround unless the HOA amends its CC&Rs to remove the clause, which typically requires a 67-75% supermajority vote. FHA is more lenient on right of first refusal but may still flag it during review.

Get Your CC&Rs Analyzed

Upload your HOA's CC&Rs and get instant analysis of rental restrictions, pet policies, financing red flags, and more. Free. No signup required.

5. Insufficient Insurance Coverage

The requirement: FHA requires a master hazard insurance policy covering 100% of replacement cost, general liability of at least $1 million per occurrence, and a fidelity bond equal to three months of aggregate assessments plus reserves for projects with 20+ units. VA also requires fidelity bond coverage for projects with 20+ units, though the VA does not specify the same formula in federal regulations.

Where to find it: Insurance declarations pages, which are separate from the CC&Rs. Request the current certificate of insurance, not last year's. Also check the budget for the insurance line item. If insurance costs dropped significantly, the board may have reduced coverage to save money.

What happens if it fails: Any insurance gap blocks approval. Flood insurance is also required if the building is in a FEMA flood zone. After the Surfside collapse, many Florida condo insurance premiums doubled or tripled. Some associations responded by cutting coverage below required thresholds rather than passing the costs to owners.

6. Active Litigation

The requirement: Both FHA and VA require disclosure of pending litigation. FHA evaluates whether the lawsuit threatens the project's financial stability, physical condition, or safety. Construction defect suits, personal injury claims, and disputes that could result in judgments exceeding insurance coverage are all red flags.

Where to find it: The lender questionnaire includes a litigation disclosure section. Board meeting minutes also reference ongoing legal matters. Check for legal expense line items in the budget that seem disproportionate to the building's size.

What happens if it fails: FHA and VA underwriters evaluate litigation on a case-by-case basis. A slip-and-fall claim within insurance limits probably won't block approval. A $10 million construction defect lawsuit on a 50-unit building will. The concern is that a large judgment could deplete reserves or trigger a massive special assessment.

7. Too Much Commercial Space

The requirement: FHA allows up to 35% of total floor area for commercial use (with exceptions to 49% in certain cases). VA requires the project to be "primarily residential" but does not specify an exact percentage. Most VA lenders apply a 25% maximum as an overlay.

Where to find it: The CC&Rs define the project's unit breakdown and permitted uses. The site plan or condo plat map shows floor area allocation. Mixed-use buildings with ground-floor retail, restaurants, or office space are the ones to watch.

What happens if it fails: A building with 30% commercial space passes FHA but may fail VA lender guidelines. A building at 40% fails FHA (without exception) and almost certainly fails VA. This is particularly common in urban mixed-use developments where developers dedicate multiple floors to retail or office tenants. The commercial income may benefit the HOA budget, but it disqualifies the building from government financing.

8. Single-Entity Ownership Above 10%

The requirement: Both FHA and VA prohibit any single entity from owning more than 10% of the total units (FHA applies this to projects with 20+ units). This includes the developer, an investor, a corporation, or any related entities.

Where to find it: The lender questionnaire and the HOA's unit registry. In newer buildings where the developer hasn't sold out, this is especially common. An 80-unit building where the developer still holds 12 unsold units (15%) fails both FHA and VA.

What happens if it fails: Denial until ownership concentration drops below 10%. In practice, this means waiting for the developer to sell more units. For condo financing purposes, this is a timing issue that resolves as the building sells out, but it can block deals for months or years in slow markets.

VA-Specific Deal Killers Most Agents Miss

VA has four unique deal killers most agents miss: ROFR ban, lien subordination, lease restriction limits, and no spot approval.

VA loans carry specific requirements that trip up even experienced agents. These four issues are unique to VA and cause the most denials:

Right of First Refusal (ROFR) Ban

Under 38 CFR 36.4362, a VA-financed condo "shall not be subject to any right of first refusal." This applies to all CC&Rs recorded after December 1, 1976. Most US condo associations include some form of ROFR in their governing documents. It's the most common reason condos fail VA approval, and many boards don't even realize it's a problem.

Super-Lien Prohibition

The VA mortgage must hold first lien position. Any HOA super-lien clause that gives assessment liens priority over the mortgage is a deal killer. Several states, including Florida, Colorado, and Nevada, grant HOAs a statutory super-lien that takes priority for a certain number of months of unpaid assessments. Buildings in these states face an uphill battle for VA approval even if the CC&Rs don't explicitly create a super-lien.

Lease Restriction Limits

VA requires the HOA to allow owners to lease their units. No "seasoning clauses" requiring the owner to live in the unit for one or two years before renting. No board approval of tenants. No board screening of lessees. This matters for military families who face PCS (Permanent Change of Station) orders and may need to rent their unit on short notice. A building that bans rentals or requires board approval of tenants will not get VA approval.

No Spot Approval Fallback

FHA restored Single Unit Approval (SUA) in October 2019, giving buyers a path even when the full project isn't approved. VA has no equivalent. If the building is not on the VA approved condo list, the veteran cannot use VA financing. There is no individual unit exception. This makes VA approval an all-or-nothing proposition. You can check the VA's lookup tool before writing an offer to avoid wasting time.

What You Can Do If the Building Fails

FHA Single Unit Approval, portfolio loans, CC&R amendments, and VA waivers are options, but each has cost-time-success tradeoffs.

A failed building doesn't always mean a dead deal. Here are the workarounds, ranked by practicality:

| Workaround | How It Works | Tradeoff |

|---|---|---|

| FHA Single Unit Approval | Lender submits HUD Form 9991 for the individual unit | Core requirements still apply (50% occupancy, or 35% with qualifying conditions, 10% reserves, no major litigation). FHA concentration limited to 10% of units (or max 2 for <10-unit projects). |

| Portfolio loan | Lender keeps the loan on its books instead of selling to GSEs | 20-25% down payment required. Higher interest rates. |

| HOA applies for approval | Board proactively files for FHA (3-year) or VA (lifetime) approval | Requires board cooperation. Many boards don't bother. Takes weeks to months. |

| CC&R amendment | Remove the blocking clause (ROFR, rental ban, super-lien) | Requires 67-75% supermajority vote. Months of effort. Politically difficult. |

| VA waiver request | Request exception for ROFR or lease restriction issues | Not guaranteed. Limited documentation on success rates. |

| Non-QM lender | Specialty lender outside qualified mortgage rules | 20-25% down. Rates 2-4% higher than conventional. Last resort. |

The most practical path for FHA buyers is Single Unit Approval. It bypasses the need for full project approval, but the core financial requirements (reserves, delinquency, occupancy) still apply. If the building fails on those fundamentals, SUA won't help.

For VA buyers, the options narrow significantly. There is no spot approval. If the building is not VA-approved and the HOA won't apply or amend its documents, the only paths forward are portfolio loans or Non-QM lenders. Both require substantially more money down and higher rates, which defeats the purpose of using a VA loan.

The best approach is catching these issues before writing an offer. Check the VA condo lookup tool for VA loans. For FHA, request the HOA's financials and CC&Rs early and review them for the eight red flags above. You can upload documents to GoverningDocs' free CC&R analysis tool to flag issues automatically before your buyer gets invested.

Frequently Asked Questions

Can I get an FHA loan on a condo that isn't FHA-approved?

Yes, through Single Unit Approval (SUA). Since October 2019, lenders can submit HUD Form 9991 to approve individual units even when the full project lacks FHA approval. However, the building must still meet core requirements: 50% owner-occupancy (or 35% with qualifying conditions), 10% reserve funding, below 15% delinquency, and no disqualifying litigation. FHA concentration is limited to 10% of units (or max 2 units in projects with fewer than 10 units) under SUA.

How do I check if a condo is VA-approved?

Use the VA Condo Lookup Tool at lgy.va.gov. Search by state, city, or project name. If the building does not appear, it is not VA-approved and the buyer cannot use a VA loan. Unlike FHA, VA has no single-unit approval option.

What is a right of first refusal, and why does it kill VA loans?

A right of first refusal (ROFR) gives the HOA board the right to match any purchase offer or approve buyers before a sale closes. Under 38 CFR 36.4362, VA-financed condos "shall not be subject to any right of first refusal." This clause exists in a large share of US condo CC&Rs and is the single most common reason for VA condo denial. Removing it requires a supermajority CC&R amendment.

What is the FHA reserve requirement for condos?

FHA requires at least 10% of total annual budgeted assessment income to be allocated toward reserves per HUD 4000.1. This applies to both full project approval and Single Unit Approval. Note that Fannie Mae and Freddie Mac are raising their conventional loan threshold to 15% effective January 4, 2027.

Can the HOA block a veteran from buying a condo?

Indirectly, yes. If the HOA board refuses to apply for VA approval or won't amend CC&Rs that contain disqualifying clauses like ROFR or rental bans, the building remains ineligible for VA financing. The veteran can still purchase with a conventional or portfolio loan, but loses VA benefits including the zero-down-payment advantage.

How long does FHA condo approval last?

FHA project approval is valid for three years. The HOA must recertify before the approval expires. If it lapses, new FHA buyers cannot close until the recertification is complete. VA approval, by contrast, lasts a lifetime and does not require renewal unless revoked.

Check your building before writing an offer

Upload CC&Rs or reserve studies and get an instant analysis of FHA/VA red flags. Built on insights from 1,900+ HOA documents analyzed.

Related Articles

- HOA Financial Health Guide: The Complete Assessment

- Condo Financing and HOA Documents: What Lenders Check

- Non-Warrantable Condo: What It Means for Buyers

- HOA Delinquency Rate: The Number That Can Kill Your Condo Purchase

- Fannie Mae and Freddie Mac Condo Rules: What Changed in 2026

- Are Low HOA Fees a Red Flag?

Sources & References

- HUD 4000.1 (FHA Single Family Housing Policy Handbook) (FHA condo approval requirements, reserve minimums, delinquency thresholds)

- 38 CFR 36.4362 (VA Condo Regulations) (VA lien subordination, ROFR prohibition, condo project requirements)

- Fannie Mae Selling Guide B4-2.1-03 (conventional condo project standards, reserve requirements)

- VA Condo Lookup Tool (lgy.va.gov) (search VA-approved condo projects)

- HUD Press Release PR19-121 (6,591 FHA-approved condos out of 150,000+ nationwide)

- NAR FHA Condo Rule Assessment (National Association of Realtors analysis of FHA condo approval impact)

- HUD Cityscape Vol. 22 No. 1 (FHA condo lending declined from 8.4% to 2.1% of FHA loans, 2001-2018)

- CAI Advocacy Blog (Fannie/Freddie reserve requirement increase to 15%, effective Jan 4, 2027)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. FHA and VA condo approval requirements are subject to change. Consult a qualified mortgage lender or real estate attorney for guidance specific to your situation. GoverningDocs is not affiliated with HUD, the VA, Fannie Mae, or Freddie Mac.