Your condo mortgage doesn't just depend on your credit score and income. Lenders review the HOA's financial health before approving your loan. If the association fails on reserves, delinquency, insurance, or litigation, your mortgage gets denied. Not because of you. Because of the building.

You found the condo. Offer accepted. Pre-approval in hand. Then your lender comes back and says the building doesn't qualify. The HOA has a problem in its documents, and your mortgage is denied.

This happens more often than most buyers realize. Lenders don't just underwrite you. They underwrite the entire condo project. Fannie Mae and Freddie Mac set specific requirements for HOA finances, insurance, and governance. If the association doesn't meet them, the building is classified as non-warrantable. And non-warrantable means no conventional mortgage.

The worst part? You typically don't find out until you're deep into the transaction. By then you've spent money on inspections, appraisals, and weeks of your time. This guide shows you exactly what lenders look for in HOA documents so you can check before you make an offer.

What Does "Warrantable" Mean and Why Should You Care?

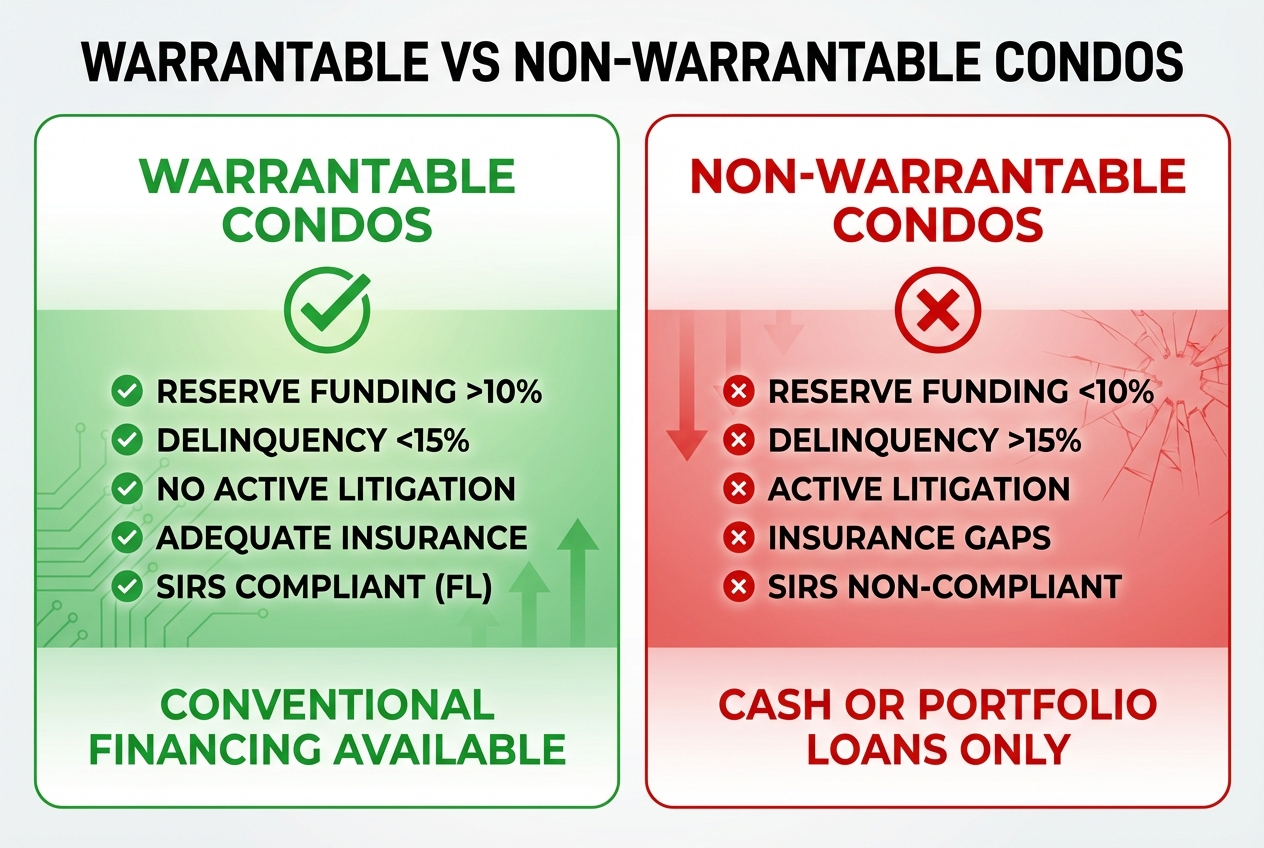

A warrantable condo meets Fannie Mae and Freddie Mac standards for financial health, allowing conventional mortgage financing.

When you apply for a conventional mortgage on a condo, your lender doesn't keep the loan. They sell it to Fannie Mae or Freddie Mac on the secondary market. But these agencies will only buy loans on condos that meet their standards. A condo that meets those standards is called "warrantable."

Think of it like a home inspection, but for the HOA itself. The lender reviews the association's budget, reserves, insurance, litigation status, and ownership mix. Fail on any single requirement, and the building is non-warrantable.

This review happens through a process called Full Review. The lender sends a condo project questionnaire to the HOA management company, which returns financial documents, insurance certificates, and governance details. As of August 3, 2026, every condo purchase with a conventional mortgage requires Full Review. The old Limited Review shortcut has been eliminated.

6 Things in HOA Documents That Kill Condo Financing

Reserve funding, delinquency rates, owner-occupancy, insurance coverage, litigation, and commercial space. Fail one and conventional financing is off the table.

1. Reserve Funding Below the Minimum

The rule: The HOA must allocate at least 10% of its annual operating budget to reserve funds for capital expenditures and deferred maintenance (Fannie Mae Selling Guide B4-2.2-02). This minimum increases to 15% on January 4, 2027, per Lender Letter LL-2026-03.

Where to find it: The HOA's annual budget. Look for a line item labeled "reserve contributions" or "replacement fund." Divide it by the total operating budget. If the result is below 10% (or 15% after January 2027), that's a financing blocker.

Exception: If the association is fully funded per its reserve study (meaning reserves equal 100% of projected needs), the percentage-of-budget minimum does not apply. But few associations hit that mark. Based on our analysis of 1,900+ HOA documents, the majority fall well below full funding.

2. Delinquency Rate Above 15%

The rule: No more than 15% of units can be 60 or more days delinquent on HOA assessments (Fannie Mae Selling Guide B4-2.2-02, Freddie Mac Guide 5701.5).

Where to find it: The HOA's financial statements or the condo questionnaire. Look for an "accounts receivable aging" report. If 15% or more of units are behind on dues, the building fails. This also applies to FHA and VA loans.

Why it matters beyond financing: High delinquency means the HOA is collecting less revenue than it budgeted. That shortfall gets covered by the owners who do pay, either through higher dues or deferred maintenance. Both are bad for you.

3. Owner-Occupancy Below 50%

The rule: At least 50% of units must be owner-occupied. This applies to Fannie Mae, Freddie Mac, FHA, and VA loans (Fannie Mae B4-2.2-02, HUD Handbook 4000.1).

Where to find it: The condo questionnaire or HOA management report. Buildings with high investor concentrations (vacation rentals, Airbnb-heavy buildings, student housing) often fail this test.

Recent change: Fannie Mae and Freddie Mac eliminated the 50% investor concentration limit in March 2026. But the 50% owner-occupancy requirement remains. The distinction: the old rule blocked buildings where one or a few entities owned many units as investments. The owner-occupancy rule counts all non-owner-occupied units regardless of who owns them.

4. Inadequate Insurance Coverage

The rule: The HOA's master insurance policy must carry replacement cost coverage equal to 100% of the estimated replacement cost of the project (Fannie Mae Selling Guide B7-3-03). Associations with more than 20 units must also carry a fidelity bond (Fannie Mae B7-4-02) covering at least three months of aggregate assessments.

Where to find it: The HOA's insurance certificate and master policy declarations page. Verify the coverage type says "replacement cost," not "actual cash value." As of March 2026, ACV coverage is permitted for roofs only.

The insurance squeeze: Rising insurance costs have pushed some HOA boards to downgrade coverage to save money. If the board switches the master policy from replacement cost to actual cash value, every unit in the building becomes non-warrantable. A board decision to cut costs could kill your financing.

5. Pending Litigation Against the HOA

The rule: The project is ineligible if the HOA is a party to pending litigation related to safety, structural soundness, habitability, or functional use of the property (Fannie Mae Selling Guide B4-2.1-03). Minor disputes like neighbor complaints or noise ordinance issues are excluded.

Where to find it: The condo questionnaire asks about litigation directly. HOA meeting minutes often reveal pending or threatened lawsuits before they show up on questionnaires. Construction defect lawsuits are the most common financing killer in this category.

6. Too Much Commercial Space

The rule: No more than 35% of total floor area can be commercial or non-residential space for both Fannie Mae (Selling Guide B4-2.1-03) and Freddie Mac (Guide 5701.5). FHA also allows up to 35%, with exceptions to 49% with additional documentation.

Where to find it: The condo declaration or offering plan. Mixed-use buildings with ground-floor retail are common in urban markets. If the commercial percentage exceeds the limit, the building fails review. Since your lender chooses which agency to sell to, this can surprise you.

Conventional vs FHA vs VA: Same Documents, Different Rules

FHA, VA, and conventional loans all review HOA documents but apply different thresholds. FHA requires project approval. VA requires full project certification with no spot approvals.

| Requirement | Conventional (Fannie/Freddie) | FHA | VA |

|---|---|---|---|

| Reserve funding | 10% of budget (15% after Jan 2027) | 10% of budget (20% if <50% owner-occupied) | Adequate reserves required |

| Delinquency cap | 15% of units (60+ days) | 15% of units (60+ days) | 15% of units |

| Owner-occupancy | 50% minimum | 50% (can go to 35% with documentation) | 50% minimum |

| Commercial space | 35% (both agencies) | 35% (up to 49% with exceptions) | Varies by project |

| Approval type | Full Review (per transaction) | Project approval or Single Unit Approval | Full project approval only (no spot approvals) |

| Approval duration | Reviewed each transaction | 3 years (must recertify) | Must be on VA-approved list |

FHA Single Unit Approval (SUA) is a backup option if the building isn't on the FHA-approved project list. Your lender can approve the individual unit if the building still meets the basic requirements (50% occupancy, adequate reserves, insurance). This works for existing projects only, not new construction.

VA has no spot approval option. The entire project must be on the VA-approved condo list. If it's not there, VA financing is not available for that building. Period. Check the list before you start looking.

What Happens When Your Condo Is Non-Warrantable?

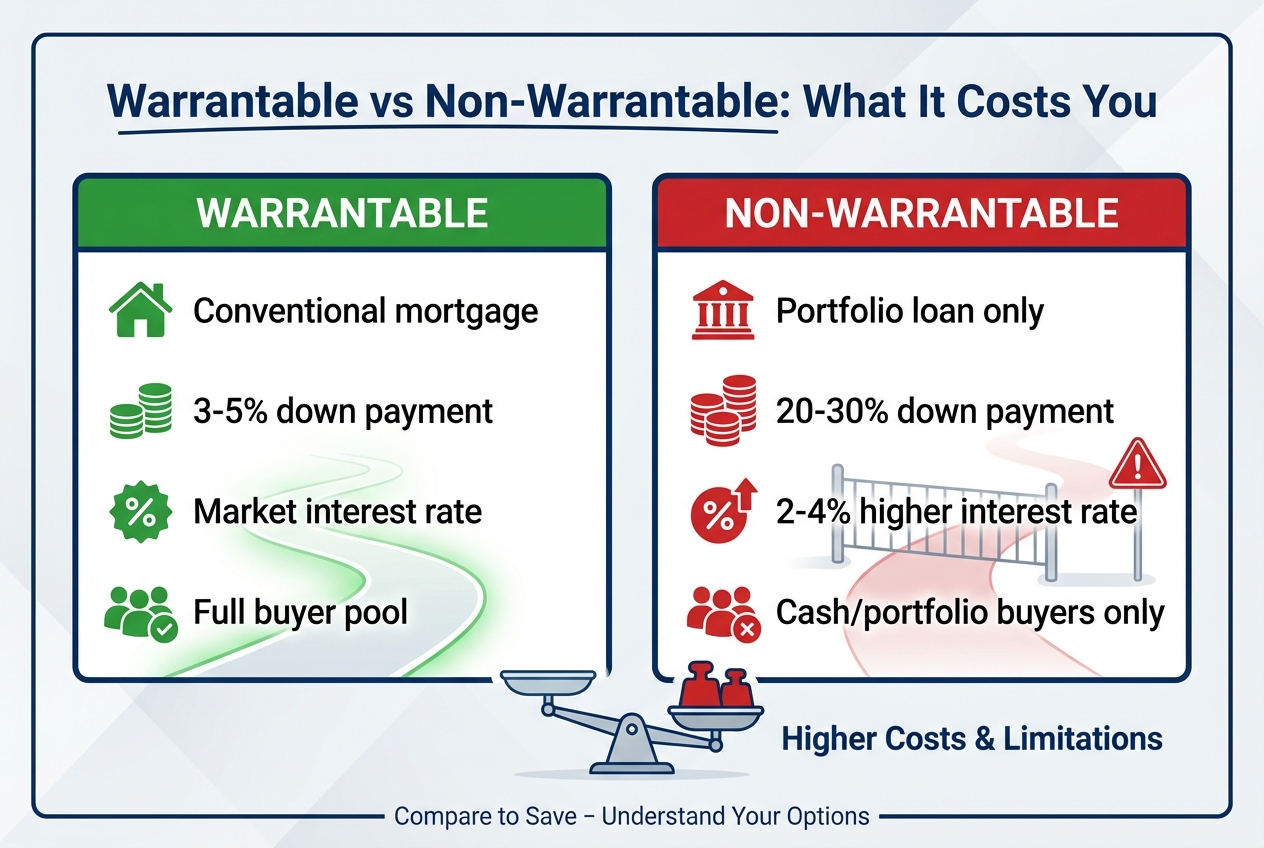

Non-warrantable condos require portfolio loans with higher rates, larger down payments, and a much smaller buyer pool when you sell.

If the building fails warrantability review, conventional financing is off the table. So is FHA and VA in most cases. Your options narrow to:

- Portfolio loans from banks or credit unions that keep the loan on their own books instead of selling to Fannie or Freddie. Rates are typically 2-4 percentage points higher than conventional.

- Larger down payments. Expect 20-30% down instead of the 3-5% available with conventional loans.

- Stricter credit requirements. Higher minimums on credit score and lower debt-to-income ratios.

- Cash purchase. Some buyers in non-warrantable buildings pay cash, but this obviously limits the buyer pool.

The real cost goes beyond the mortgage terms. When you sell, your buyer faces the same restrictions. A non-warrantable building has a significantly smaller buyer pool, which depresses prices. You might buy at a discount, but you sell at a discount too.

How to Check Warrantability Before You Make an Offer

Request the HOA budget, reserve study, insurance certificate, and financial statements before going under contract. Five checks take 10 minutes.

Don't wait for your lender to flag problems during underwriting. By then you've already invested time, money, and emotional energy. Run these checks early:

- Request the HOA budget and calculate the reserve allocation percentage. Divide annual reserve contributions by the total operating budget. Is it above 10%? Will it hit 15% by January 2027?

- Ask for the reserve study. Is it dated within the last 36 months? What funding level does it use? After August 3, 2026, lenders require the highest recommended funding level.

- Check delinquency rates. Ask for the accounts receivable aging report. Count the units 60+ days past due and divide by total units. Over 15% is a deal-breaker.

- Verify insurance coverage. The master policy should specify replacement cost (not actual cash value, except for roofing). Check for a fidelity bond if the building has 20+ units.

- Ask about litigation. The condo questionnaire covers this, but board meeting minutes often reveal pending or threatened lawsuits earlier.

Pro tip: You can ask the listing agent or HOA management company for the condo project questionnaire before going under contract. Some management companies charge $150-300 for this document, but it's the single best source of the information your lender will need.

Frequently Asked Questions

Can a condo that was warrantable become non-warrantable?

Yes. Warrantability is assessed at the time of each loan application. If the HOA's financial situation changes (reserves drop, delinquency rises, insurance lapses), a building can lose warrantable status between transactions. This is why owners should care about HOA governance even after they buy.

How do I find out if a condo is FHA or VA approved?

For FHA, check HUD's Condominium Project Approval search. For VA, check the VA Condo Lookup. If the building isn't listed for FHA, ask your lender about Single Unit Approval (SUA) as a backup option. VA has no equivalent. The building must be on the list.

What is a condo project questionnaire?

A standardized form that HOA management companies fill out for lenders during the Full Review process. It covers reserve funding, delinquency rates, insurance, litigation, owner vs. investor occupancy, commercial space, and other warrantability factors. The joint form is known as Fannie Mae Form 1076 / Freddie Mac Form 476.

My lender says the building is non-warrantable. Can I still buy?

Yes, but your financing options are limited. You'll need a portfolio loan (higher rates, bigger down payment) or a cash purchase. Some credit unions specialize in non-warrantable condo financing. Shop around, but factor the higher cost into your budget. Also ask why the building failed. If it's a fixable issue (the HOA is raising reserves or resolving litigation), you may be able to wait for the issue to clear.

Do the new 2026 Fannie/Freddie rules make it harder to finance a condo?

For some buildings, yes. The reserve minimum increases from 10% to 15% of the operating budget by January 2027, and all transactions now require Full Review (no more Limited Review). Buildings that were borderline will face more scrutiny. But the elimination of the 50% investor concentration limit opens up financing for many urban buildings that were previously blocked. Full breakdown of the 2026 changes →

Check Your HOA Documents Before the Lender Does

Upload your CC&Rs or reserve study for free analysis. See reserve funding levels, rental restrictions, and red flags in minutes instead of hours. No signup required. Based on our analysis of 1,900+ HOA documents, the issues that kill financing are almost always visible in these two documents.

Related Articles

Sources & References

- Fannie Mae Selling Guide B4-2.2-02 (Full Review process and warrantability requirements)

- Fannie Mae Selling Guide B4-2.1-03 (Ineligible project characteristics)

- Lender Letter LL-2026-03 (Fannie Mae. March 2026 condo project and insurance updates)

- Freddie Mac Guide 5701.5 (Condo project eligibility requirements)

- VA Condo Lookup (VA-approved condo project database)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. Warrantability requirements, loan programs, and lender criteria vary by state, agency, and individual lender. Individual lenders may apply overlays that are more restrictive than agency guidelines. Consult a qualified mortgage professional for guidance specific to your situation.