On March 18, 2026, Fannie Mae and Freddie Mac released coordinated policy updates that reshape how condos get financed. Reserve minimums are jumping from 10% to 15%, Limited Review is being eliminated, and every condo purchase will face more scrutiny. Here are the 6 changes and what to verify before you close.

On March 18, 2026, Fannie Mae and Freddie Mac released coordinated policy updates that reshape how condos get financed in the United States. If you're buying a condo with a conventional mortgage, these changes directly affect whether your loan gets approved and how much your HOA fees might increase.

The timing is rough. You might already be mid-search, maybe even under contract. And your lender probably hasn't flagged any of this yet. That's because some changes take effect immediately, while others phase in over the next 10 months. By the time most buyers hear about this, they'll be scrambling.

This guide breaks down the six biggest changes from Fannie Mae Lender Letter LL-2026-03 and Freddie Mac Bulletin 2026-C, what each one means for your purchase, and exactly what to verify before you close.

What Changed on March 18, 2026?

Fannie Mae and Freddie Mac simultaneously released new condo project standards affecting reserves, reviews, insurance, and investor limits.

On the same day, both agencies published matching rule changes. Fannie Mae issued Lender Letter LL-2026-03 and Freddie Mac published Bulletin 2026-C. The changes are designed to align the two agencies and tighten financial standards for condo associations.

Here's what matters for buyers. Not all changes are bad news. But every single one affects whether your condo qualifies for conventional financing.

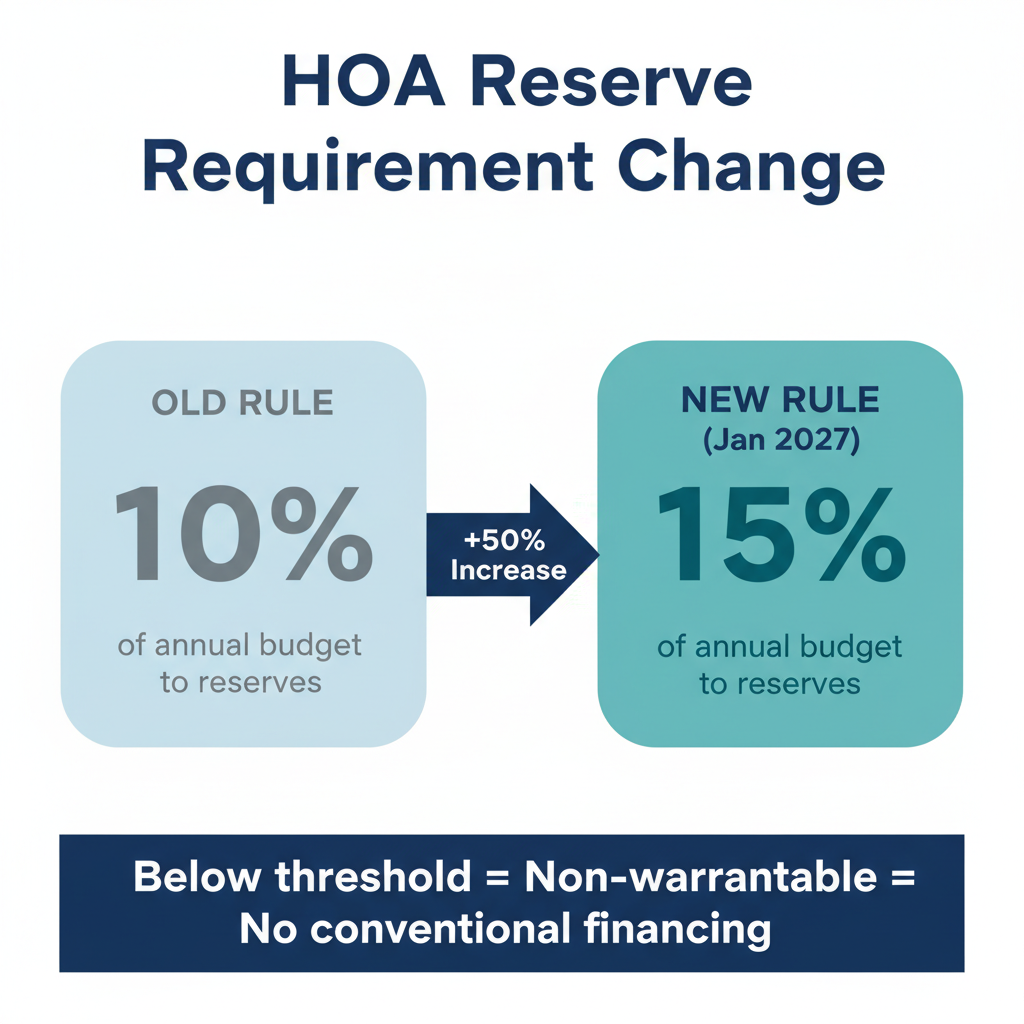

Reserve Requirements Are Jumping from 10% to 15%

HOAs must now allocate at least 15% of their annual budget to reserves, up from 10%, or risk losing warrantable status.

Effective date: January 4, 2027

This is the change that will hit buyers hardest. Both Fannie Mae and Freddie Mac are raising the minimum reserve allocation from 10% to 15% of the HOA's annual operating budget. Any condo association that falls below 15% becomes non-warrantable, meaning conventional mortgages won't be available for units in that building.

What does this mean in practice?

- HOA dues will likely increase. Associations currently at 10-14% will need to raise assessments to hit the new threshold. Budget for this when calculating your monthly costs.

- Some buildings will lose warrantable status. Based on our analysis of 1,900+ HOA documents, a significant number of associations currently operate right at the 10% floor. They have less than a year to adjust.

- Your lender will check this. The reserve allocation percentage will appear in the HOA's financial documents. Ask for the current budget before making an offer.

What to do: Request the HOA's current budget and verify the reserve allocation percentage. If it's below 15%, ask the board whether they plan to increase it before January 2027. If they don't have a plan, treat that as a red flag.

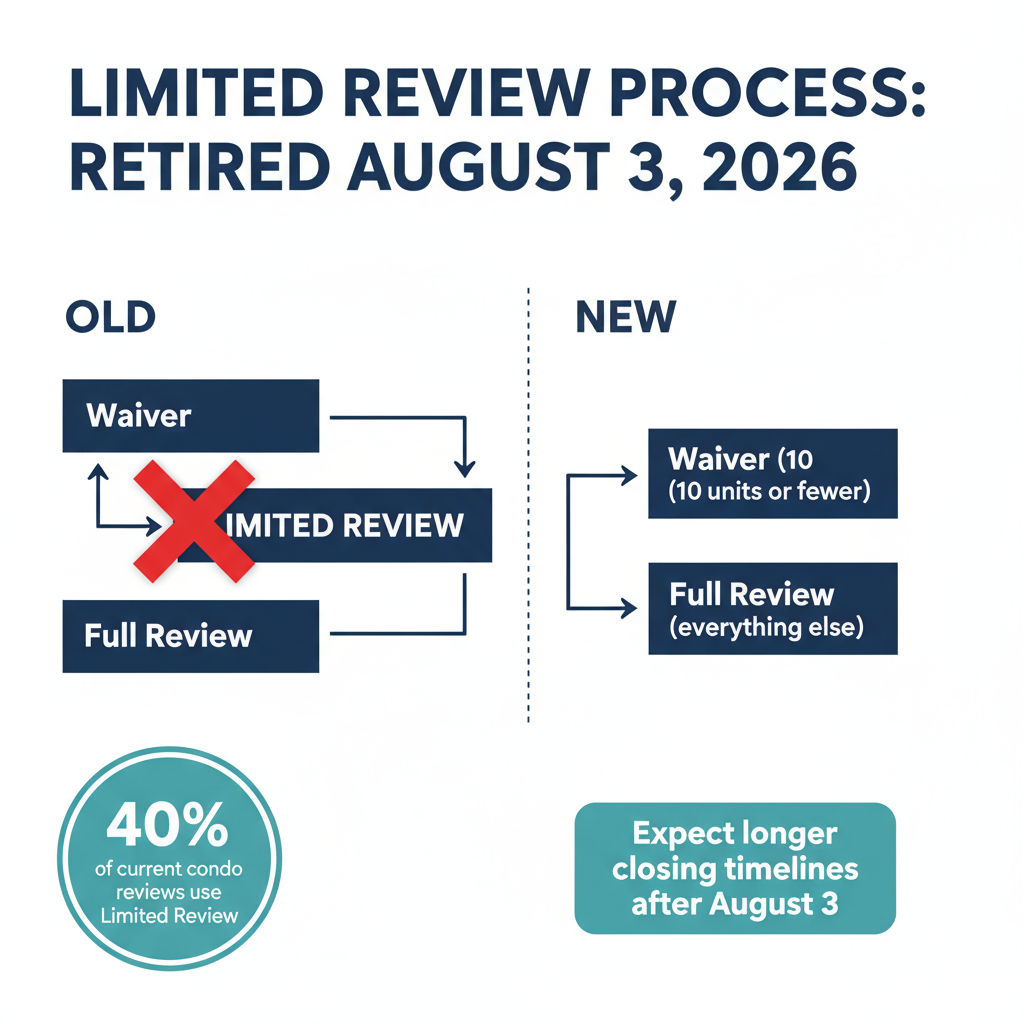

Limited Review Process Is Gone

The Limited Review option that 40% of condo transactions relied on is being eliminated, requiring Full Review for most purchases.

Effective date: August 3, 2026

This one creates real friction. Until now, many condo purchases used a Limited Review process that required less HOA documentation and less financial scrutiny. According to the Community Associations Institute (CAI), roughly 40% of current condo project reviews use this streamlined path.

Starting August 3, that option disappears. Every condo purchase will require either a Full Review or a qualifying Waiver of Project Review.

What this means for you:

- Longer closing timelines. Full Reviews require more documentation from the HOA. If the association is slow to respond (many are), expect delays.

- More financial scrutiny. Lenders will now examine the HOA's insurance coverage, reserve funding, litigation status, and delinquency rates for every transaction. Issues that might have slipped through Limited Review will now surface.

- Start gathering documents early. Don't wait until you're under contract. Ask the HOA management company for the condo questionnaire as soon as you identify a building you're serious about.

What to do: Factor an extra 2-4 weeks into your closing timeline for any condo purchase after August 3. Ask your lender what documents they'll need from the HOA and start requesting them immediately.

50% Investor Concentration Limit Retired

Buildings previously blocked by the investor-owner cap can now qualify for conventional financing again.

Effective date: Immediate

Good news for buyers interested in urban high-rises and mixed-use buildings. Both agencies have eliminated the rule that made condos non-warrantable if more than 50% of units were investor-owned (non-owner-occupied).

Many downtown buildings in cities like Miami, New York, Chicago, and Las Vegas were effectively cut off from conventional financing because of this rule. That's changing now.

But there's a catch. Individual lenders can still apply their own overlays. Just because Fannie and Freddie dropped the limit doesn't mean your specific lender will approve the loan. Some banks and credit unions will continue to impose their own investor concentration thresholds.

What to do: If you're looking at a building that was previously non-warrantable due to investor concentration, confirm with your lender that they follow agency guidelines without additional overlays. Get this in writing before you commit.

Small Condo Waiver Expanded to 10 Units

Condos with up to 10 units can now qualify for a Waiver of Project Review, simplifying financing for small buildings.

Effective date: Immediate

If you're buying in a small condo building, this is welcome news. The Waiver of Project Review previously applied only to very small projects. Now it covers buildings with up to 10 units.

This means less paperwork, faster closings, and fewer documentation headaches for small condo purchases. The waiver bypasses much of the Full Review process, so the HOA's financial details get less scrutiny.

For small building buyers, this offsets some of the friction created by eliminating Limited Review. But keep in mind: less lender scrutiny also means less protection for you. Consider running your own due diligence on the HOA's finances even if your lender doesn't require it.

What to do: If your building has 10 or fewer units, ask your lender if you qualify for the Waiver of Project Review. But still review the HOA's reserve study and budget yourself. Lender approval doesn't mean the building is financially healthy.

Reserve Studies Must Follow the Highest Recommended Funding Level

Baseline or threshold funding levels are no longer accepted. The reserve study must recommend and follow full funding.

Effective date: August 3, 2026

This is a technical change with big financial implications. Reserve study companies typically provide multiple funding scenarios: baseline (bare minimum), threshold (moderate), and full funding (recommended). Many HOAs have been using the lowest option to keep dues down.

That's over. Both Fannie and Freddie now require the reserve study to reflect the highest recommended funding level. The study must also be completed within the last 36 months.

What this means:

- HOAs using baseline funding will need to increase contributions. This translates directly to higher monthly assessments.

- Outdated reserve studies won't pass review. If the building's study is more than 3 years old, the lender will flag it.

- The reserve study becomes the single most important document in your due diligence. It tells you whether the building is funded to handle major repairs without special assessments.

What to do: Request the reserve study and check two things. First, when was it completed? If it's older than 36 months, that's a problem. Second, which funding level does it use? If it says "baseline" or "threshold," the HOA will need to increase funding before January 2027 to maintain warrantable status.

ACV Insurance Allowed for Roofs Only

HOAs can use Actual Cash Value insurance for roofs, but everything else must carry Replacement Cost coverage.

Effective date: Immediate

Insurance costs have been crushing condo associations, especially in Florida and coastal markets. This change offers a small relief valve. HOAs can now use Actual Cash Value (ACV) insurance for roof coverage instead of the more expensive Replacement Cost Value (RCV) policies.

But there's a hard limit. Every other component of the master insurance policy must remain at replacement cost. If the HOA switches its entire master policy to ACV to save money, the building becomes non-warrantable.

This distinction matters because some boards, under pressure to reduce costs, might make insurance changes that jeopardize financing for every owner in the building.

What to do: Ask for a copy of the HOA's master insurance policy. Verify it carries replacement cost coverage for everything except roofing. If the board is discussing switching to ACV to lower premiums, understand that this could make your unit un-financeable with a conventional mortgage.

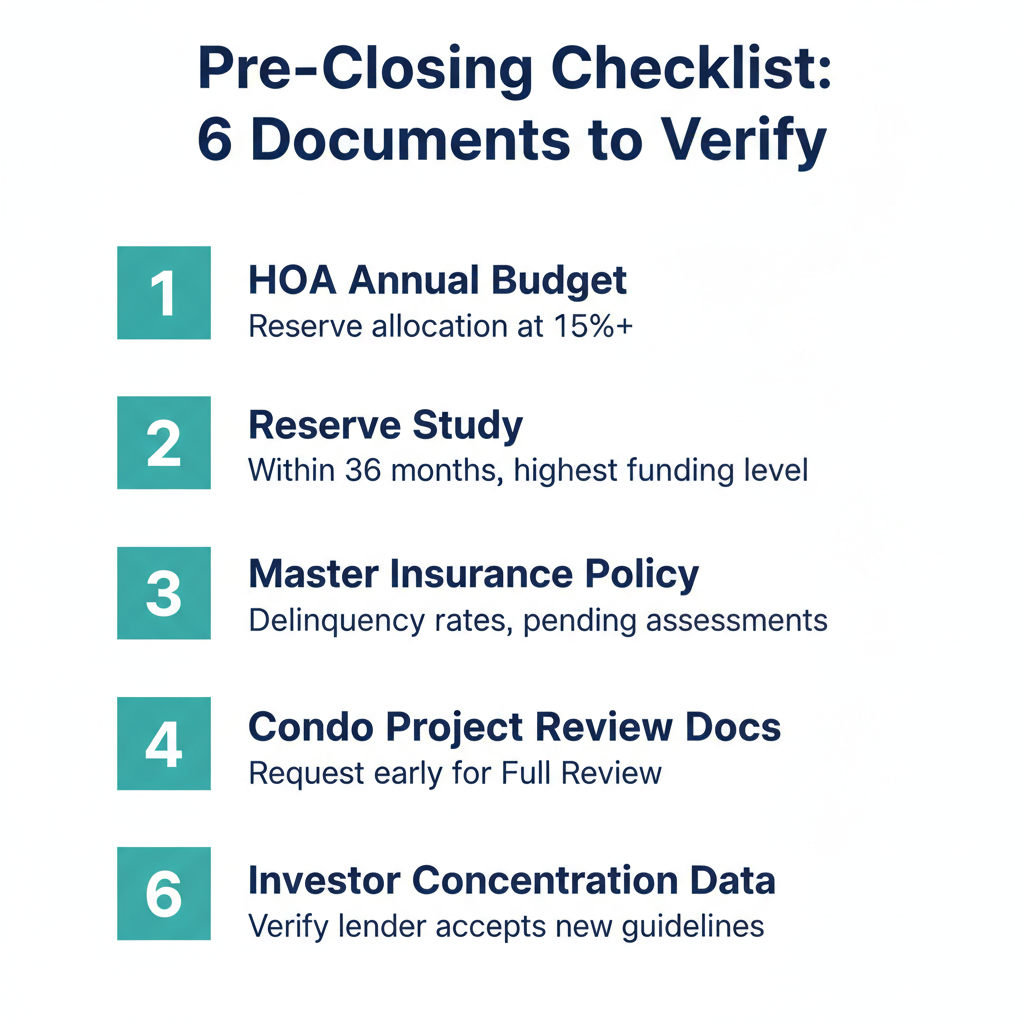

Your Pre-Closing Checklist: 6 Documents to Request

Before you close on any condo in 2026, gather these six documents and verify each item against the new rules.

Before you close on any condo in 2026, gather these documents and verify each item:

- HOA annual budget: Confirm reserve allocation is at or above 15% (or has a plan to reach it by January 2027)

- Reserve study: Must be within 36 months and use the highest recommended funding level

- Master insurance policy: Verify replacement cost coverage on everything except roofing

- HOA financial statements: Check delinquency rates and any pending special assessments

- Condo questionnaire: Your lender will need this for Full Review. Start the request early.

- Investor concentration data: If the building had issues before, confirm your lender accepts the new guidelines

Frequently Asked Questions

When do the new Fannie Mae and Freddie Mac condo rules take effect?

The changes have three effective dates. The investor concentration limit removal and ACV roof insurance changes are effective immediately (March 18, 2026). The elimination of Limited Review and reserve study funding requirements take effect August 3, 2026. The reserve allocation increase from 10% to 15% takes effect January 4, 2027.

Will these changes make it harder to get a condo mortgage?

For some buildings, yes. Eliminating Limited Review means more documentation and scrutiny for every condo purchase. Buildings with low reserve funding or outdated reserve studies may temporarily lose warrantable status. However, removing the investor concentration limit opens up financing for many urban buildings that were previously blocked.

How will the 15% reserve requirement affect my HOA dues?

If your HOA currently allocates less than 15% of its budget to reserves, the board will need to increase contributions. The exact impact depends on your building's current allocation and budget size. An association moving from 10% to 15% could see a meaningful bump in monthly dues.

What happens if my condo building becomes non-warrantable?

If a building loses warrantable status, conventional mortgages (backed by Fannie Mae or Freddie Mac) are no longer available for units in that building. Buyers would need to use portfolio loans, which typically carry higher interest rates and larger down payment requirements. This also affects resale values since the buyer pool shrinks significantly. Learn more about non-warrantable condos →

Can I still close on a condo purchase that's already in progress?

Yes. Transactions already in progress before the effective dates can generally close under the existing rules. But if your closing extends beyond August 3, 2026, your lender may require a Full Review instead of Limited Review. Talk to your loan officer now about which standards will apply to your timeline.

Don't Go In Blind. Check Your HOA Documents Now.

Start with the reserve study. It's the single document that tells you whether the building can handle what's coming. Upload it for free analysis of percent funded, annual budget allocation, and components at end of useful life. No signup required. Based on our analysis of 1,900+ HOA documents, the patterns in that one document predict most of the financial surprises buyers face after closing.

Related Articles

Sources & References

- Lender Letter LL-2026-03 (Fannie Mae. Condo project standards and insurance requirements)

- Bulletin 2026-C (Freddie Mac. Condominium project review updates)

- Campbell Property Management Analysis (Impact analysis for condo associations and homeowners)

- MBA Statement (Mortgage Bankers Association on insurance affordability and eligibility changes)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. HOA documents, reserve funding requirements, and lender criteria vary significantly by state, lender, and association. Consult a qualified professional for guidance specific to your situation.