In This Guide

Florida agents must disclose SIRS compliance status, explain reserve funding levels to clients, and navigate new buyer review periods. Understanding these requirements can help protect your clients and your transactions.

Your buyer found a beachfront condo in Fort Lauderdale. The price is $40K below comps. HOA fees look reasonable. Then you pull the association documents and realize the building hasn't completed its SIRS. No milestone inspection either. And the reserve fund is sitting at 18% funded.

This scenario is playing out across Florida right now. Reported estimates suggest over half of condo associations in some South Florida markets may not have completed their SIRS by the original deadline. That means agents are fielding questions they weren't trained for. What's a SIRS? Is this building safe? Am I going to get hit with a $200K assessment? Can I even get a mortgage here?

The agents closing deals in this market are the ones who can answer those questions. This guide covers the new rules, what you need to disclose, and how to evaluate buildings for your clients. It's based on publicly available Florida statutes, published industry data, and analysis of over 1,900 HOA documents.

Note: This guide is for informational purposes only. It is not legal advice. Florida real estate law is complex and varies by situation. Consult a licensed Florida attorney or your broker for guidance on specific transactions.

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

The Agent's Dilemma in 2026

Florida condo agents are navigating a market with more disclosure rules, more buyer hesitation, and more risk than at any point in recent memory.

Condo sales volume in parts of South Florida has reportedly dropped significantly from pre-crisis levels. Buyers are cautious. Headlines about six-figure special assessments and structural safety concerns have made every condo transaction more complex.

At the same time, disclosure requirements have expanded. The Florida Legislature passed HB 913 in 2025, which expanded seller disclosure requirements, extended the buyer cancellation period, and mandated website disclosures for larger associations.

Most real estate training programs haven't caught up. Agents are expected to understand SIRS reports, milestone inspections, reserve funding analysis, and updated disclosure requirements with minimal guidance.

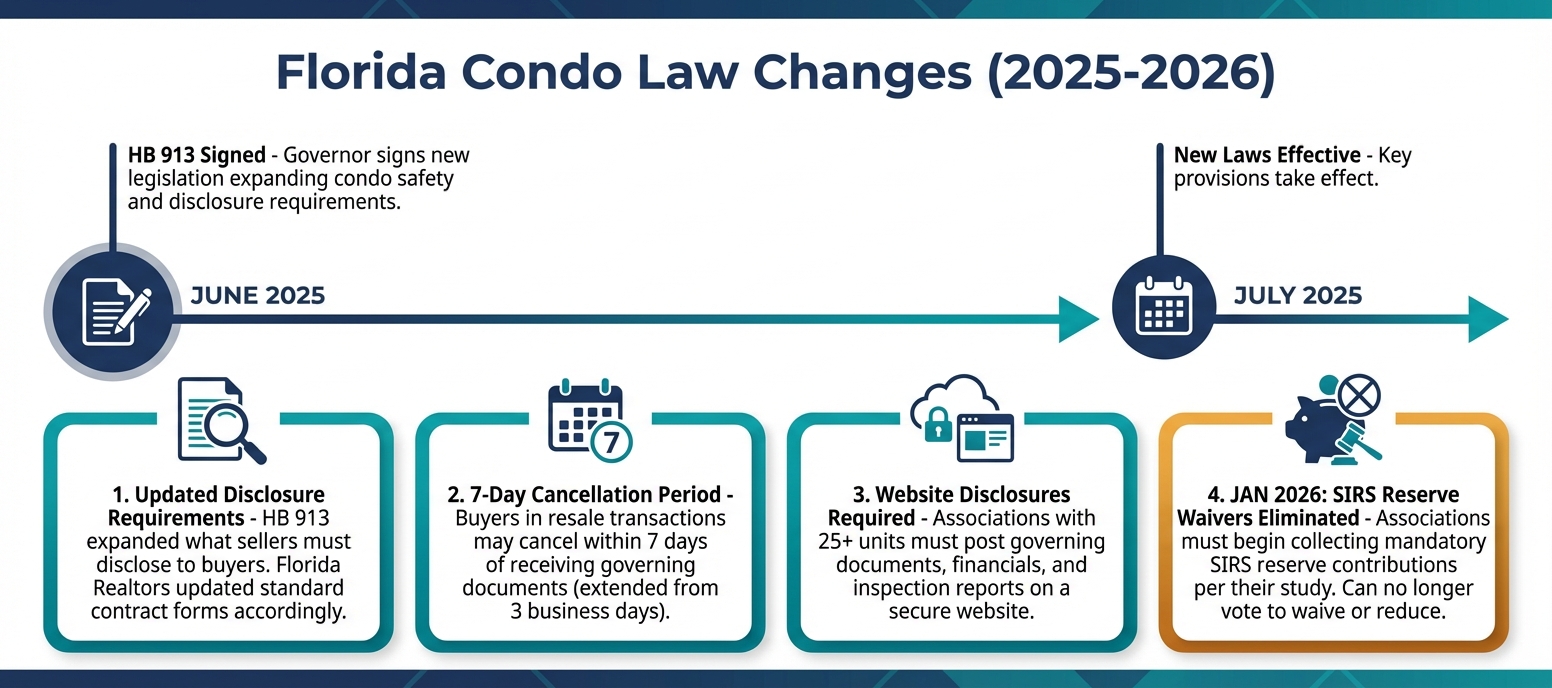

What Changed in 2025-2026

HB 913 (signed June 2025, effective July 2025) changed the timeline and disclosure requirements for Florida condo transactions.

Key Florida condo law changes affecting real estate agents (2025-2026)

Updated Disclosure Requirements

HB 913 expanded what sellers must disclose to buyers in resale condo transactions, including SIRS compliance status. In response, Florida Realtors and the Florida Bar updated the standard Condominium Rider (CR-7) to reflect these changes. Agents should verify the current form version with their broker.

7-Day Cancellation Period

For resale transactions, buyers now have 7 days (excluding weekends and holidays) to cancel the purchase agreement after receiving governing documents. This was extended from 3 business days under prior law. This is a cancellation right, not just a review window. Agents should verify the specific terms applicable to their transaction.

Website Disclosure Requirements

Associations with 25 or more units are now generally required to maintain a website with certain governing documents, financial records, and inspection reports accessible to owners and prospective buyers.

SIRS Reserve Waivers Eliminated (January 2026)

As of January 1, 2026, associations must begin collecting mandatory reserve contributions for the 8 structural components covered by SIRS, as determined by their reserve study. The prior ability for owners to vote to waive or reduce these contributions has been eliminated. This does not mean associations must be "fully funded" immediately, but they can no longer defer SIRS funding. This is the single biggest change for buyer cost expectations. Consult the current version of Florida Statute §718.112 for authoritative details.

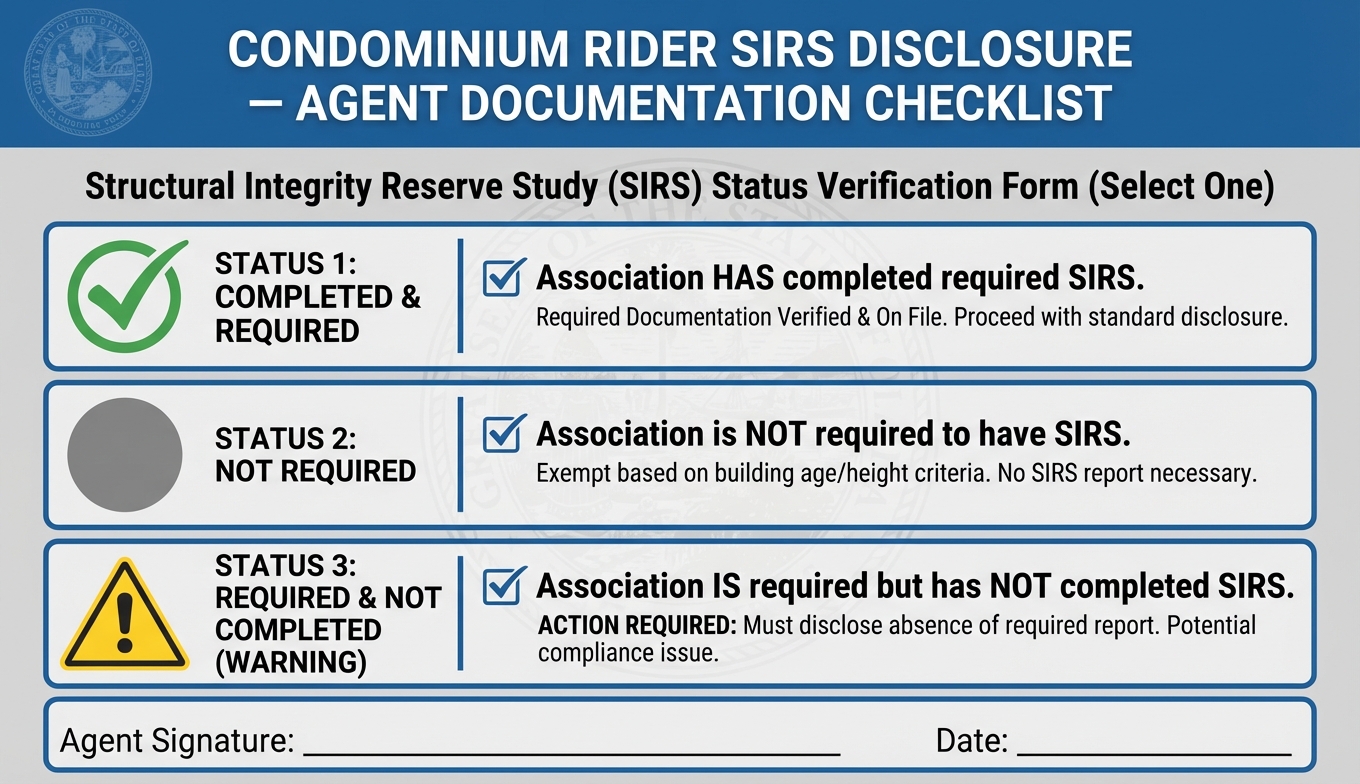

Your New Disclosure Obligations

HB 913 expanded resale disclosure requirements. The updated Condominium Rider (CR-7) now includes SIRS compliance status. Agents should understand these categories and verify current requirements with their broker.

The three SIRS compliance statuses agents should be prepared to document

Association HAS completed required SIRS

The building has its SIRS on file. Request a copy and review the funding levels. This is the strongest position for buyers and financing.

Association is NOT required to have SIRS

Generally applies to buildings under 3 habitable stories. Document this clearly. These buildings may still have a traditional reserve study, which is still worth reviewing.

Association IS required but has NOT completed SIRS

This is the category that requires the most client education. Non-compliant buildings may face financing restrictions, and buyers should understand the potential for future assessments once the SIRS is completed.

Beyond the rider, Florida's material facts disclosure obligation still applies. If you know or should know about conditions that could materially affect the property's value, you generally have an obligation to disclose them. A building that hasn't completed a required SIRS, or one with critically low reserve funding, could fall into this category. When in doubt, consult your broker or a real estate attorney.

How to Explain SIRS to Buyers

Most buyers have never heard of SIRS. Here's a framework for explaining it clearly without overcomplicating the conversation.

When a buyer asks "What is SIRS?", keep it simple. A SIRS (Structural Integrity Reserve Study) is a Florida-specific reserve study focused on 8 structural building components. It was created after the Surfside condo collapse in 2021 to help ensure condo buildings set aside money for structural maintenance.

The key points buyers need to understand:

- It's not a full reserve study. A SIRS covers 8 structural components (roof, structure, electrical, plumbing, waterproofing, windows, fire protection, elevators). A traditional reserve study covers everything (50-100+ components).

- Funding can no longer be waived. Unlike traditional reserves, associations can no longer vote to waive or reduce SIRS component funding as of January 2026. They must begin collecting contributions per their reserve study.

- It tells you the financial risk. Check the percent funded figure and any items with RUL=0 (remaining useful life exhausted). These are indicators of potential near-term costs.

- Non-compliance is a red flag. Buildings that haven't completed a required SIRS may face lending restrictions and could see significant assessments once they do comply.

For a deeper breakdown of SIRS reports, point clients to our Florida SIRS Reports Explained guide.

Questions Buyers Will Ask (And How to Approach Them)

Here are the most common buyer questions in Florida condo transactions right now, and frameworks for addressing them.

"Is this building safe?"

Explain the difference between a milestone inspection (structural safety assessment by an engineer) and a SIRS (financial reserve plan). A completed milestone inspection addresses structural safety. A SIRS addresses financial preparedness. Buyers generally want to see both. If either is missing, help them understand what that means for their due diligence. For structural safety questions specifically, refer clients to qualified engineers.

"Will I get hit with a special assessment?"

No one can guarantee the answer. But you can help buyers evaluate the risk. Check the reserve funding % (industry benchmarks suggest 70%+ as a healthier range). Look for RUL=0 items (components past their useful life). Review board meeting minutes for any discussion of upcoming assessments. Low reserves plus aging components often correlate with future assessments.

"Can I get financing?"

Fannie Mae and other agencies have warrantability requirements for condo buildings. Buildings on restricted lists, those without required structural inspections, or those with insufficient insurance or reserves may not qualify for conventional financing. This can significantly limit the buyer pool and affect resale value. Encourage buyers to check with their lender early in the process.

"Should I walk away?"

This isn't a decision agents should make for clients. But you can help them evaluate: What's the total cost of ownership (price + likely assessments + rising HOA fees)? Is the price discounted enough to reflect the risk? Are they comfortable with uncertainty? Sometimes the right move is negotiating a lower price rather than walking away entirely.

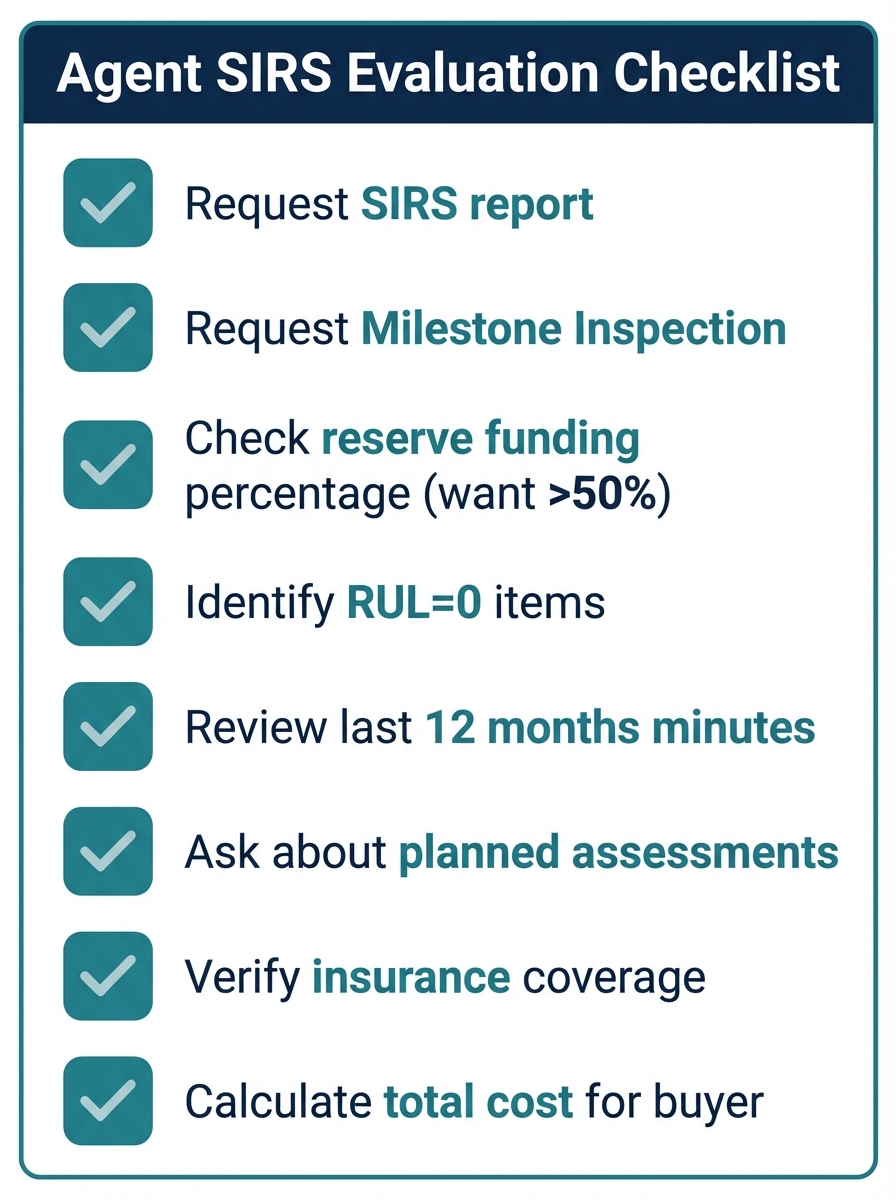

How to Evaluate a Building for Clients

A practical checklist for Florida condo due diligence. Not every item will apply to every transaction, but this covers the key areas to investigate.

Key items to check when evaluating a Florida condo building for clients

For a complete breakdown of what to look for in HOA documents, see our How to Review HOA Documents Before Buying guide.

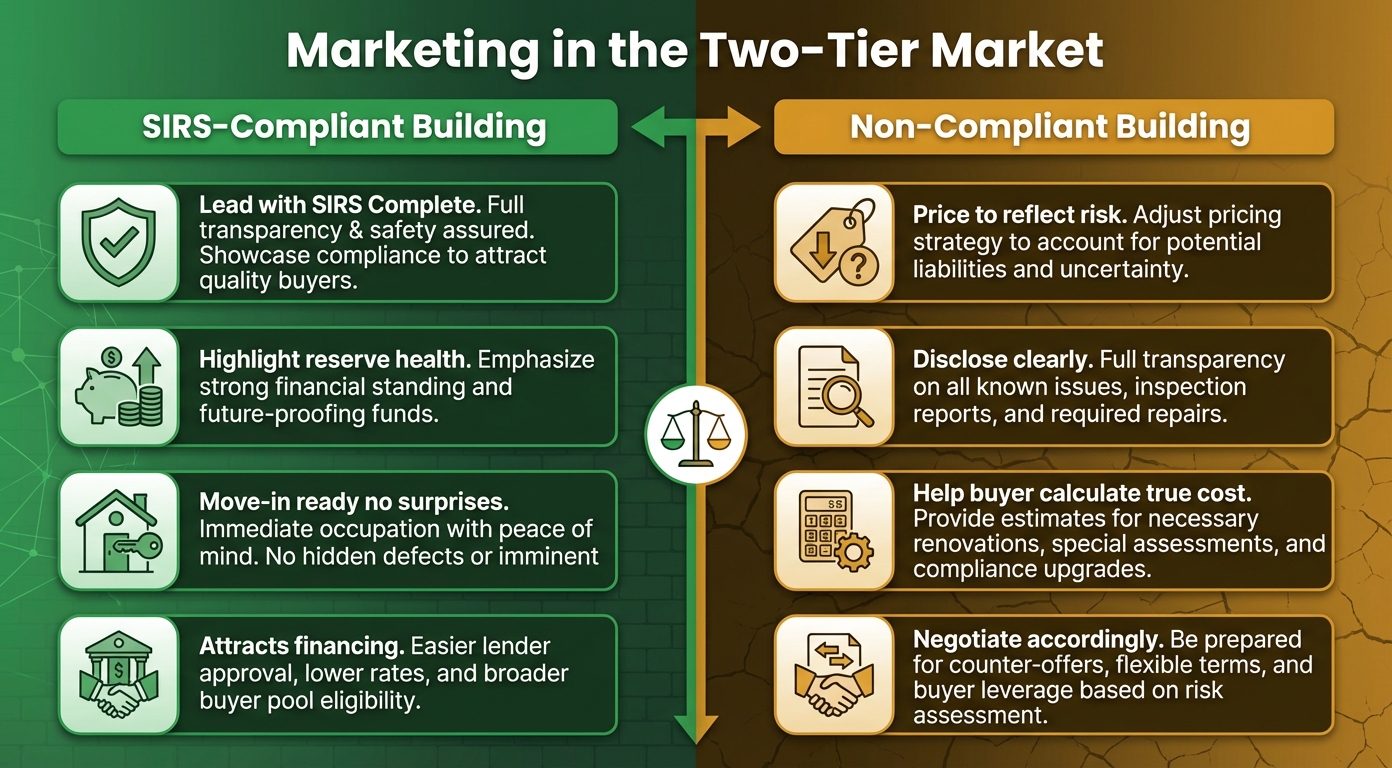

The Two-Tier Market: Compliant vs. Non-Compliant

Florida's condo market is splitting into two categories. The approach differs significantly depending on which side of the line a building falls.

How SIRS compliance status affects marketing and buyer conversations

SIRS-Compliant Buildings

- ✓Lead with "SIRS Complete" in marketing

- ✓Highlight reserve health and funding levels

- ✓Position as "move-in ready, fewer surprises"

- ✓Generally eligible for conventional financing

Non-Compliant Buildings

- ⚠Price should reflect the compliance gap

- ⚠Disclose status clearly to all parties

- ⚠Help buyers calculate true cost (price + likely assessments)

- ⚠May face financing restrictions

For listing agents: SIRS compliance is becoming a competitive advantage. If your listing's building has completed its SIRS and has healthy reserves, make that a selling point. Buyers are learning to ask, and the ones who don't will hear about it from their lender.

For buyer's agents: When working with clients on non-compliant buildings, help them understand the full financial picture. A condo priced $50K below comps might not be a deal if a $60K assessment is likely within the next year or two. Encourage them to work through the numbers with a financial advisor.

Bottom Line: Knowledge Is Your Competitive Edge

Florida's condo market is more complex than it was two years ago. But complexity creates opportunity for agents who take the time to understand the new landscape. The agents building reputations right now are the ones who can walk clients through a SIRS report, explain what reserve funding levels mean, and help them make informed decisions.

Key takeaways for agents:

Check Your Building's Financial Health

Upload your HOA's reserve study and get instant analysis of percent funded, deferred maintenance, and special assessment risk. Free. No signup required.

Frequently Asked Questions

Do I need to be a SIRS expert to sell Florida condos?

You don't need to be an engineer or reserve analyst. But you should understand the basics: what a SIRS covers, why it matters, and what the key numbers mean. Buyers are asking these questions, and agents who can answer them are closing more deals. For technical questions, refer clients to qualified professionals.

What if the association won't provide SIRS documents?

Florida law generally requires associations to provide certain documents to prospective buyers. If an association is unresponsive, that itself may be a red flag worth noting. Consult with your broker about next steps. Associations with 25+ units should also have a website with documents accessible.

How does SIRS affect condo financing?

Fannie Mae and other agencies have warrantability requirements that include structural inspection and reserve adequacy criteria. Buildings that haven't completed required inspections, or that have inadequate reserves or insurance, may be classified as "non-warrantable," which means conventional mortgages may not be available. Buyers should consult their lender early to confirm the building qualifies.

Should I disclose SIRS non-compliance to buyers?

This is a question for your broker and potentially a real estate attorney. Generally, Florida's material facts disclosure requirements may apply to SIRS compliance status, particularly when non-compliance could materially affect the property's value or the buyer's ability to obtain financing. The updated Condominium Rider specifically addresses SIRS disclosure. Always err on the side of transparency and consult your broker.

What's the difference between a milestone inspection and SIRS?

A milestone inspection is a structural safety assessment performed by a licensed engineer. It tells you whether the building has structural deterioration. A SIRS is a financial reserve study that calculates how much the association needs to set aside for structural maintenance and repairs. The milestone tells you what needs fixing; the SIRS tells you how to fund it. Buildings generally need both to be fully compliant.

Where can I learn more about Florida's SIRS requirements?

Start with Florida Statute §718.112 for the authoritative legal text. Florida Realtors offers webinars and updated forms. The DBPR condominium portal has FAQs and compliance information. For a buyer-friendly explanation, see our Florida SIRS Reports Explained guide.

Sources & References

- Florida House Bill 913 (2025) - Florida House of Representatives (extended deadlines, 7-day review, new rider requirements)

- Florida Statute §718.112 - Florida Legislature (SIRS component requirements, mandatory funding)

- Surfside condominium collapse - Wikipedia (98 deaths confirmed, catalyst for SIRS legislation)

- DBPR Condominium FAQs - Florida Department of Business & Professional Regulation

- 62% of South Florida condo associations failed SIRS deadline - Condo Vultures, citing Miami Association of Realtors (Feb 2025)

- New 2025 Florida Condo Laws (HB 913) - Perez Mayoral, P.A.

This article is for informational purposes only and does not constitute legal, financial, or professional advice. Florida real estate and condominium law is complex and subject to change. Consult a licensed Florida attorney, your broker, or a qualified professional for guidance specific to your situation and transactions.