In This Guide

Florida's condo crisis creates opportunities for informed buyers. SIRS-compliant, well-funded buildings hold value. Distressed properties may offer discounts but carry assessment risk of $50K-$400K per unit.

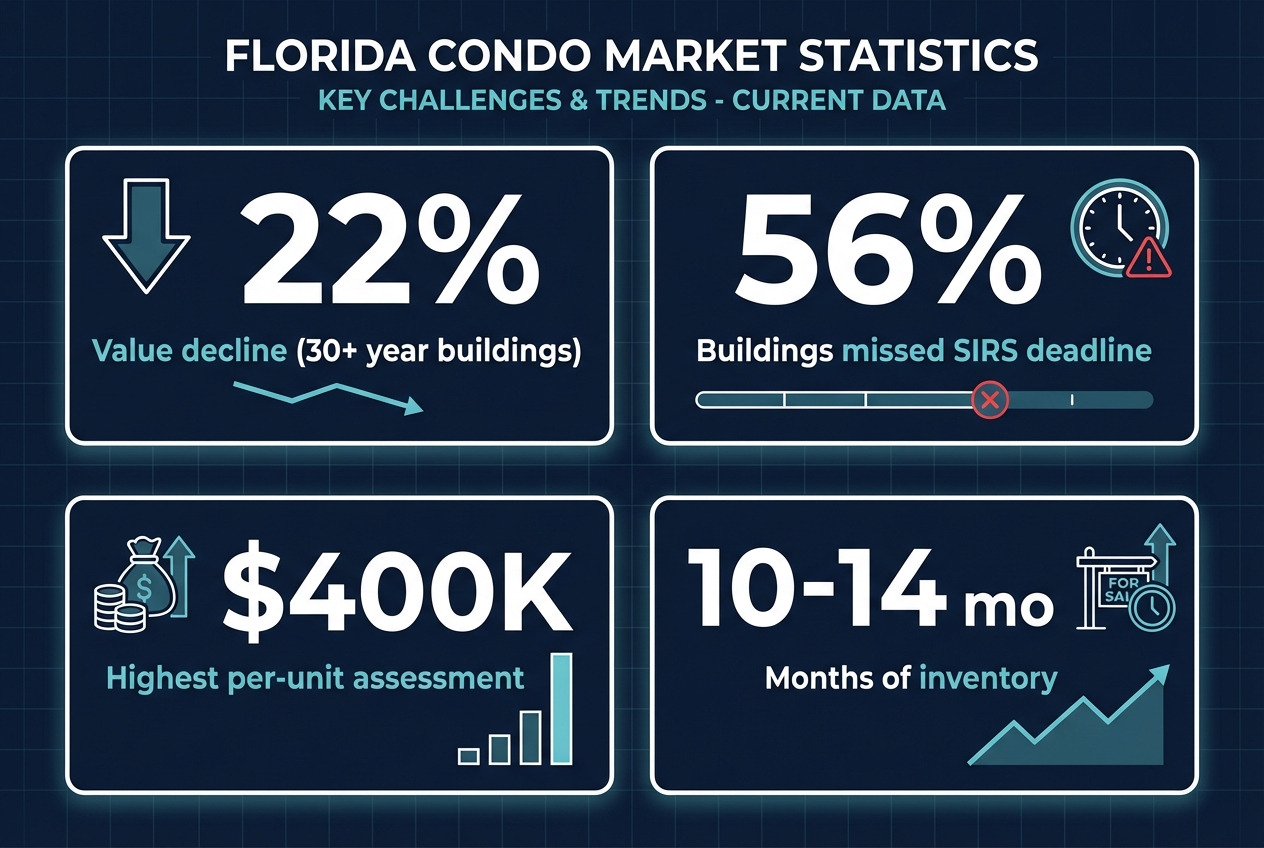

Florida condos over 30 years old have lost 19% of their value since 2023. Inventory in South Florida is sitting at 10-14 months. Sellers are desperate. If you're an investor or buyer watching from the sidelines, this looks like a fire sale.

But cheap doesn't mean safe. The same forces pushing prices down (SIRS requirements, special assessments, insurance spikes) can turn a "bargain" into a six-figure liability. 92% of Miami-Dade condo sellers got less than asking price in 2025. Some of those sellers were cutting their losses after getting hit with assessments they couldn't absorb.

The opportunity is real. So is the risk. The difference between a smart buy and a disaster comes down to knowing which buildings have already done the hard work and which ones are still pretending the bill isn't coming.

Based on GoverningDocs Research

This guide draws on our analysis of 1,900+ HOA documents, including 70 Florida SIRS reports. Statistics reflect real reserve study data from our corpus.

The Current Market Reality

Florida's condo market is in a buyer's market driven by post-Surfside safety laws, rising insurance, and mandatory reserve funding that took effect January 1, 2026.

The numbers paint a clear picture. Condos over 30 years old in South Florida have dropped 19% in value since 2023. In Miami-Dade County, 92% of condo sellers got less than their asking price. Inventory in South Florida is sitting at 10-14 months, well above the 6 months that signals a balanced market.

Three forces are driving this simultaneously. First, the SIRS deadline passed on December 31, 2025, and over 56% of buildings in Miami-Dade that were required to comply still haven't finished. Second, reserve fund waivers were banned as of January 1, 2026. Boards that had been deferring contributions for years now have to start funding. Third, insurance premiums have spiked across South Florida, with some buildings seeing 2-3x increases in a single renewal cycle.

The result: a flood of motivated sellers who either can't afford the assessment or don't want to wait around for it. Miami-Dade County had to create a 0% interest loan program so owner-occupants could borrow up to $50K just to cover their assessment obligations (the program was temporarily paused in mid-2025 due to high demand).

Key market indicators for Florida's condo market in 2026

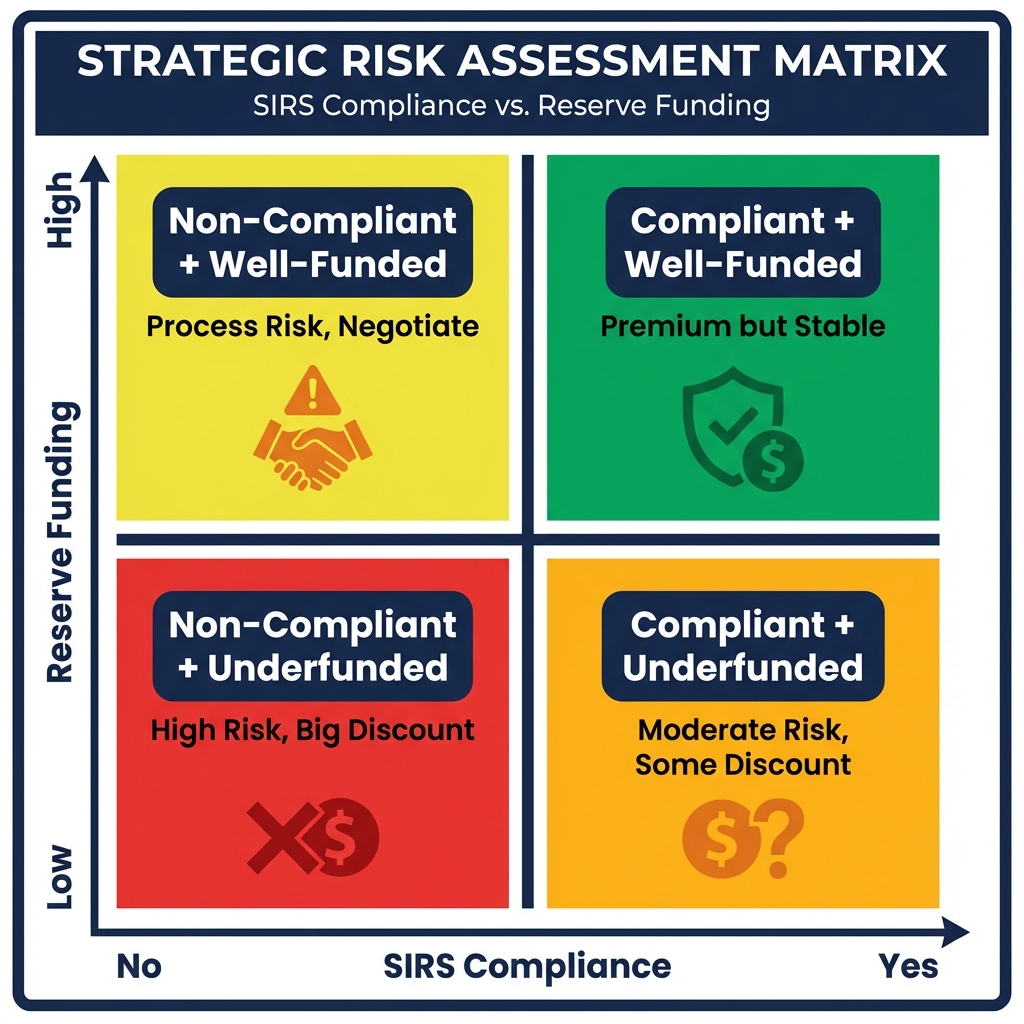

The Risk-Opportunity Matrix

Not all Florida condos carry the same risk. SIRS compliance status and reserve funding level create four distinct categories of investment opportunity.

Every Florida condo you evaluate falls into one of four buckets. Where it lands determines your risk, your financing options, and your likely return.

Four categories of Florida condo investment based on compliance and funding

| Category | Risk Level | Typical Discount | Financing |

|---|---|---|---|

| Compliant + Well-Funded | 🟢 Low | Minimal (5-10%) | Conventional available |

| Compliant + Underfunded | 🟡 Moderate | 10-20% | Conventional possible, check reserves |

| Non-Compliant + Well-Funded | 🟠 Elevated | 15-25% | May need portfolio lender |

| Non-Compliant + Underfunded | 🔴 High | 25-40%+ | Cash only in most cases |

The Sweet Spot: Compliant Buildings with Temporary Discounts

The most interesting category for informed buyers is buildings that have already completed SIRS compliance and funded their reserves but are still trading at a discount because the broader market hasn't caught up. These buildings did the hard work. They absorbed the assessment. The sellers who couldn't handle it have already left. What remains is a building on the other side of the worst.

Look for buildings where the SIRS report is complete, reserves are above 50% funded, and the board has a multi-year funding plan in place. These properties are priced like the crisis is still happening but the actual financial risk has already been addressed.

How to Identify SIRS-Compliant Opportunities

Check MyFloridaLicense.com for SIRS filing status, then request the actual reserve study to verify funding levels. Buildings that completed compliance early are often the best opportunities.

Start with the public record. Florida's DBPR (Department of Business and Professional Regulation) database shows whether a condo association has filed its SIRS report. This is your first filter. If the building hasn't filed, you know you're dealing with a non-compliant property and should price accordingly.

But filing alone isn't enough. A building can file a SIRS report and still be critically underfunded. Our analysis of 70+ Florida SIRS reports found a bimodal distribution: 65% of buildings were at or near 100% funded, while 27% were critically underfunded below 30%. Almost nothing in the middle. Buildings either took it seriously or they didn't.

After confirming SIRS filing status, request these documents:

- The SIRS report itself (not just the filing confirmation). Check percent funded, components at end of useful life (RUL=0), and the recommended annual contribution.

- Milestone Inspection report (required for buildings 30+ years old). This is the structural engineering assessment. Look for any findings classified as "substantially structural" which trigger mandatory repairs.

- Board meeting minutes (last 24 months). Search for anything "tabled" or "deferred." This is where you find the gap between what the SIRS report recommends and what the board actually does.

Pro Tip

Buildings that completed SIRS compliance early (before the December 2025 deadline) are a positive signal. It means the board was proactive, not reactive. That same proactive mindset usually carries over to maintenance and financial management.

Evaluating Distressed Properties

The listed price is never the true cost. Add the likely special assessment, insurance increase, and deferred maintenance to calculate your real basis in the property.

When a Florida condo is priced 30-40% below comparable units in the area, there's a reason. Your job is to figure out whether that reason is priced into the discount or not.

Calculate the True Cost

Purchase price + likely assessment + insurance premium increase + deferred maintenance share = your real basis.

Start with the reserve study. If the building is 30% funded and needs $5M in reserves, the gap is $3.5M. Divided across 100 units, that's $35,000 per unit that has to come from somewhere. Either through a special assessment, a dues increase, or a combination of both. That number gets added to your purchase price.

Then check insurance. Florida condo insurance has been one of the biggest cost drivers. Some buildings have seen premiums go from $80K to $220K in a single renewal. That cost gets passed to unit owners through HOA fees. Ask for the last three years of insurance renewals to see the trend.

Watch Out

If a building's master insurance policy has been non-renewed or the carrier has pulled out entirely, the building is likely non-warrantable. No conventional financing. Cash only. And reselling later will be extremely difficult.

Financing Considerations

Fannie Mae and Freddie Mac now require SIRS compliance, adequate reserves, and current insurance for conventional financing. Non-compliant buildings are effectively cash-only.

Financing is where the crisis hits hardest. Fannie Mae and Freddie Mac's condo questionnaire now asks about SIRS compliance, reserve funding, structural inspections, and insurance adequacy. If the building fails any of these checks, it becomes non-warrantable. That means no conventional mortgage.

Non-warrantable status triggers a death spiral that we're already seeing play out across the state. Nearly 1,500 Florida condo buildings are now on Fannie Mae's restricted list. The building fails the reserve threshold. Fannie and Freddie won't back loans. The buyer pool shrinks to cash buyers and portfolio lenders. Fewer buyers means lower prices. Lower prices mean less equity for current owners to absorb the assessment. More owners sell at a loss. Prices drop further.

The Cash Buyer Advantage

If you're buying cash, this is where the biggest discounts live. Non-warrantable buildings have fewer competing buyers, more motivated sellers, and less price support. But the risk is proportional. You're buying into a building that may not be financeable for years. Your exit depends on the building regaining warrantable status, which depends on the board fixing the problems that caused the designation in the first place.

For financed buyers, focus on SIRS-compliant buildings with reserves above 10% of the annual budget (Fannie Mae's threshold). Ask your lender to run a warrantability check early in the process. Don't wait until underwriting to find out the building doesn't qualify.

Check a Building's Reserve Health Before You Buy

Upload a reserve study and get instant analysis of percent funded, deferred maintenance, and lending risk flags. Free. No signup.

Analyze a Reserve Study →Based on analysis of 1,900+ HOA documents

Geographic Opportunities

Compliance rates vary dramatically by region. Markets with the lowest compliance tend to have the most motivated sellers and the biggest discounts, but also the highest risk.

Not all Florida markets are equally affected. Compliance rates range from under 30% in some counties to over 60% in others. The markets where compliance is lowest tend to have older building stock, less institutional ownership, and boards that were slower to act.

| Market | Opportunity Type | Key Factor |

|---|---|---|

| Miami-Dade / Broward | Highest volume of distressed inventory | Oldest building stock. Most assessments in progress. |

| Palm Beach | Low compliance (~28%), motivated sellers | Luxury and mid-tier mix. Higher price points. |

| Orlando / Central FL | Newer stock, fewer SIRS requirements | Less crisis impact. Steady rental demand. |

| Tampa Bay / Gulf Coast | Post-hurricane rebuilds, insurance challenges | Some buildings completed repairs. Recovery play. |

| Southwest FL (Cape Coral, Fort Myers) | Value markets with motivated sellers | Post-Ian recovery. Lower price points. Cash buyer territory. |

Market conditions as of early 2026. Verify current data before making investment decisions.

The best geographic strategy depends on your buyer profile. Financed buyers should focus on Orlando and Central Florida where SIRS impact is minimal and conventional loans are still available. Cash buyers with higher risk tolerance can find the biggest discounts in Miami-Dade, Broward, and Palm Beach.

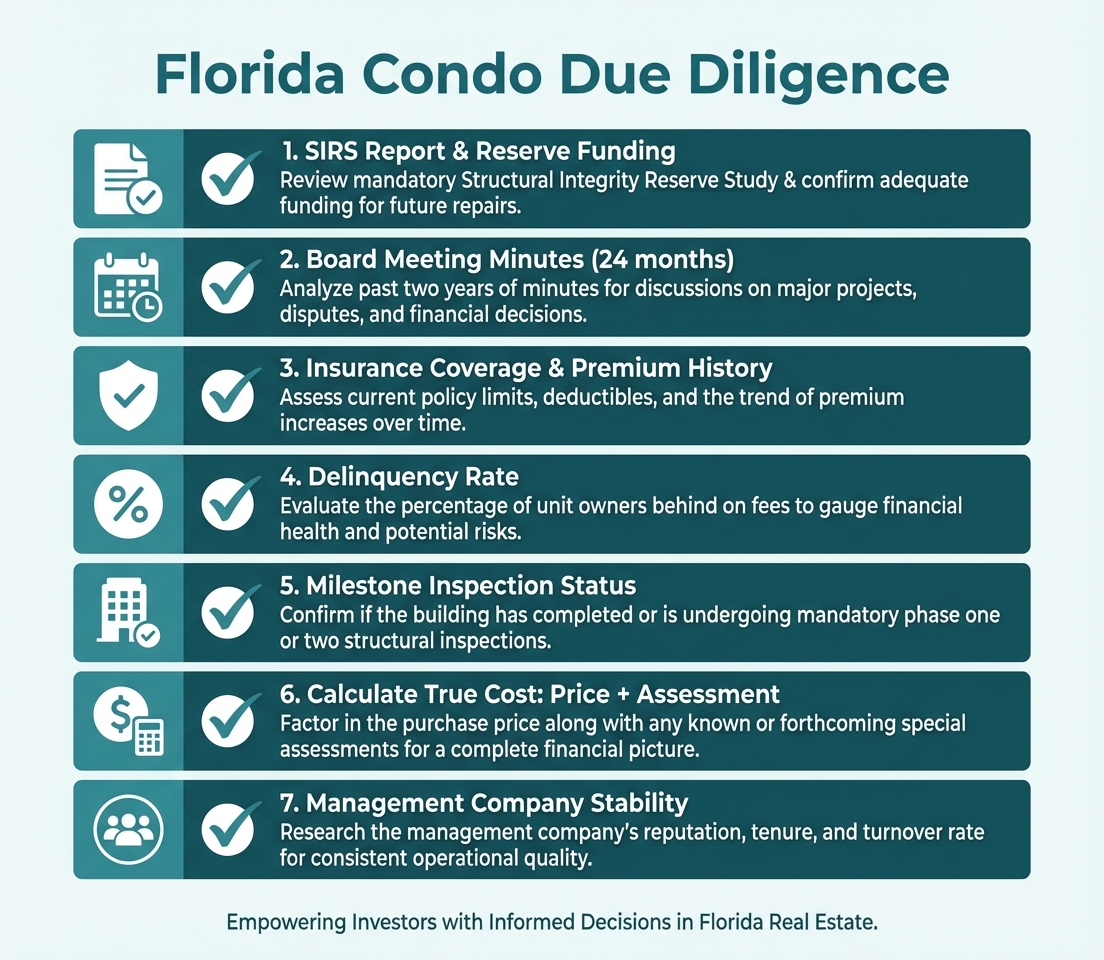

Due Diligence Checklist for Investors

Seven documents and data points every Florida condo investor must check before making an offer.

Complete due diligence checklist for Florida condo investments

Before You Make an Offer:

- ☐SIRS report and reserve funding analysis. Check percent funded (below 50% is danger zone), RUL=0 components, and recommended vs actual annual contribution.

- ☐Board meeting minutes (last 24 months). Search for "tabled," "deferred," "assessment," "litigation." Deferred repairs don't disappear. They compound.

- ☐Insurance coverage and premium history. Request the last 3 years of master policy renewals. Look for coverage reductions, carrier changes, or non-renewal notices.

- ☐Delinquency rate. Above 15% is a red flag for both building financial health and Fannie Mae warrantability. Ask the management company directly.

- ☐Milestone Inspection status. For buildings 30+ years old, confirm the milestone inspection is complete and check for any "substantially structural" findings.

- ☐True cost calculation. Purchase price + likely assessment + insurance increase + deferred maintenance. If this number exceeds comparable compliant units, the discount isn't real.

- ☐Management company stability. Has the management company changed recently? Frequent turnover is a sign of board dysfunction or financial problems that scare off professional managers.

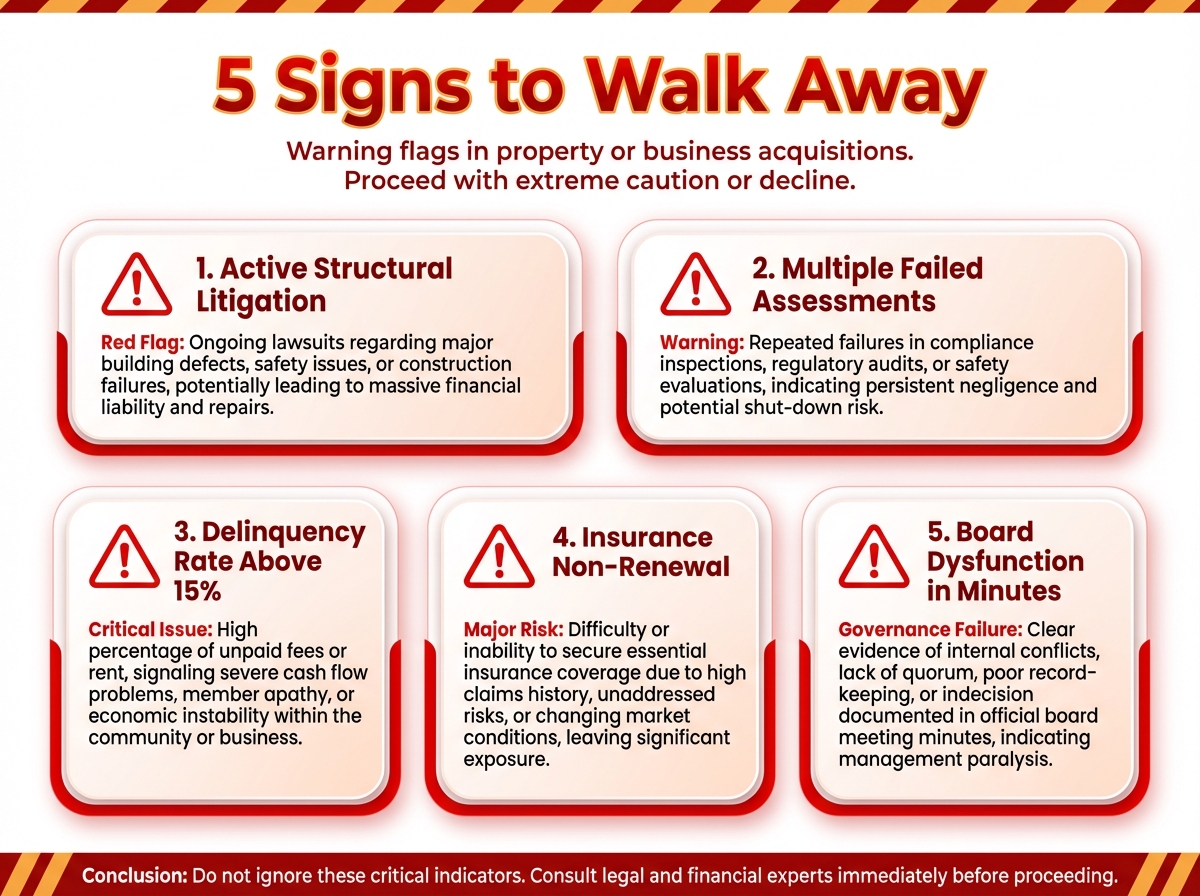

When to Walk Away

Some buildings are bargains. Others are traps. Five signs that a distressed condo is not worth the risk at any price.

Red flags that should make you walk away from any deal

Active structural litigation. If the building is suing the developer, a contractor, or its own board over structural defects, the outcome is unpredictable and the timeline is long. Litigation can freeze insurance, prevent financing, and tank resale value for years.

Multiple failed assessments. If the board has attempted to levy assessments and owners have refused to pay or voted them down, the building has a governance problem that no amount of discount can fix. The repairs still need to happen. The money still isn't there. And now there's a track record of non-compliance.

Delinquency rate above 15%. This is both a Fannie Mae disqualifier and a signal of broader financial distress. When 15% or more of owners aren't paying their dues, the building can't fund basic operations, let alone reserves.

Insurance non-renewal. If the building's master policy has been non-renewed and they're operating on surplus lines or have gaps in coverage, the building is effectively uninsurable at standard rates. This makes it non-warrantable and creates massive liability exposure for every owner.

Board dysfunction in the minutes. If meeting minutes show a revolving door of board members, shouting matches, failed quorums, or a board that consistently overrides professional recommendations from their reserve study firm or engineer, the building's problems are governance problems. Money alone won't fix them.

Bottom Line

A 40% discount on a condo with active litigation, no insurance, and a dysfunctional board is not a bargain. It's someone else's exit strategy. The discount exists because informed buyers have already walked away.

Frequently Asked Questions

Is now a good time to buy a Florida condo?

It depends on the building, not the market. SIRS-compliant buildings with healthy reserves are trading at temporary discounts because the broader market is depressed. These can be good opportunities. Non-compliant buildings with unknown assessment exposure are not bargains regardless of price.

How do I check if a Florida condo is SIRS compliant?

Start with the Florida DBPR database at MyFloridaLicense.com to check filing status. Then request the actual SIRS report from the association to verify the findings and funding levels. Filing alone does not mean the building is adequately funded.

What is a non-warrantable condo?

A condo that doesn't meet Fannie Mae or Freddie Mac eligibility requirements for conventional financing. Common reasons include reserve funding below 10% of the annual budget, delinquency rates above 15%, active litigation, or insurance coverage gaps. Non-warrantable buildings can only be purchased with cash or portfolio loans.

How much are Florida condo special assessments in 2026?

Assessments vary wildly depending on the building's condition and size. Ranges go from $15,000 for minor deferred maintenance to $400,000 per unit at Mediterranean Village in Aventura. The average for buildings with major structural work is $50K-$100K per unit. The reserve study will tell you how much the building needs.

Can I get a mortgage on a Florida condo right now?

Yes, if the building is SIRS compliant, has adequate reserves, current insurance, and low delinquency. Many buildings still qualify for conventional loans. But a growing number are falling out of compliance, which limits financing to cash or portfolio lenders. Ask your lender to run warrantability early.

When will Florida's condo market recover?

Recovery is expected to be building-by-building, not market-wide. Compliant buildings with completed repairs will likely stabilize first, potentially by late 2026. Non-compliant buildings may take years longer as they work through assessments, repairs, and regaining warrantable status.

Sources & References

- South Florida condo owners dumping homes after six-figure assessments — Yahoo Finance (19% price decline, Cricket Club $134K/unit)

- 62% of South Florida condo associations failed to complete SIRS by 2025 deadline — Condo Vultures / Miami Association of Realtors (Feb 2025)

- Homebuyers scored the biggest discounts in more than a decade in 2025 — ConsumerAffairs (92% of Miami sellers below asking)

- Number of Florida condos on mortgage blacklist is growing — Newsweek (1,438 buildings on Fannie Mae restricted list)

- Aventura condo owners face unprecedented special assessments — Brosda & Bentley (Mediterranean Village $400K/unit)

- Condo HOA fees surge in Florida amid insurance crisis — Redfin (2024)

- Condo prices May 2025 — Redfin (Fannie Mae restricted list data)

- Condominium Special Assessment Program — Miami-Dade County ($50K 0% interest loans)

- Florida Senate Bill 4-D (2022) — Florida Senate (SIRS requirements)

- Florida House Bill 913 (2025) — Florida House of Representatives (buyer protections)

Proprietary statistics (reserve funding distribution, component analysis) are based on GoverningDocs analysis of 70 Florida SIRS reports. All other statistics are sourced from the publications listed above. This article is for informational purposes only and does not constitute legal or financial advice.