In This Guide

Who pays an HOA special assessment at closing depends on your purchase contract and state law. Generally, assessments levied before closing are the seller's responsibility. But in Florida, Hawaii, and Washington, buyers can be jointly liable for unpaid assessments by statute.

You're two weeks from closing on a condo. Everything looks good. Then the title company sends over the estoppel certificate and there it is: a $35,000 special assessment for roof replacement, levied three months ago. The seller hasn't paid it.

Now what? Does the seller pay it off before closing? Do you inherit it? Can you negotiate a credit? The answer depends on your state, your contract, and when the assessment was approved. Get this wrong and you could be writing a five-figure check you didn't budget for.

Here's how special assessments actually work at closing, state by state.

The General Rule: Timing and Contract Language

The purchase contract controls who pays. If the contract is silent, the owner at the time the assessment is levied is generally responsible.

The default principle across most states is straightforward. Assessments approved and billed before closing are the seller's responsibility. Assessments imposed after closing are the buyer's.

But the purchase contract can override this default. Most standard real estate contracts address special assessments directly. If yours doesn't, you're relying on state law defaults, and those vary significantly.

There's an important wrinkle with installment assessments. If a $60,000 assessment is being paid over five years at $1,000 per month, many contracts specify that installments due before closing are the seller's obligation while installments due after closing become the buyer's. Even though the assessment was levied before the sale.

In California, many HOA boards adopt "due on sale" clauses in their governing documents. When present, these clauses make the full remaining assessment balance due upon transfer of title. The seller can't transfer remaining installments to the buyer. Check the CC&Rs for acceleration language before assuming installments will carry over.

State-by-State Guide: Who Pays the Special Assessment?

Three states impose joint liability on buyers by statute. Most others protect buyers through mandatory disclosure documents that cap liability.

Laws vary by state. Here's what you need to know in the states with the most condo activity.

| State | Buyer Jointly Liable? | Key Disclosure Document | Buyer Protection |

|---|---|---|---|

| Florida | Yes | Estoppel certificate | Liability capped at estoppel amount |

| Hawaii | Yes | Board statement | Liability capped at board statement amount |

| Washington | Yes | Resale certificate | 5-day cancellation after receiving certificate |

| California | No | Civil Code 4525 disclosure | Many HOAs have "due on sale" clauses; lien requires recording |

| Texas | No | Resale certificate | Buyer not liable for undisclosed debts |

| Colorado | No | Status letter | Association loses lien if late providing statement |

| Illinois | No | 22.1 letter + Paid Assessment Letter | Standard attorney review period (contractual) |

| Arizona | No | Resale disclosure | Lien extinguished if association misses 10-day deadline |

| Nevada | No | Resale package | Buyer not liable beyond disclosed amounts |

| Virginia | No | Resale certificate | Buyer not liable beyond certificate amounts |

Important: This table summarizes statutory defaults. Your purchase contract can modify these rules. Always read the assessment language in your contract before relying on state defaults.

The Three Joint Liability States: What Buyers Must Know

In Florida, Hawaii, and Washington, the buyer is jointly and severally liable with the seller for unpaid assessments by statute. Estoppel certificates cap this liability.

Florida (FL Stat. 718.116)

Florida has the most aggressive buyer liability rule in the country. Under FL Statute 718.116(1)(a), a buyer is jointly and severally liable with the seller for all unpaid assessments that accrued before title transfer. The association can pursue either party for the debt.

The buyer has the right to recover those amounts from the seller after the fact. But that means hiring a lawyer and chasing the money. Not ideal.

The protection: Florida's estoppel certificate. The association must issue one within 10 business days of a written request. It must itemize all assessments, special assessments, and amounts owed. The association waives the right to collect any amount in excess of what the estoppel states from anyone who relies on it in good faith. The estoppel is valid for 30 days. The statutory fee is currently capped at $299 (adjusted for inflation by the DBPR in 2022).

Bottom line: In Florida, never close without a current estoppel certificate. It's your liability cap.

Hawaii (HRS 514B-144)

Hawaii follows a similar pattern. Under HRS 514B-144(f), the buyer is jointly and severally liable with the seller for all unpaid assessments up to the time of conveyance. But the buyer's liability is capped at the amount stated in a written statement from the board.

Hawaii also has a lien for assessments under HRS 514B-146. The lien is subordinate to previously recorded mortgages for most amounts. But six months of unpaid regular monthly assessments get super-priority status that takes precedence even over first mortgages. Real property tax liens always come first.

Washington (RCW 64.34.364 / RCW 64.90.485)

Washington imposes joint and several liability on the buyer for the seller's unpaid assessments. The buyer can pursue the seller for reimbursement, but the association can come after either party.

Washington buyers get a 5-day cancellation right after receiving the resale certificate. If no current reserve study exists, the association must disclose that "insufficient reserves may require you to pay on demand as a special assessment your share of common expenses." The resale certificate fee is capped at $275.

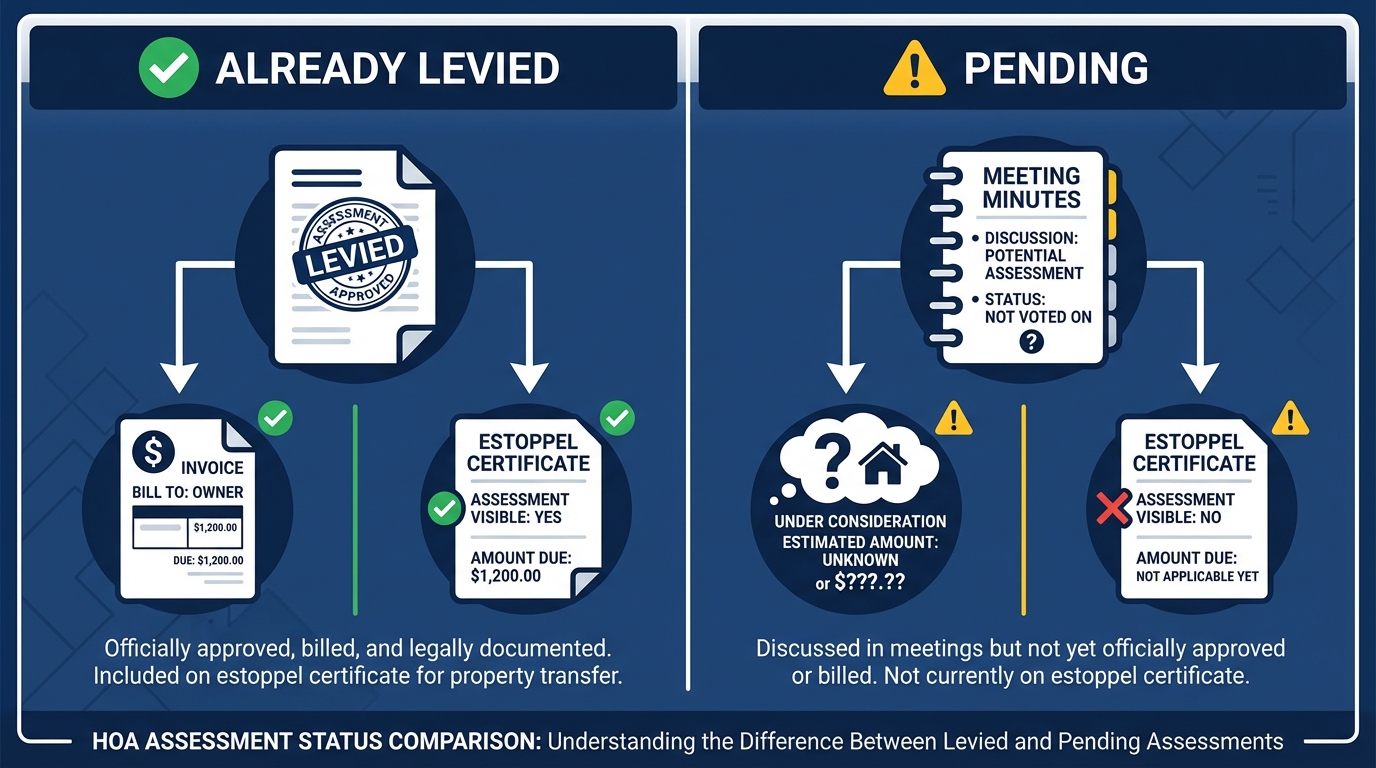

Already Levied vs. Pending: The Gray Area That Causes Disputes

Levied assessments show up on estoppel certificates and are allocable. Pending assessments discussed in board meetings but not yet approved are the gray area buyers miss.

Already-Levied Assessments

These are formally approved by the board and billed to owners. They show up on estoppel certificates and resale disclosures. Allocation is straightforward: whoever owned the unit when the assessment was levied is responsible.

If the assessment is being paid in installments, the standard approach in most states is that the seller pays installments due before closing and the buyer pays installments due after. In California, this exception doesn't apply. The full remaining balance becomes due at sale.

Pending Assessments (Not Yet Approved)

This is where buyers get blindsided. A special assessment that the board has been discussing for six months but hasn't voted on yet won't appear on the estoppel certificate. The seller isn't legally required to pay for something that hasn't been levied.

But the warning signs are in the board meeting minutes. If the minutes mention "deferred maintenance," "engineering report," "reserve funding shortfall," or "assessment options," an assessment may be weeks away from a vote. By the time it's approved, you're the owner and you're paying it.

Always request the last 12 months of board meeting minutes before closing. This is the only way to catch pending assessments that haven't hit the estoppel yet.

How to Negotiate Special Assessments at Closing

Six negotiation strategies: seller pays in full, closing credit, price reduction, cost split, escrow holdback, or buyer assumes for a lower price.

A special assessment doesn't have to kill a deal. Here are six ways buyers and sellers typically handle it.

- Seller pays in full before closing. The cleanest option. The assessment is cleared, the buyer takes clean title, and there's no post-closing liability.

- Closing credit. The seller gives the buyer a dollar-for-dollar credit at closing. The buyer manages the payment directly with the HOA. Works well when the buyer wants control over the payment timeline.

- Price reduction. Lower the purchase price by the assessment amount. Same economic result as a credit, but affects comparable sales data for the building. Some sellers prefer this to avoid showing an assessment on the closing statement.

- Split the cost. Common when the assessment was levied shortly before listing. Both parties share the burden. Often used when the seller argues they "didn't cause the deferred maintenance" and the buyer concedes the building still needs the work done.

- Escrow holdback. When the final assessment amount isn't confirmed, funds are held in escrow until the HOA finalizes the number. Protects both parties when the board has approved the project but hasn't set the per-unit amount.

- Buyer assumes for a lower price. The buyer accepts the assessment in exchange for a significant price reduction. This works when the buyer has cash reserves and wants a deeper discount. The risk is that the final assessment could exceed the estimate.

The Estoppel Certificate: Your Most Important Closing Document

The estoppel certificate (or resale certificate) reveals all current assessments and caps buyer liability in many states. Never close without one.

Different states call it different things: estoppel certificate in Florida, resale certificate in Virginia and Nevada, 22.1 letter in Illinois, status letter in Colorado. Whatever the name, this document serves the same purpose: it tells you exactly what the seller owes the HOA.

What a good estoppel reveals:

- Current regular assessment amount and payment status

- Any unpaid or delinquent assessments from the seller

- Special assessments that have been levied (paid or not)

- Special assessments approved but not yet due

- Fines, penalties, interest, and collection costs

- Pending litigation involving the association

- Reserve fund balance

In several states, the association is legally bound by what it puts in the estoppel. Florida, Virginia, Nevada, and Texas all protect buyers from amounts not disclosed. In Arizona and Colorado, the association can actually lose its lien entirely if it fails to provide the statement within the statutory deadline.

| State | Document Name | Response Deadline | Fee Cap |

|---|---|---|---|

| Florida | Estoppel certificate | 10 business days | $299 |

| Arizona | Resale disclosure | 10 days | $400 |

| Washington | Resale certificate | 10 days | $275 |

| Illinois | 22.1 letter + PAL | 10 business days | ~$100 (typical) |

| Colorado | Status letter | 14 calendar days | Varies |

| Texas | Resale certificate | 10 business days | Varies |

| Nevada | Resale package | 10 calendar days | Varies |

| Virginia | Resale certificate | Per contract | Varies |

| California | Civil Code 4525 disclosure | 10 days | Varies |

Real Numbers: What Special Assessments Look Like in 2026

Special assessments in 2024-2026 range from $8,700 for elevator replacement to $400,000 for full building remediation. Florida leads the country.

These aren't hypothetical numbers. These are real assessments from real buildings in the past two years.

| Building / Location | Assessment Per Unit | Reason |

|---|---|---|

| Mediterranean Village, Aventura FL | Up to $400,000 | Full building remediation |

| Cricket Club, North Miami FL | Up to $134,000 | Structural repairs |

| Regency Gardens, Orlando FL | Up to $22,105 | Deferred maintenance |

| Elevator building (multi-unit) | $8,700 | Elevator replacement |

In our analysis of 1,900+ HOA documents, special assessment language is one of the most common red flags. Florida leads the country, but assessments of $10,000 to $50,000 per unit are increasingly common in California, Illinois, and coastal markets where aging buildings face deferred maintenance.

5 Steps to Protect Yourself Before Closing

Request the estoppel, read meeting minutes, check the reserve study, review your contract language, and get assessment language in writing before closing.

1. Request the Estoppel Certificate Early

Don't wait until the last week before closing. Request the estoppel (or your state's equivalent) as soon as you're under contract. Some associations take the full statutory deadline to respond. In Florida, that's 10 business days. You need time to review it and negotiate if surprises come up.

2. Read the Last 12 Months of Board Meeting Minutes

The estoppel only shows what's been levied. Meeting minutes reveal what's being discussed. If the board is getting bids for roof replacement or debating a special assessment vote, you need to know before closing. Upload the minutes to GoverningDocs to flag assessment-related language automatically.

3. Check the Reserve Study

A building with reserves below 30% funded is significantly more likely to levy a special assessment. Upload the reserve study to our free analyzer to see percent funded, deferred maintenance items, and major expenses coming in the next five years.

4. Review Your Contract's Assessment Language

Check what your purchase contract says about special assessments. Does it address who pays for assessments levied before closing? What about installment assessments? If the contract is silent, you may be relying on state defaults that may not be in your favor.

5. Get Assessment Commitments in Writing

If the seller agrees to pay a special assessment, make sure it's documented in the contract or an addendum. Verbal agreements don't survive closing. If there's a pending assessment that hasn't been levied yet, consider an escrow holdback or a contractual credit tied to a dollar cap.

How to Check Your Building's Assessment Risk

Every data point in this article comes from HOA documents: estoppel certificates, reserve studies, board meeting minutes, and CC&Rs. These documents tell you whether an assessment has been levied, whether one is being discussed, and whether the building's financial health makes one likely.

Upload your CC&Rs or reserve study to GoverningDocs. The tool extracts assessment language, reserve funding levels, and deferred maintenance items. Free. No signup.

In a market where special assessments are surging, knowing who pays at closing is only half the equation. Knowing whether one is coming is the other half.

Frequently Asked Questions

Who is responsible for a special assessment at closing, the buyer or seller?

It depends on your purchase contract and state law. In most states, the seller is responsible for assessments levied before closing and the buyer is responsible for assessments levied after. But in Florida, Hawaii, and Washington, buyers are jointly and severally liable with sellers for unpaid assessments by statute. Always check both your contract and the estoppel certificate.

What happens if a special assessment is levied after I sign the contract but before closing?

This depends on your contract language. Most standard contracts assign the assessment to whoever owns the property when the assessment is approved. If the assessment is levied after you sign but before you close, the seller typically still pays because they hold title. But some contracts shift this risk. Read the assessment clause carefully.

Can I back out of a deal because of a special assessment?

Possibly. Several states give buyers cancellation rights after receiving HOA disclosure documents. Washington gives 5 days after receiving the resale certificate. Your contract may also include a due diligence or inspection contingency that covers HOA document review.

What is an estoppel certificate and why do I need one?

An estoppel certificate is a document from the HOA that states all amounts owed by the seller, including regular assessments, special assessments, fines, and fees. In many states, the association is legally bound by the amounts listed. The certificate caps your potential liability and protects you from undisclosed debts. Never close on a condo or HOA property without one.

Check Your HOA Documents Before Closing

Upload your CC&Rs or reserve study for free analysis. See special assessment language, reserve funding levels, deferred maintenance items, and other red flags in minutes. No signup required. Based on our analysis of 1,900+ HOA documents.

Related Articles

See how GoverningDocs detects special assessments and financial risks.

See Sample Report →Sources & References

- Florida Statute § 718.116 (Condo assessments; liability; lien and priority; estoppel certificates)

- Hawaii HRS § 514B-144 (Association fiscal matters; joint and several liability)

- Washington RCW 64.34.364 (Condominium Act; lien for assessments)

- California Civil Code § 4525 (Transfer disclosures; seller obligations)

- Texas Property Code Chapter 207 (Disclosure of information by property owners' associations)

- Colorado CRS § 38-33.3-316 (CCIOA; lien for assessments)

- Illinois 765 ILCS 605/22.1 (Condominium Property Act; resale disclosure)

- Arizona ARS § 33-1256 (Condominiums; common expense liens)

- Nevada NRS § 116.4109 (Resales of units; resale package)

- Virginia Resale Disclosure Act (Title 55.1, Ch. 23.1) (Resale certificate requirements)

- ResiClub Analytics (Spiking HOA fees and special assessments in Florida)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. HOA assessment laws, estoppel requirements, and buyer liability rules vary by state and community. Statute citations are current as of March 2026 but may be amended. Consult a qualified real estate attorney for guidance specific to your situation.