In This Guide

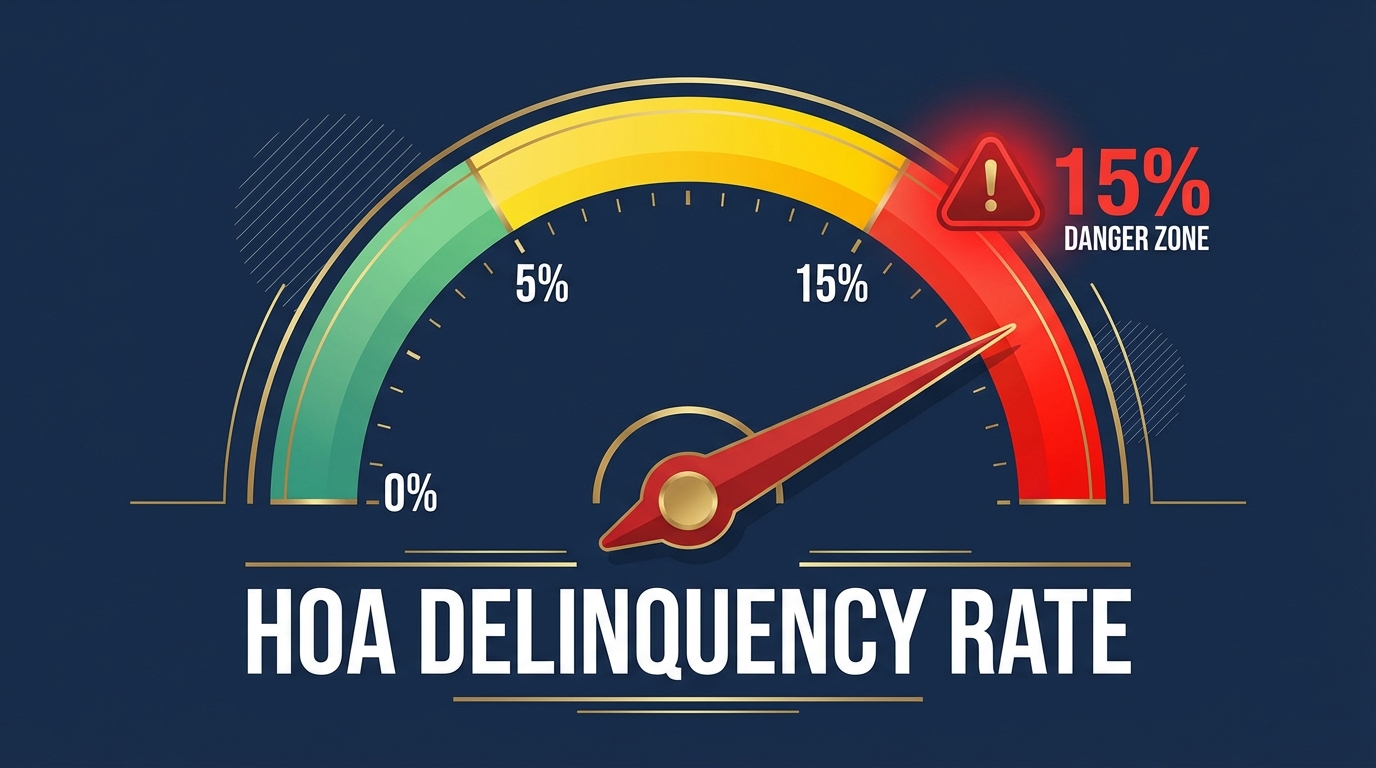

If more than 15% of units in a condo building are 60+ days behind on HOA dues, Fannie Mae, Freddie Mac, and FHA all refuse to back mortgages on any unit in the building. That one number can make your condo non-warrantable overnight.

You found the perfect condo. Offer accepted. Inspection passed. Then your lender comes back with bad news: the building's HOA delinquency rate is too high. Mortgage denied.

It doesn't matter that you have perfect credit. It doesn't matter that you put 20% down. When too many owners in your building stop paying their HOA dues, every unit in the building becomes unfundable. Your neighbors' unpaid bills just killed your purchase.

The HOA delinquency rate is the single most overlooked number in condo buying. Most buyers never ask about it. Most agents don't think to check. But lenders check every time. Here's what the number means, where the cutoff is, and how to find it before you waste months on a deal that was dead from the start.

What Is the HOA Delinquency Rate?

The percentage of units in a condo building that are 60 or more days past due on HOA assessment payments.

The HOA delinquency rate measures how many unit owners in a building are behind on their dues. It's calculated with a simple formula:

Delinquency Rate = (Units 60+ days past due on assessments) ÷ (Total units in building) × 100

A 200-unit building where 32 owners are two or more months behind on dues has a 16% delinquency rate. That single percentage is enough to block every mortgage in the building.

The denominator is total units in the project, not occupied units or units that owe dues. And the threshold is 60 days past due, which is consistent across Fannie Mae, Freddie Mac, and FHA.

One important nuance: regular assessment delinquency and special assessment delinquency are calculated separately. If 14% of owners are behind on regular dues and 7% are behind on a special assessment, those numbers are not combined. Both are under 15%, so the building passes. This distinction comes directly from the Fannie Mae and Freddie Mac selling guides.

The 15% Threshold That Kills Conventional Financing

Fannie Mae, Freddie Mac, and FHA all set the cutoff at 15% of units 60+ days past due. The VA uses a similar benchmark.

Every major mortgage agency in the country uses the same number. If more than 15% of units are 60 or more days delinquent on assessments, the project is ineligible for conventional financing.

| Agency | Delinquency Threshold | Past Due Period | Guide Reference |

|---|---|---|---|

| Fannie Mae | 15% of units | 60+ days | Selling Guide B4-2.1-03 |

| Freddie Mac | 15% of units | 60+ days | Guide Section 5701.5 |

| FHA / HUD | 15% of units | 60+ days | HUD Handbook 4000.1 |

| VA | ~15% (guideline) | Holistic review | VA Pamphlet 26-7, Ch. 16 |

Fannie Mae spells it out in Selling Guide section B4-2.1-03: if more than 15% of units are 60+ days past due on common expense assessments, the project is ineligible. The same standard applies whether the lender uses the full review process (B4-2.2-02) or the limited review process (B4-2.2-01).

Freddie Mac mirrors Fannie's rule in Guide Section 5701.5. Projects that exceed 15% receive a "Not Eligible" status in Freddie Mac's Condo Project Advisor tool. No exceptions.

FHA adopted the same 15% / 60-day standard as part of its 2019 condominium rule modernization (Federal Register 84 FR 41694). FHA also offers a bonus: if delinquency is 10% or below, the owner-occupancy requirement drops from 50% to 35%, making approval easier.

The VA doesn't publish a hard numerical cutoff. VA Pamphlet 26-7, Chapter 16 describes a holistic financial review. But multiple mortgage industry sources confirm the VA uses roughly 15% as a working benchmark. High delinquency is listed as a "major red flag" that can result in VA approval being denied or revoked.

What Happens When a Building Crosses 15%

The building becomes non-warrantable. Buyers lose access to conventional, FHA, and VA loans. Prices drop 10-25%.

When a condo building crosses the 15% delinquency threshold, it becomes non-warrantable. That designation triggers a cascade of problems that affect every owner in the building, not just the ones who stopped paying.

Conventional financing disappears. Fannie Mae and Freddie Mac will not purchase loans on any unit in the building. That eliminates roughly 70% of the mortgage market by origination volume.

FHA and VA loans are gone too. First-time buyers using FHA and veterans using VA loans are locked out entirely. The buyer pool shrinks dramatically.

What's left costs more. Buyers who still want in must use portfolio lenders or non-QM lenders. That means higher interest rates (typically 0.5% to 2% above conventional, sometimes as high as 4% above market), larger down payments (20-30% instead of 3-5%), and fewer lenders willing to participate.

Prices fall. Sellers in non-warrantable buildings typically accept 10 to 25% less than comparable units in well-funded buildings. The buyer pool shrinks by an estimated 65-90% when conventional financing is unavailable. Cash buyers and investors dominate, and they negotiate steep discounts.

As of 2024, Fannie Mae listed 1,438 ineligible condo buildings across Florida. Nearly half (696) are concentrated in Miami-Dade, Broward, and Palm Beach counties. Many of these buildings became ineligible due to a combination of delinquency, insurance problems, and deferred maintenance.

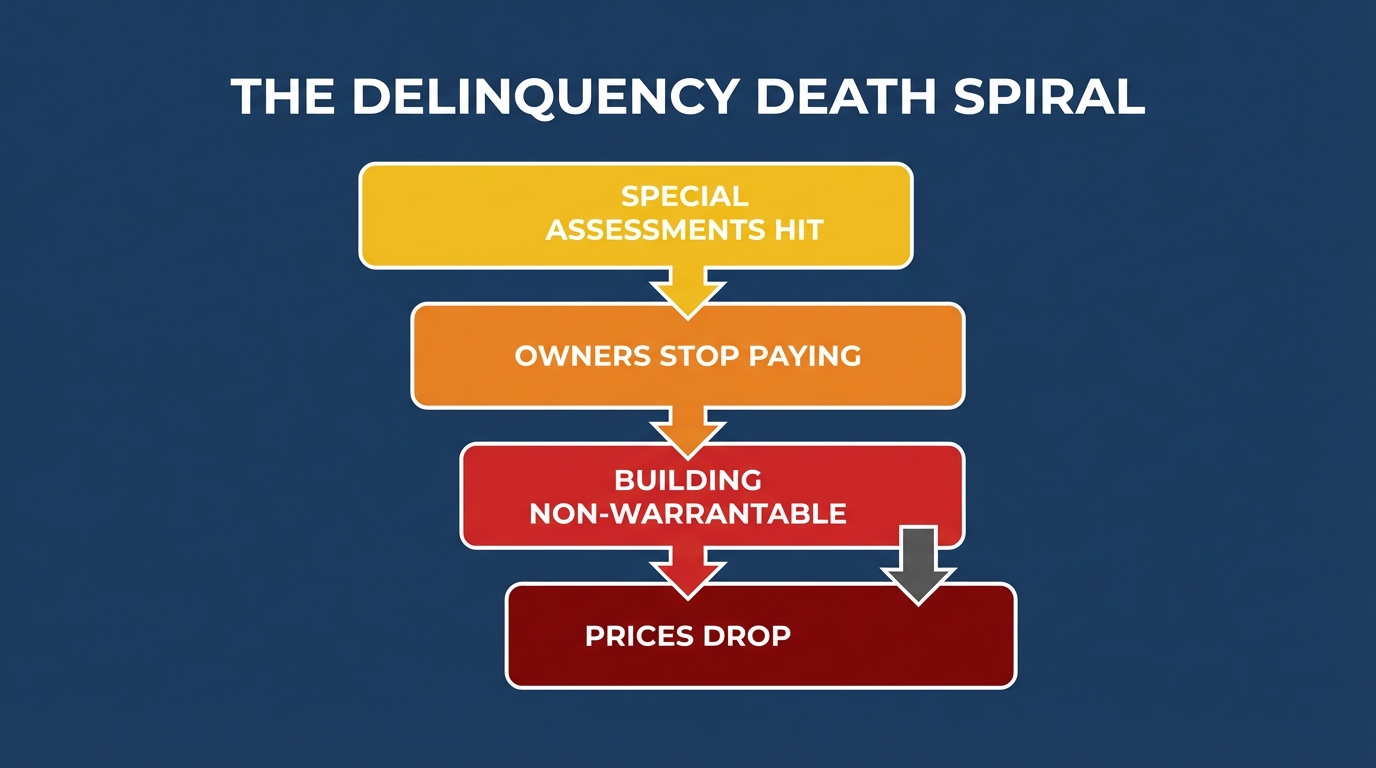

The Delinquency Death Spiral

Special assessments push owners into delinquency. Delinquency blocks financing. Blocked financing drops values. Dropping values push more owners out.

Delinquency rarely stays at 15%. Once a building crosses the threshold, a self-reinforcing cycle kicks in that makes the problem worse.

It starts with underfunded reserves. Years of deferred maintenance lead to expensive emergency repairs. The board levies a special assessment. Some owners can't afford five- or six-figure bills, so they stop paying. Delinquency climbs.

Once delinquency crosses 15%, conventional financing disappears. Fewer buyers means less demand. Prices drop. Owners who are already struggling see their equity evaporate. Some walk away entirely. Delinquency climbs further.

The association now has less revenue to fund repairs. Deferred maintenance gets worse. Insurance premiums spike. The board may levy another assessment. More owners fall behind. The cycle accelerates.

KSN Law, a Florida condo law firm, describes the endgame: "For owners on fixed incomes or tight budgets, these assessments are likely unaffordable and may lead to forced sales, mounting delinquencies, or widespread financial strain within communities."

This is exactly what's playing out across South Florida right now. The combination of new SIRS requirements, insurance rate increases, and aging buildings has pushed delinquency rates past the breaking point in hundreds of communities.

Real Buildings That Hit the Wall

Florida condo buildings are seeing assessments from $100K to $400K per unit. Owners are being forced to sell at massive losses.

These are not hypothetical scenarios. These are real buildings where delinquency and financial collapse happened in the past two years.

| Building | Assessment Per Unit | What Happened |

|---|---|---|

| Mediterranean Village, Aventura FL | Up to $400,000 | Full building remediation |

| Cricket Club, North Miami FL (220 units) | ~$134,000 | Roofing, waterproofing, wind prep. 50 years of deferred reserves. |

| Murano at Portofino, Miami Beach FL (189 units) | $66K – $322K | Two assessments totaling ~$60M in two years (varies by unit) |

| Isola Condominium, Brickell Key FL | $19M+ total | Pool deck and garage repairs after years of neglect |

At Cricket Club in North Miami, owner Ivan Rodriguez paid $119,000 for his unit in 2019. After the $30 million special assessment hit, he was forced to sell. His unit went for $110,000. He lost money on a property he owned for five years while roughly 40 of the building's 220 units sat on the market with few takers.

The common thread in every case: years of underfunded reserves leading to massive catch-up assessments. Florida's old law allowed associations to vote to waive reserve funding entirely. Many did. Now the bills are coming due all at once, and the buildings that can't pay are becoming unfundable.

The most extreme example is Champlain Towers South in Surfside. Before the June 2021 collapse, the building's reserves stood at just 6.9% of the recommended level ($706,000 versus $10.3 million recommended). Two major HOA lenders had already declined to provide loans to the association. The board levied a $15 million special assessment in April 2021, two months before the building fell.

How to Check the Delinquency Rate Before You Buy

Request the HOA questionnaire, resale certificate, and financial statements. Look for the aging of receivables report.

The delinquency rate is not on the MLS listing. Your agent probably won't mention it. But it's in the HOA documents if you know where to look.

1. Ask for the HOA Questionnaire

Lenders require the HOA to complete a questionnaire that discloses the current delinquency rate, pending litigation, insurance coverage, and reserve levels. You can request a copy from the management company or your lender. This is the single most direct source. It will state the exact percentage.

2. Request the Resale Certificate or Disclosure Package

Most states require sellers to provide a resale certificate or HOA disclosure package. This document includes the association's budget, anticipated expenditures, reserve amounts, and financial disclosures. Some states include delinquency information directly.

3. Review the Financial Statements

The association's annual financial statements include a balance sheet and income/expense report. Look for the aging of receivables report. This shows exactly how many owners are 30, 60, and 90+ days past due and the total dollar amount owed. You can calculate the delinquency rate yourself from this data.

4. Get the Estoppel Letter

The estoppel letter shows the seller's specific account status. While it doesn't show the building-wide delinquency rate, it tells you whether the seller is current. If the seller is delinquent, that's a red flag about the building's overall financial health.

5. Read the Board Meeting Minutes

Board meeting minutes often discuss collection issues, delinquent owners, and attorney engagement for collections. If the board is frequently discussing delinquency, sending lien notices, or hiring collection attorneys, the rate is likely elevated. Upload the minutes to GoverningDocs to flag collection-related language automatically.

6. Ask Your Lender Early

Don't wait until underwriting to discover the delinquency rate. Ask your lender to run a preliminary warrantability check as soon as you're under contract. If the building is already on Fannie Mae's ineligible list, your lender will know immediately.

What the Numbers Actually Mean

Under 5% is healthy. 5-8% is caution. 8-15% is a warning. Over 15% means no conventional financing.

Not every building with some delinquency is a problem. Here's how to read the number.

| Delinquency Rate | What It Means | Action |

|---|---|---|

| Under 5% | Healthy. Normal for well-managed associations. | No delinquency concerns. Check other financials. |

| 5% – 8% | Elevated. Approaching negative territory for lenders. | Investigate why. Check reserves and recent assessments. |

| 8% – 15% | Warning zone. One bad quarter could push past 15%. | Serious due diligence. Review collection policy and trends. |

| Over 15% | Non-warrantable. No conventional, FHA, or VA financing. | Walk away or prepare for portfolio lending (25-30% down, higher rates). |

CAI (Community Associations Institute) estimates that normal delinquency rates fall between 5-8% in well-managed communities. Anything above 8% is considered a negative signal by financial institutions.

But don't just look at the current number. Ask for the trend. A building at 12% that was at 8% six months ago is heading in the wrong direction. A building at 12% that was at 18% and is actively collecting is recovering. Context matters.

Also check the reserve study funding percentage. Buildings with low reserves are far more likely to levy special assessments, which push delinquency higher. A building at 10% delinquency with 20% funded reserves is a building heading toward 15%.

Frequently Asked Questions

What is a good HOA delinquency rate?

Under 5% is considered healthy for a well-managed condo association. Rates between 5-8% are in the normal range but worth investigating. Anything above 8% is a warning sign, and above 15% means the building is non-warrantable and ineligible for conventional financing from Fannie Mae, Freddie Mac, or FHA.

Can I get a mortgage on a condo with a high delinquency rate?

If the building's delinquency rate exceeds 15% at 60+ days past due, you cannot get a conventional mortgage backed by Fannie Mae or Freddie Mac, an FHA loan, or a VA loan. Your options are limited to portfolio lenders or non-QM lenders, which typically require 20-30% down payments and charge higher interest rates (0.5% to 4% above conventional rates).

How do I find out the delinquency rate for a condo building?

Request the HOA questionnaire from the management company or your lender. It directly states the delinquency rate. You can also review the association's financial statements and look for the aging of receivables report, which shows how many owners are 30, 60, and 90+ days past due. Board meeting minutes often discuss collection issues as well.

Does the 15% threshold apply to special assessments too?

Yes, but regular assessment delinquency and special assessment delinquency are calculated separately under Fannie Mae and Freddie Mac rules. If 14% of owners are behind on regular dues and 7% are behind on a special assessment, those percentages are not added together. Each is evaluated independently against the 15% cap.

What does non-warrantable mean for a condo?

A non-warrantable condo is one where Fannie Mae and Freddie Mac will not purchase mortgages on units in the building. High delinquency rates are one of several reasons a building can become non-warrantable. Others include low reserves, pending litigation, insufficient insurance, and high investor concentration.

Check Your Condo's Financial Health Before You Buy

Upload your HOA documents for free analysis. Our tools flag delinquency-related language in meeting minutes, low reserve funding in reserve studies, and assessment risks in CC&Rs. No signup required. Based on our analysis of 1,900+ HOA documents.

Related Articles

Sources & References

- Fannie Mae Selling Guide B4-2.1-03 (Ineligible projects; delinquency threshold)

- Freddie Mac Guide Section 5701.5 (Condo project ineligibility criteria)

- Federal Register 84 FR 41694 (FHA condominium rule modernization; 15% delinquency standard)

- VA Pamphlet 26-7, Chapter 16 (Common interest communities; financial review)

- Yahoo Finance (South Florida condo owners and special assessments)

- Axios Miami (Safety regulations pushing condo owners out)

- CNN Investigation (Champlain Towers South reserve fund analysis)

- CAI Foundation 2024 Fact Book (Community association statistics)

- Condo Blacklist (Fannie Mae ineligible condo buildings database)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. HOA delinquency rates, lender requirements, and building eligibility can change. Consult a qualified real estate attorney or mortgage professional for guidance specific to your situation.