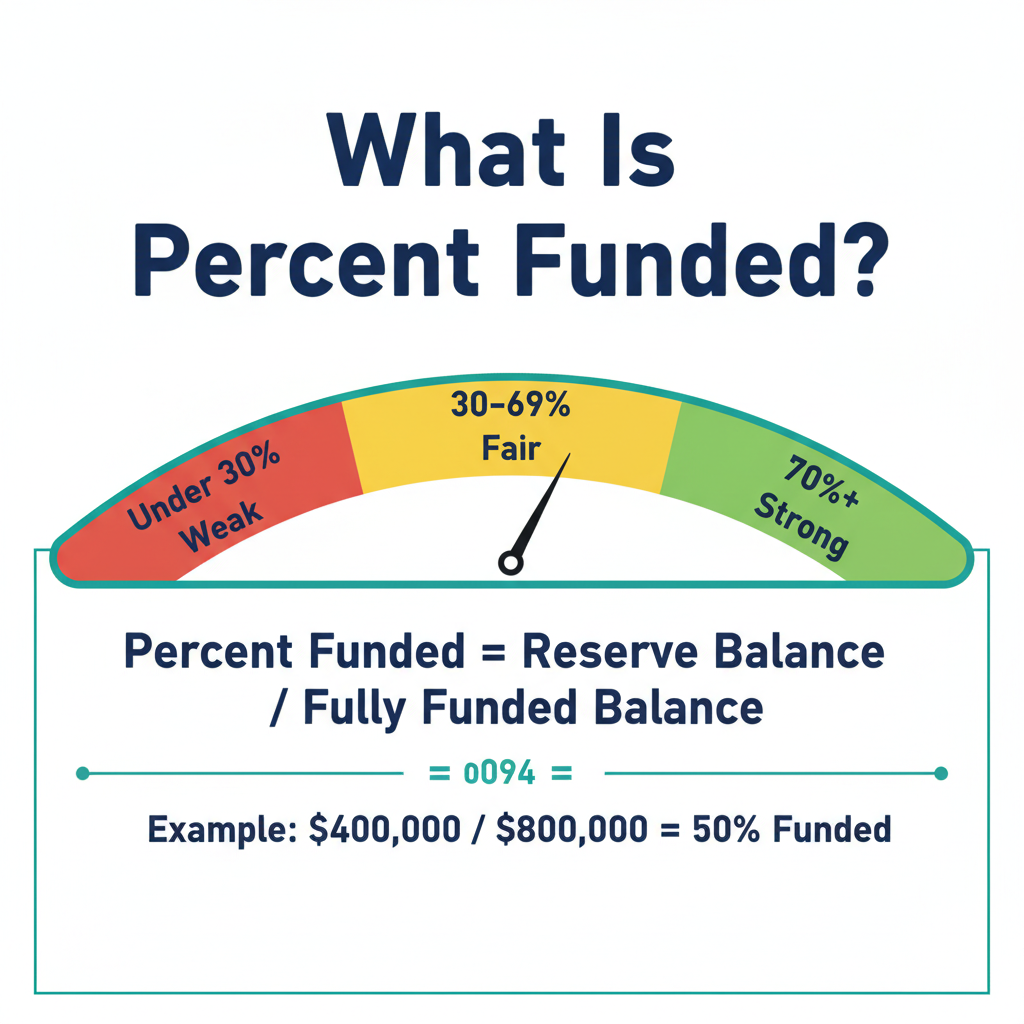

Percent funded compares your HOA's current reserve balance to what it should have saved based on the age and condition of building components. 70% or higher is considered strong. Below 30% is a red flag for special assessment risk.

Every HOA is supposed to save money over time to pay for major repairs. Roofs, elevators, parking structures, plumbing. These components wear out on a schedule, and the reserve fund is where the money comes from. Percent funded tells you how much of that money the HOA has actually saved compared to how much it should have by now.

It is the single most important number in a reserve study. If you are buying a condo or townhome, this number tells you whether the building is financially prepared for future repairs or whether a special assessment is likely coming.

How Percent Funded Is Calculated

Percent funded is the ratio of the HOA's current reserve balance to its fully funded balance, expressed as a percentage.

The formula is straightforward:

Percent Funded = (Current Reserve Balance ÷ Fully Funded Balance) × 100

The "fully funded balance" is what the reserve account should hold right now based on the age and expected replacement cost of every component.

Here is a worked example. Say your building's reserve study shows a current balance of $400,000. The fully funded balance (the ideal amount based on component aging) is $800,000. That puts you at 50% funded. The building has saved half of what it should have by this point.

A reserve study professional calculates the fully funded balance by adding up the depreciated replacement cost of every component the HOA is responsible for. The number changes each year as components age and costs adjust.

What the Numbers Mean

Industry benchmarks group percent funded into three risk bands: strong (70%+), fair (30-69%), and weak (under 30%).

Strong

Low special assessment risk. The HOA is keeping pace with component aging. Lenders view this favorably.

Fair

Monitor closely. The reserve fund has gaps that may require dues increases or targeted assessments if major repairs come due.

Weak

High risk of special assessments. The HOA has saved less than a third of what it needs. Large unexpected costs will likely be passed directly to owners.

Based on our analysis of 1,900+ HOA documents, buildings in the "weak" category are significantly more likely to have a history of special assessments. The pattern is consistent: deferred contributions lead to deferred maintenance, which eventually leads to emergency costs passed on to owners.

These bands are widely used in the reserve study industry and by lenders evaluating condo project eligibility. They are not regulatory thresholds, but they are a practical shorthand for financial health.

Why Percent Funded Matters When Buying a Condo

Percent funded affects mortgage eligibility, predicts special assessments, and impacts your resale value.

Lenders care about this number. Fannie Mae and Freddie Mac evaluate HOA reserve health as part of their condo project approval process. Buildings with very low reserves can be classified as non-warrantable, which means conventional mortgage financing is not available. That shrinks the buyer pool and puts downward pressure on prices.

Special assessments are the other risk. When a major component fails and the reserves are not there to cover it, the board levies a special assessment. These can range from a few thousand dollars to $50,000 or more per unit depending on the building and the repair. A low percent funded number is the clearest early warning sign.

Starting January 2027, Fannie Mae and Freddie Mac will require HOAs to allocate at least 15% of their annual operating budget to reserves. This is a tighter standard than the current 10% requirement and will affect buildings that are already underfunded. Read more in our Fannie/Freddie condo rules guide.

Where to Find Percent Funded in Your Reserve Study

Look for percent funded on the first 2-3 pages of the reserve study, typically in the executive summary section.

Most reserve studies list percent funded prominently in the executive summary. It is usually on page 1 or 2, near the current reserve balance and the recommended annual contribution. Some studies label it "funding level" or "reserve fund ratio" instead.

If the number is not obvious, look for the current reserve balance and the "fully funded balance" or "ideal balance." Divide the first by the second and multiply by 100. That gives you percent funded.

Not sure what you are looking at? Upload your reserve study to our free reserve study analysis tool and it will extract percent funded, components at end of useful life, and other key metrics automatically.

Frequently Asked Questions

What is a good percent funded for an HOA?

70% or higher is considered strong by industry standards and reserve study professionals. At that level, the HOA has saved enough to cover most upcoming repairs without special assessments. Some well-managed buildings maintain 80-100% funding. See our detailed percent funded benchmarks for a deeper breakdown.

What happens when percent funded is below 30%?

Below 30% means the HOA has saved less than a third of what it needs. When a major component needs replacement, the money is not there. The board will likely levy a special assessment on all owners to cover the shortfall. These can be substantial. In severe cases, low funding can also affect the building's ability to qualify for conventional financing.

Is 50% percent funded bad?

50% falls in the "fair" range. It is not a crisis, but it warrants scrutiny. The HOA has saved half of what it ideally should have. Check whether the reserve study shows an upward funding trend (contributions increasing to close the gap) or a flat/declining trend. A building at 50% with a strong funding plan is in better shape than one at 50% with no plan to improve.

Does percent funded affect my mortgage?

Yes. Lenders evaluate HOA reserve health when approving condo loans. Fannie Mae and Freddie Mac require a minimum budget allocation to reserves (currently 10%, increasing to 15% in January 2027). Buildings with severely low reserves can be classified as non-warrantable, which disqualifies them from conventional financing. Buyers would then need cash or a portfolio loan with higher rates and larger down payments.

Check Your Building's Percent Funded

Upload your HOA's reserve study and get instant analysis of percent funded, components at end of useful life, and deferred maintenance risks. Free. No signup required.

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. HOA documents, reserve funding requirements, and lender criteria vary significantly by state, lender, and association. Consult a qualified professional for guidance specific to your situation.