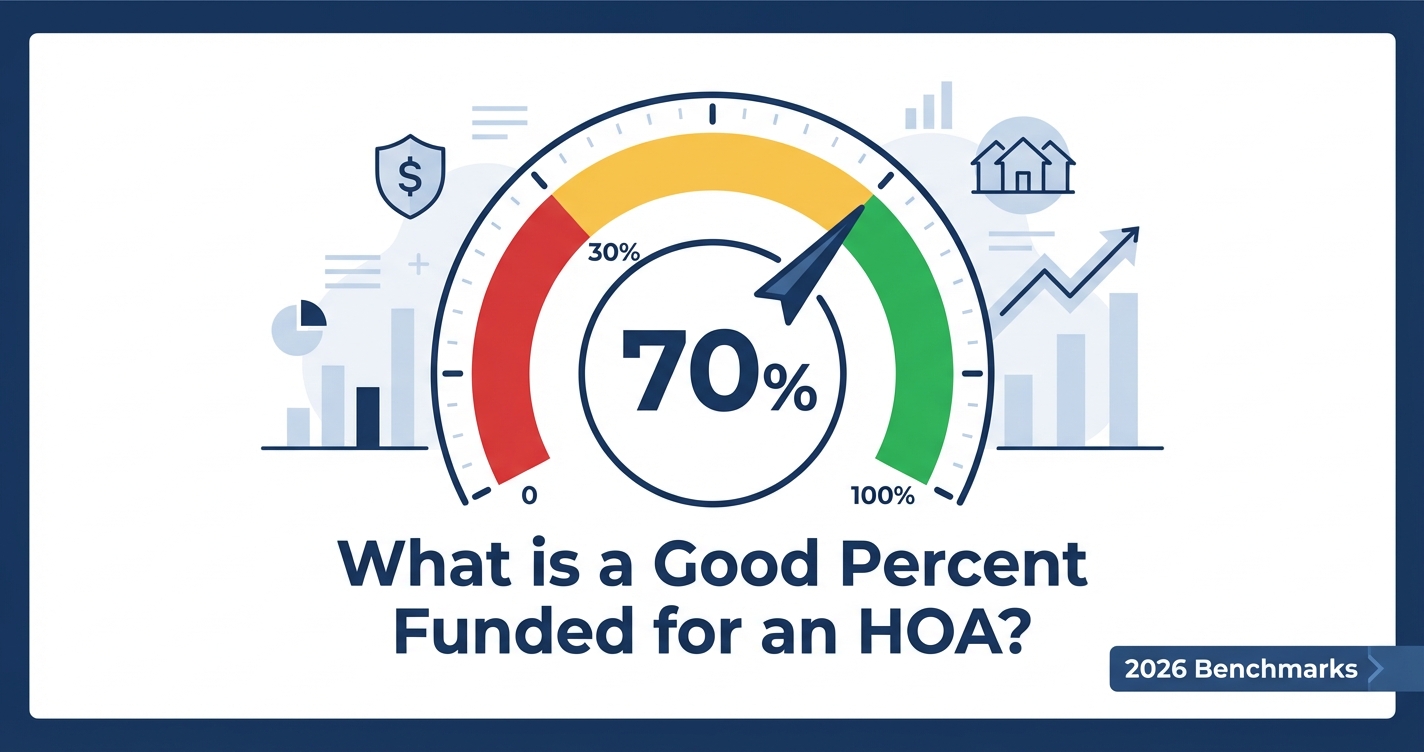

A good percent funded for an HOA is 70% or higher. Below 30% is a red flag signaling high special assessment risk. Between 30-70% requires careful review of upcoming expenses.

You found a condo you love. The listing looks great, the HOA dues seem reasonable. Then you open the reserve study and see a number you've never encountered before: percent funded.

This single number is one of the most useful indicators of financial risk you'll find in the HOA disclosure package. Here's how to read it.

What Does Percent Funded Mean?

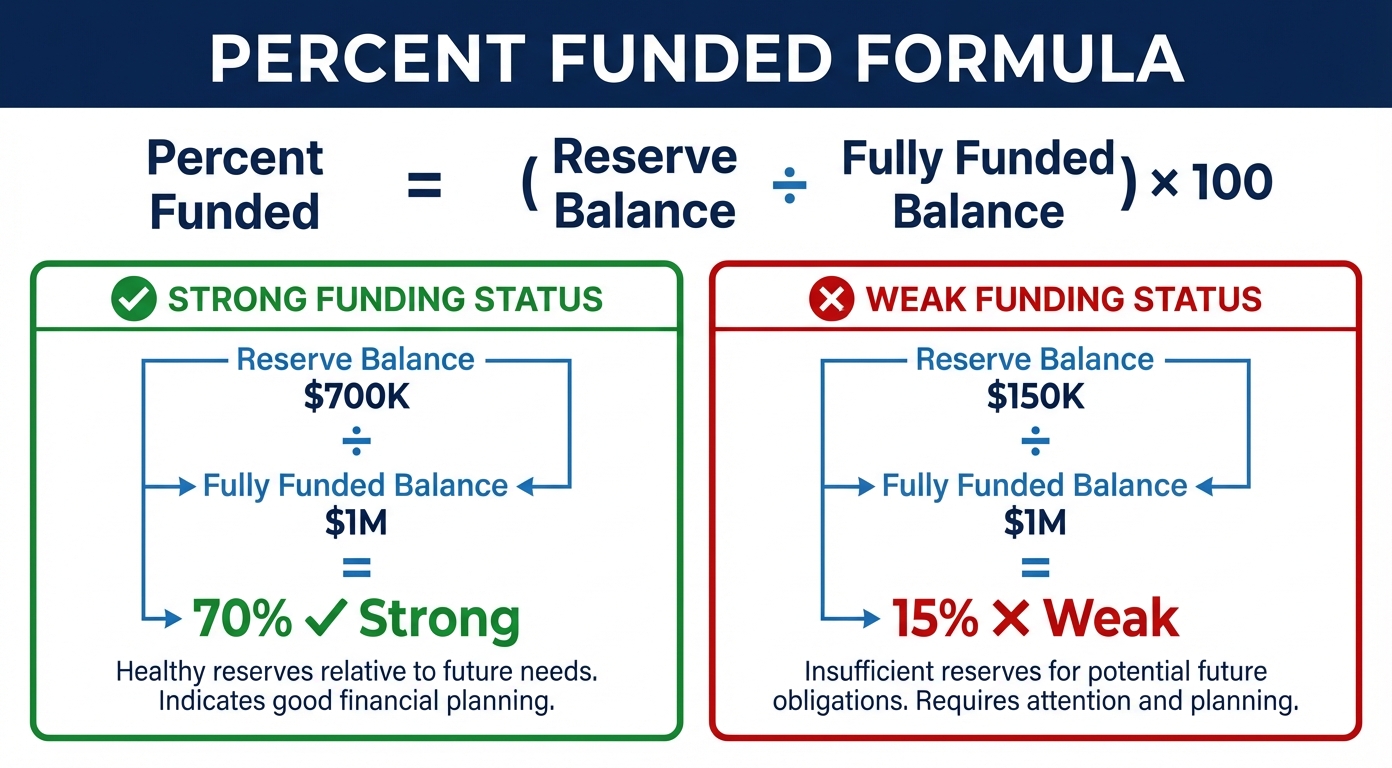

Percent funded compares an HOA's actual reserve balance to what it should have based on the age and condition of building components, expressed as a percentage.

Think of it like a retirement savings target. If you should have $100,000 saved by age 40 but only have $40,000, you're 40% funded. Same concept applies to HOA reserves.

The formula: Percent Funded = (Actual Reserve Balance ÷ Fully Funded Balance) × 100

The "fully funded balance" is what the reserve study calculates the HOA should have set aside by now, based on the age of every component (roofs, elevators, parking lots, plumbing) and their expected replacement costs.

A 200-unit building with a $2M reserve balance sounds impressive. But if the fully funded balance is $5M, that building is only 40% funded. The raw dollar amount means nothing without context.

2026 Industry Benchmarks

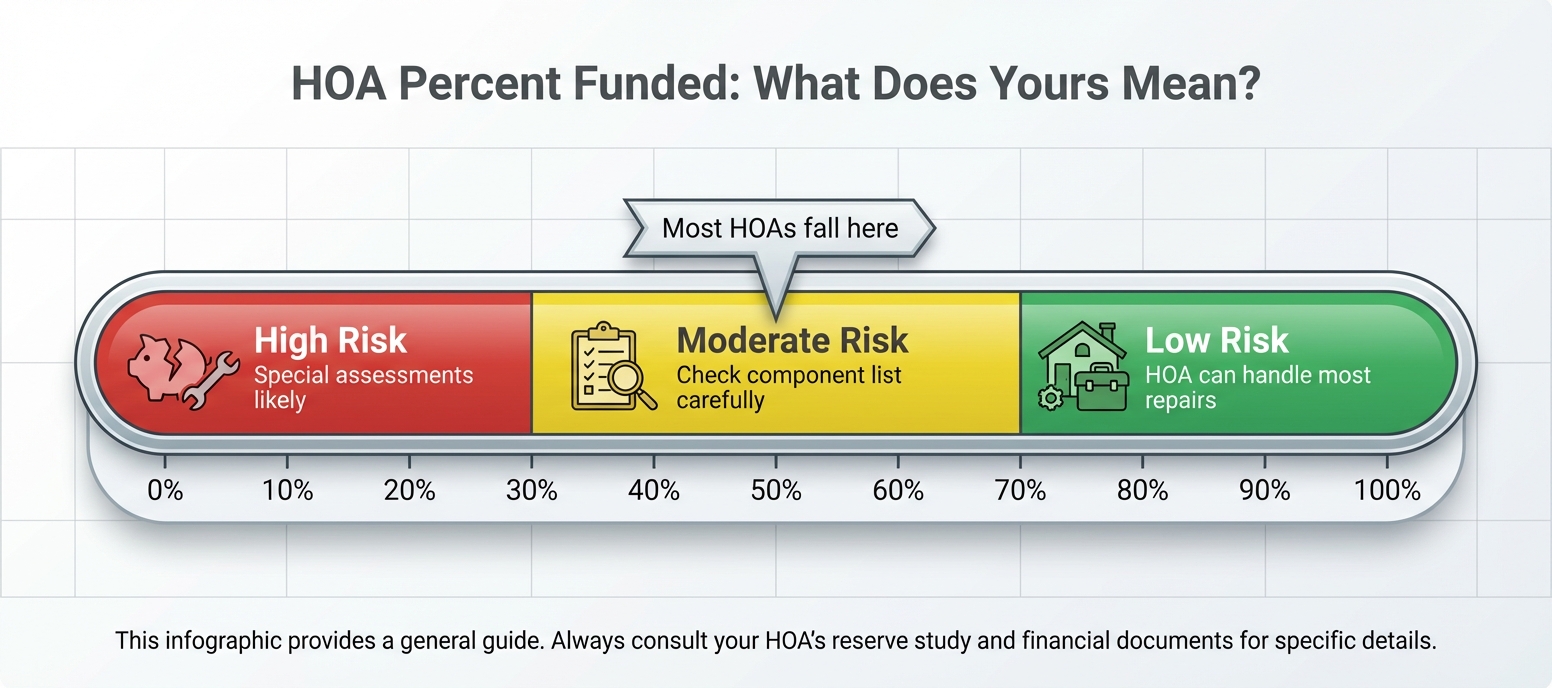

The Community Associations Institute (CAI) considers 70%+ adequately funded. Industry estimates suggest roughly half of HOAs fall below that threshold.

| Percent Funded | Rating | What It Means for You |

|---|---|---|

| 70–100% | Strong | Low special assessment risk. HOA can handle most repairs from reserves. |

| 30–70% | Fair | Moderate risk. Check the component list for near-term expenses before buying. |

| Below 30% | Weak | High risk. Special assessments likely for any major repair. Investigate carefully. |

For context on what else to look for beyond percent funded, see our guide to 5 HOA red flags from 1,900+ documents.

Why 70% Is the Target (Not 100%)

100% funding isn't always optimal because it can mean HOA dues are unnecessarily high. The 70% threshold balances adequate reserves with reasonable monthly costs.

Reserve study professionals consider 70% the practical target because:

- Adequate cushion: Covers most anticipated expenses without special assessments

- Flexibility: Absorbs unexpected costs without crisis

- Reasonable dues: Doesn't over-burden owners with excessive monthly fees

- Lender confidence: Generally viewed favorably by lenders evaluating condo project eligibility (though lenders use their own criteria — see below)

A building at 100% funded isn't necessarily better managed. It could mean dues are higher than they need to be, or the reserve study underestimated future costs.

Context Matters: When the Number Alone Isn't Enough

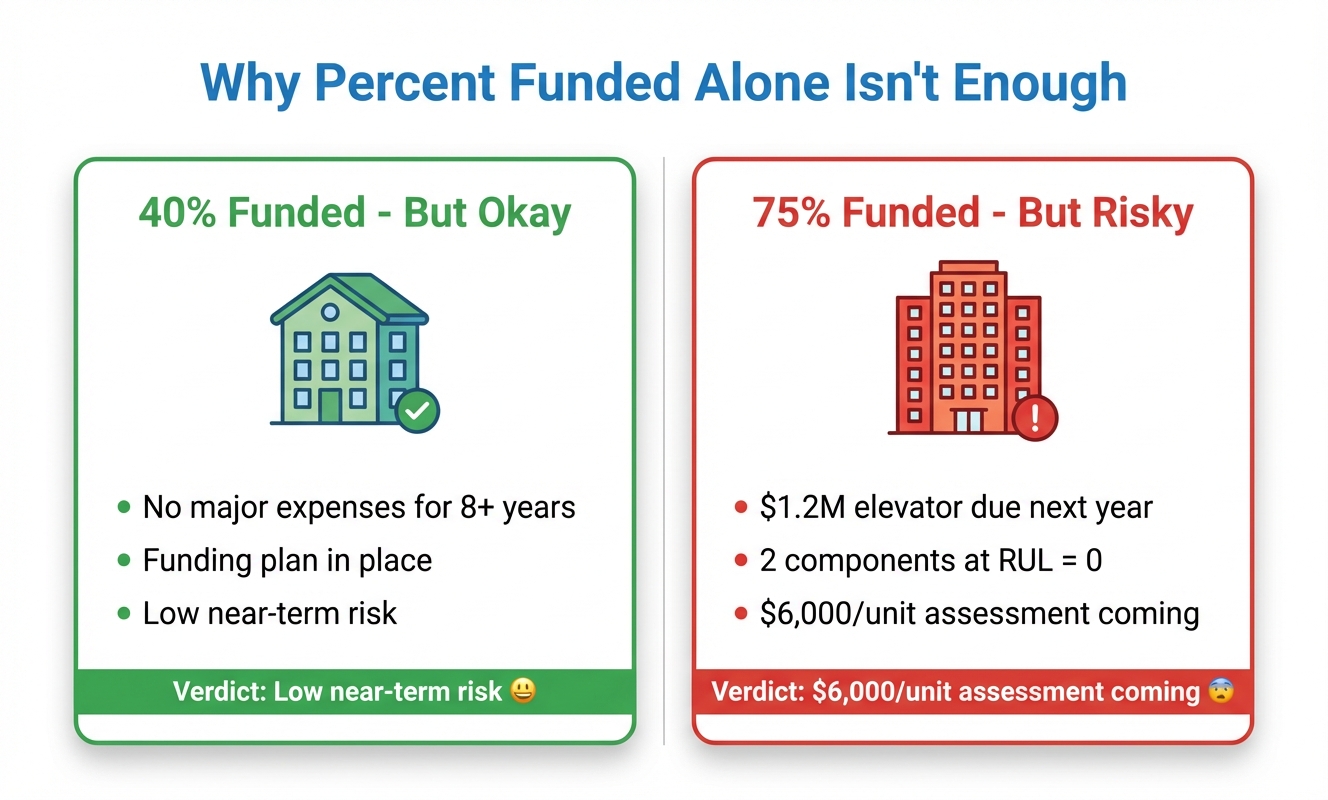

A small 10-unit HOA at 40% funded may only need modest contribution increases, while a large complex at 80% could still face assessments if major expenses are imminent.

Consider these two scenarios:

Scenario A: 40% Funded, But Probably Fine

A 10-unit townhouse complex. No major expenses due for 8+ years. The board is gradually increasing contributions to reach 70% before the roof replacement in 2034. The reserve study shows a clear funding plan.

Scenario B: 75% Funded, But Risky

A 200-unit high-rise at 75% funded. Looks healthy on paper. But elevator modernization ($1.2M) is due next year, and two HVAC units have RUL = 0. A $6,000/unit assessment may be coming despite the "good" funding level.

The takeaway: Always check the reserve study's component list for items with RUL (Remaining Useful Life) = 0 or due within 2 years. These override the overall percent funded number. Our guide to reading a reserve study walks through exactly how to find them.

How to Find Percent Funded in Your Reserve Study

Look for the executive summary or financial analysis section. The percent funded figure is usually on the first 2-3 pages, often in a table labeled "reserve fund status."

Reserve studies vary in format, but the percent funded number is almost always in the executive summary. Here's where to look:

- Executive summary page: Usually labeled "Percent Funded," "Funding Level," or "Reserve Fund Status"

- Financial analysis table: Shows current balance vs. fully funded balance, with the percentage calculated

- 30-year projection chart: Some studies graph percent funded over time, showing whether it improves or declines

Pro Tip

If you can't find the percent funded number, the study may only list "current reserve balance" and "fully funded balance." Divide the first by the second and multiply by 100. That's your percent funded.

Some HOA disclosure packages don't include a reserve study at all. That's a major red flag. If the seller or management company can't produce one, proceed with caution.

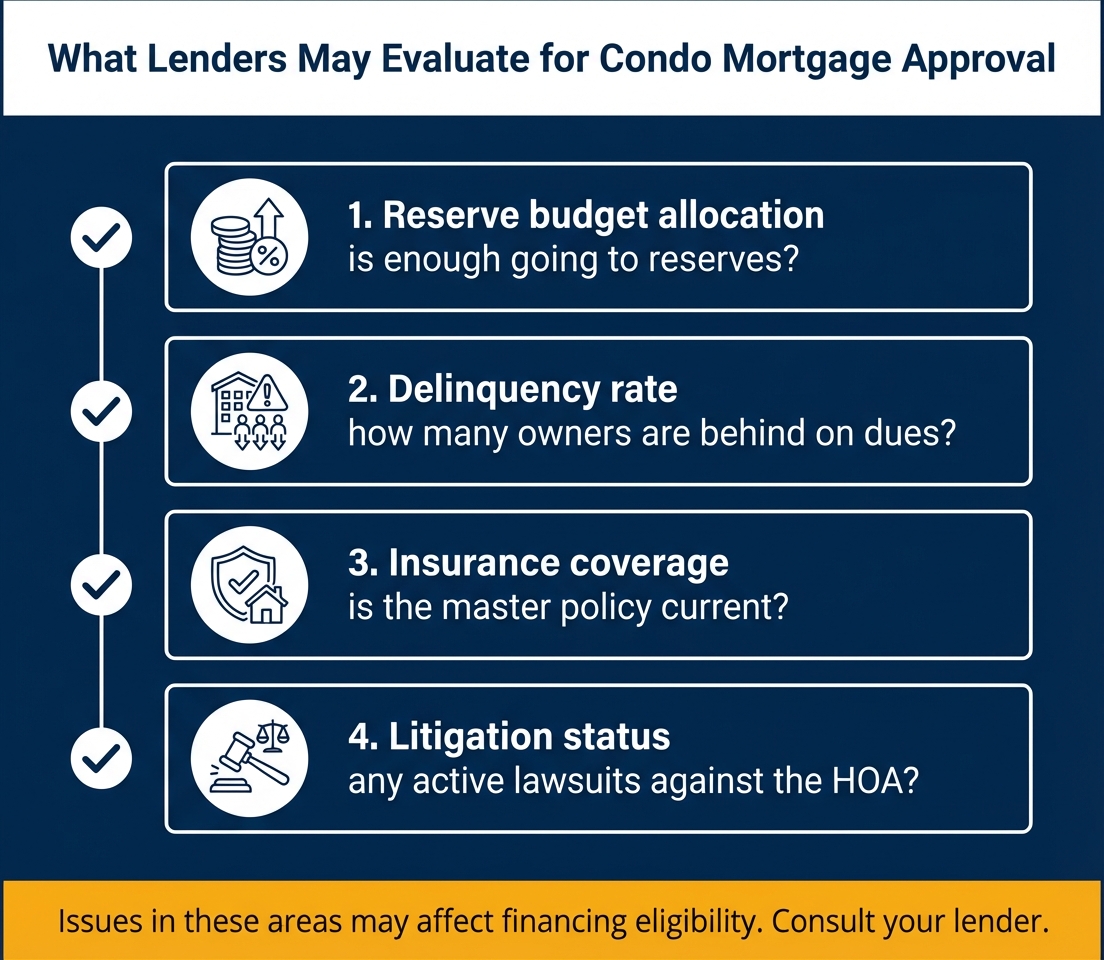

What Lenders Look For (And Why It Affects Your Mortgage)

Lenders evaluate HOA finances using their own criteria, including budget allocation to reserves. Low reserve funding can make a building non-warrantable, limiting buyers to cash or portfolio loans.

Percent funded doesn't just affect your risk of a special assessment. It can influence whether you can get a mortgage at all.

Important distinction: Percent funded and lender reserve requirements are related but different metrics. Percent funded measures how much the HOA has saved relative to what it should have. Lenders like Fannie Mae look at a separate number: what percentage of the HOA's annual operating budget is allocated to reserves (typically requiring at least 10%).

A building can be 70% funded but still fail lender criteria if its annual budget doesn't allocate enough to reserves. Buildings that fail these financial checks, or that have other issues like high delinquency rates, can be classified as non-warrantable.

Non-warrantable means:

- No conventional mortgage financing (Fannie Mae/Freddie Mac won't back the loan)

- Buyer pool shrinks to cash buyers and portfolio lenders

- Sale prices drop because fewer people can buy

If you're buying with a conventional loan, your lender will check the HOA's financials. A low percent funded number can delay or kill your deal. For more on how this works, see our post on understanding HOA special assessments.

How Florida's SB 4D Changed the Game

Post-Surfside legislation bans reserve waivers in Florida, forcing many associations from 20-30% funded to comply with full funding requirements. Assessments of $40,000-$100,000+ have been widely reported.

Before 2022, Florida HOAs could legally "waive" reserve contributions. Many condos operated at 10-30% funded for decades. The Surfside tragedy changed everything:

- SB 4-D (2022): Mandated structural inspections and reserve studies (SIRS)

- Jan 1, 2026: Reserve waivers officially banned

- Result: Thousands of Florida condos now facing massive catch-up assessments to bring funding levels into compliance

Florida Buyer Alert

If you're buying a Florida condo, don't just look at percent funded. Ask specifically about SIRS compliance, any pending assessments, and the HOA's plan to meet new reserve requirements. A building at 60% funded today could still have a $50,000 assessment on the horizon.

Key Takeaways

- ✓70%+ funded = Strong financial health, low assessment risk

- ⚠30-70% funded = Check the component list for near-term expenses before buying

- ✕Below 30% = High risk. Special assessments are likely for major repairs.

- →Always check RUL = 0 items in the component list. They override the percent funded number.

- →Low funding can affect your mortgage. Lenders evaluate HOA financials as part of conventional loan approval.

Frequently Asked Questions

What percent funded is too low for an HOA?

Below 30% is widely considered too low by industry professionals. At that level, the HOA may not be able to cover major repairs without a special assessment. Separately, lenders evaluate whether enough of the HOA's annual budget is allocated to reserves, which can affect mortgage eligibility. See all five HOA red flags to check →

Can an HOA be over 100% funded?

Yes. It means the HOA has more in reserves than the current calculated need. This can happen after a large special assessment or if the reserve study's cost estimates are conservative. It's not a problem, but it may mean owners are paying higher dues than strictly necessary.

How often should percent funded be recalculated?

The industry standard is a full reserve study update every 3-5 years, though some states require more frequent updates. Florida now mandates SIRS (structural reserve studies) in addition to traditional reserve studies. Between full updates, the percent funded number shifts as the HOA collects contributions and spends on repairs. How Florida's new reserve laws affect buyers →

Is percent funded the same as the reserve study funding plan?

No. Percent funded is a snapshot of where the HOA stands right now. The funding plan is the strategy for how it gets to where it needs to be. A building at 40% funded with an aggressive funding plan is meaningfully different from one at 40% with no plan at all. How to read a reserve study in 5 minutes →

Where can I find the percent funded for my HOA?

It's in the reserve study, usually in the executive summary or financial analysis section. If you're buying, it should be included in the HOA disclosure package. If you're an owner, you can request it from your management company or board. You can also upload your reserve study to GoverningDocs for a free analysis that extracts this number automatically.

Get Your Reserve Study Analyzed in Minutes

Upload your HOA's reserve study and get instant insights on percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Analyze Reserve Study →Related Articles

Sources & References

- National Reserve Study Standards — Percent Funded — Association Reserves (percent funded methodology and benchmarks)

- 2023 Homeowner Satisfaction Survey & Statistical Study — Foundation for Community Association Research / CAI (reserve funding statistics)

- Condominium Project Eligibility — Fannie Mae (reserve budget requirements and warrantability guidelines)

- Florida Condo Crisis 2026: What Buyers Must Know — GoverningDocs (SB 4-D, SIRS requirements, and reserve waiver ban)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. HOA documents and reserve funding requirements vary significantly by state and association. Consult a qualified professional for guidance specific to your situation.