A non-warrantable condo can't get conventional financing from Fannie Mae or Freddie Mac. That means fewer buyers, lower offers, and a longer time on market — all because of the building's finances, not your unit.

A thread in r/RealEstate with 117 upvotes captured this well: a NJ realtor described a listing that sat for months because buyers couldn't get financing approved — not because of the unit, but because of the building's financials. An Atlanta condo owner in the same thread described their building's master insurance policy jumping from roughly $80K to $220K annually — a ripple effect from Florida's insurance crisis that repriced risk in markets across the country.

These are anecdotal accounts, but they illustrate a pattern that real estate professionals are seeing more frequently. Most owners don't find out their condo is non-warrantable until a buyer's lender rejects the deal mid-contract.

What "Non-Warrantable" Actually Means

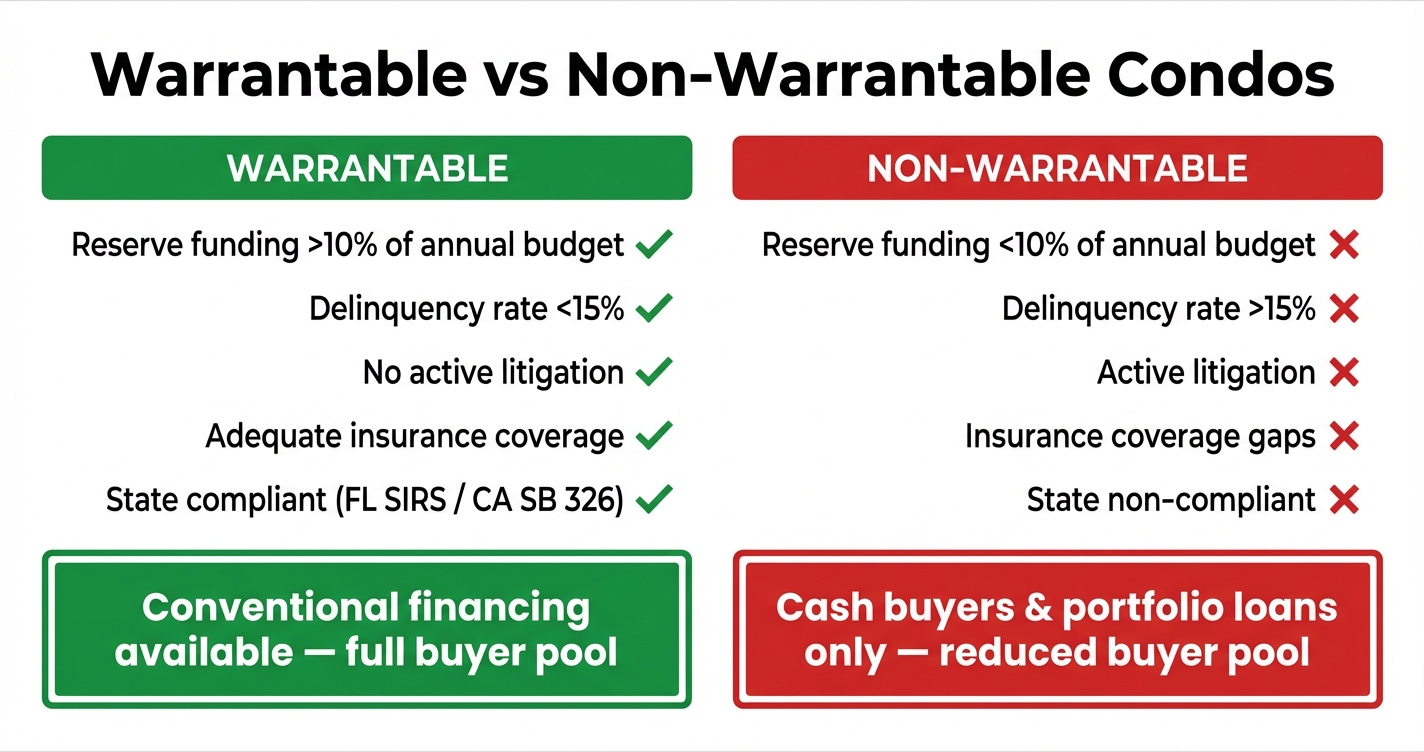

A condo is "warrantable" when Fannie Mae or Freddie Mac will back loans on it. Non-warrantable means they won't — and conventional lenders can't sell those loans on the secondary market.

When you buy a condo, your lender doesn't just evaluate you. They evaluate the entire building. Fannie Mae and Freddie Mac set eligibility criteria for condo projects — financial stability, insurance coverage, occupancy ratios — because they're the ones backing most conventional mortgages.

If the building fails those criteria, it's classified as non-warrantable. That means:

- No conventional mortgage financing (no 30-year fixed at market rates)

- Buyer pool shrinks to cash buyers and portfolio lenders

- Portfolio loans typically require higher down payments and charge higher interest rates

- Sale prices can drop significantly — because fewer people can qualify to buy

If you're a seller, this hits your bottom line directly. If you're a buyer, it affects your ability to get a loan — and your future resale value.

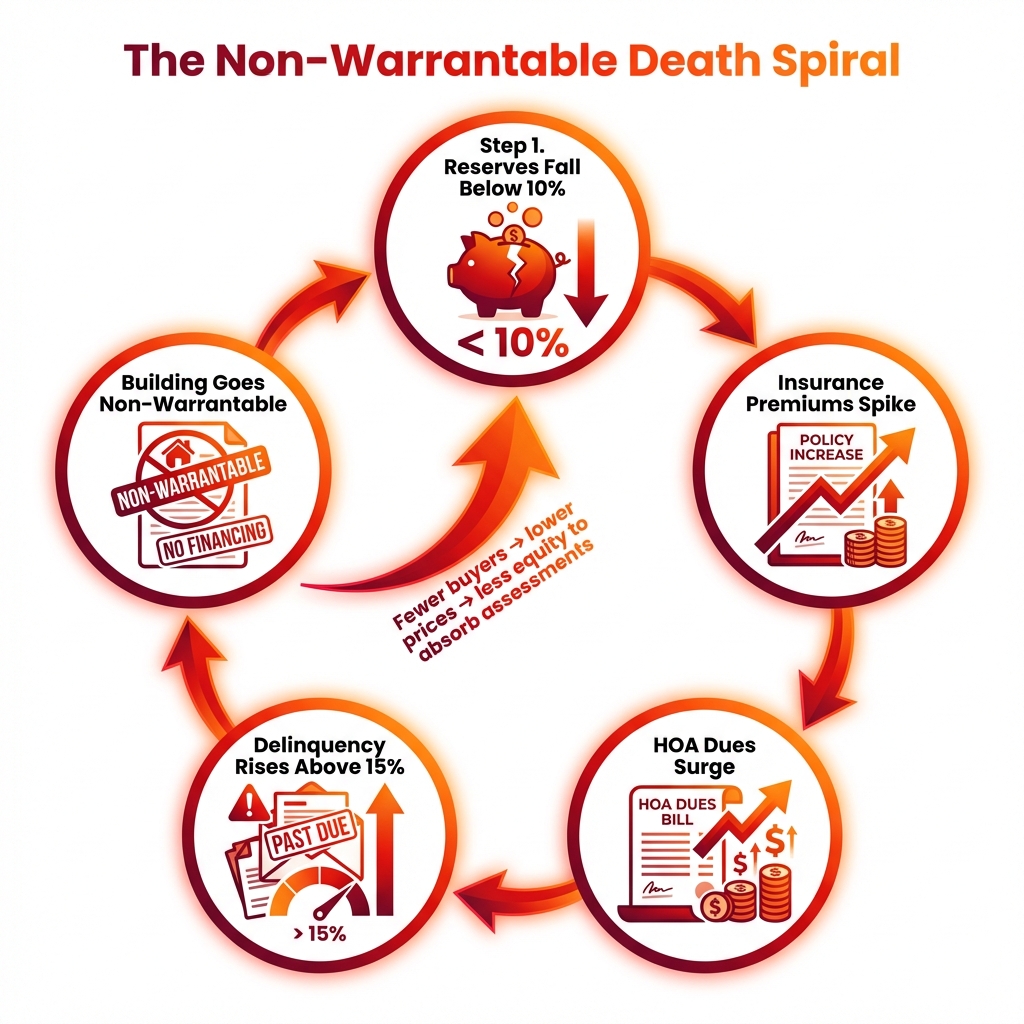

How Buildings Get There: The Death Spiral

Non-warrantability rarely happens overnight. It usually follows a pattern: underfunded reserves lead to deferred maintenance, which drives insurance increases, which pushes delinquencies up — until the building crosses a lender threshold.

Here's the pattern playing out in buildings across the country:

Reserves fall below threshold. Years of waived or underfunded contributions leave the building with less than 10% of its annual operating budget in reserves.

Insurance premiums spike or coverage lapses. Insurers review reserve studies and structural inspection reports when pricing or renewing master policies. Buildings with deferred maintenance or thin reserves are increasingly seeing large premium increases — in some cases more than doubling — as insurers reprice risk following high-profile building failures.

HOA dues rise sharply to cover the insurance increase and deferred maintenance. Some owners can't keep up.

Delinquency climbs above 15%. Once more than 15% of owners are behind on dues, lenders flag the project.

Building goes non-warrantable. Fewer buyers can get loans. Prices drop. Less equity available to absorb special assessments. The cycle tightens.

New Jersey's reserve study legislation is an example of how external factors can surface pre-existing problems quickly. When reserve studies are completed or updated to comply with new state laws, the resulting reports may reveal funding levels that lenders flag during condo project review — creating selling challenges for owners whose buildings were never transparent about their reserve status.

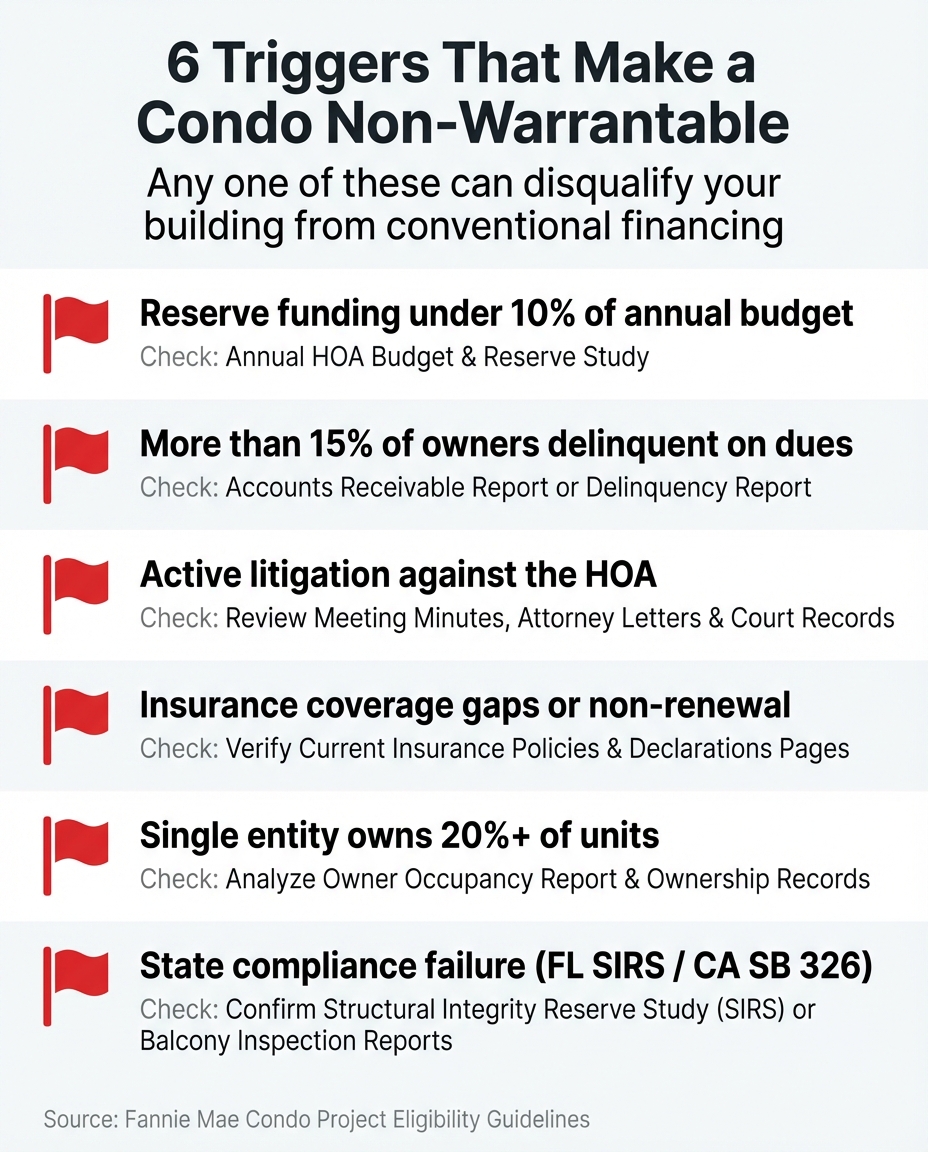

The 6 Triggers Most Owners Miss

Fannie Mae's condo project eligibility rules cover reserve funding, delinquency rates, material litigation, insurance, investor concentration, and state-specific structural compliance. Any one can disqualify a building.

- Reserve funding under 10% of annual budget. Lenders require at least 10% of the HOA's annual operating budget allocated to reserves. This is different from percent funded — a building can be 70% funded but still fail if its annual budget doesn't allocate enough going forward.

- More than 15% of owners delinquent on dues. Lenders see high delinquency as financial instability. One bad year of collections can flip a building.

- Material litigation against the HOA. Not every lawsuit disqualifies a project — routine liability claims covered by the HOA's insurance generally don't. What lenders flag is material litigation: construction defect claims, disputes that could result in large financial judgments, or cases that could materially affect the HOA's financial stability. Your lender will evaluate the nature and scope of any pending litigation.

- Insurance coverage gaps or non-renewal. If the master policy doesn't meet Fannie Mae's coverage minimums, the building fails. Premium spikes that cause coverage reductions are equally disqualifying.

- Single entity owns more than 20% of units. High investor concentration signals rental-heavy buildings. This is a common issue in newer developments.

- State-specific compliance failures. Florida's SIRS non-compliance and California's SB 326 balcony inspection requirements are now lender triggers. Many condo project review checklists have been updated since 2024.

How to Check Your Building Before It's Too Late

Request the reserve study for percent funded, ask management for the delinquency rate, review the insurance certificate for coverage gaps, and check recent board minutes for litigation mentions.

You don't need a lender to tell you there's a problem. These four steps can flag issues before they kill a deal:

Pro Tip: Ask for the Warrantability Check Early

If you're listing (or advising a seller), ask your lender to run a warrantability check on the building before you set a price. It's free, takes a few days, and tells you exactly what buyers will face. Discovering the issue early gives you time to address it or price accordingly.

1. Get the reserve study. Find the percent funded number and the annual budget allocation to reserves. You're looking for both: overall funding level AND the annual contribution rate. Upload your reserve study to GoverningDocs for a free analysis that pulls these numbers automatically.

2. Ask management for the delinquency rate. A simple question: "What percentage of owners are currently past due on dues?" Above 15% is a problem. Most management companies can pull this number from their software in minutes.

3. Review the insurance certificate. Ask for the master policy certificate and check the coverage amount, premium trend over the past 2–3 years, and renewal status. A premium that doubled in two years is worth investigating further.

4. Read recent board minutes. Three to five years of meeting minutes will surface litigation mentions, deferred maintenance discussions, and emergency assessments. See our guide on red flags in HOA meeting minutes.

If Your Building Is Already Non-Warrantable

Non-warrantability isn't permanent. Fix the failing criteria — reserve funding, delinquency, litigation — and the building can regain eligibility. But it takes board action and time.

Your options depend on which trigger caused the problem:

- Reserve funding issue: The path back typically involves updating the reserve study, adopting a funding plan that meets the 10% budget allocation threshold, and demonstrating that plan to lenders. A reserve study professional can document the current status and a credible path to compliance. This takes at minimum a full budget cycle to demonstrate to lenders.

- Delinquency issue: Collections enforcement is the lever here. This takes time and often requires working with HOA counsel on the collection process — it's harder to fix quickly than a reserve funding gap.

- Litigation: If the material litigation settles or is dismissed, lenders can reassess the project's eligibility. Until it's resolved, the uncertainty is what creates the problem for buyers seeking conventional financing.

- If you're selling now: Many real estate professionals recommend getting a lender warrantability check done before listing so pricing reflects the actual buyer pool. Consult a real estate agent or attorney familiar with your state's disclosure requirements — what needs to be disclosed and when varies by location.

Board Members: Get a Reserve Study First

If you suspect a reserve funding problem, a current reserve study is step one. It documents where you stand, what it costs to fix it, and provides a funding plan lenders can review. 33 states now have reserve-related legislation. The CAI tracks which states require studies and funding mandates on their advocacy page.

Key Takeaways

- ✕Non-warrantable = no conventional financing = smaller buyer pool = lower sale prices

- ⚠Any one of 6 triggers can disqualify a building: reserves, delinquency, litigation, insurance, investor concentration, state compliance

- →Check early: reserve study, delinquency rate, insurance certificate, board minutes

- ✓Non-warrantability is fixable — but it takes board action, a funding plan, and time

- →If selling now: get a warrantability check done early and work with a local agent on pricing — the buyer pool is smaller than a comparable warrantable unit

Frequently Asked Questions

What makes a condo non-warrantable?

Fannie Mae and Freddie Mac classify a condo as non-warrantable if the building fails any of their eligibility criteria: reserve funding below 10% of annual budget, more than 15% of owners delinquent on dues, active litigation against the HOA, inadequate insurance coverage, a single entity owning more than 20% of units, or state-specific structural compliance failures (Florida SIRS, California SB 326).

Can you get a mortgage on a non-warrantable condo?

Yes, but not a conventional loan. Non-warrantable condos require cash purchases or portfolio loans. Portfolio loans aren't sold to Fannie Mae or Freddie Mac, so lenders set their own terms — typically higher interest rates, larger down payments (often 25–30%), and stricter qualification requirements. How percent funded affects lender eligibility →

Does non-warrantable status affect my sale price?

It can, yes. Cash buyers and portfolio loan buyers generally expect some discount because their financing costs are higher and the resale pool for their future sale will also be restricted. How much of a discount depends on the local market, the specific issue causing non-warrantability, and how many cash buyers are active in that area. Consult a local real estate professional for pricing guidance specific to your market.

How do I find out if my condo building is non-warrantable?

Ask your lender to run a warrantability check on the building. It's a standard part of condo loan processing and is free. You can also proactively review the four main indicators: reserve study funding levels, delinquency rate, insurance certificate, and board meeting minutes for litigation.

Can a non-warrantable condo become warrantable again?

Yes. Non-warrantability isn't permanent. If the building resolves the failing criteria — increases reserve contributions, reduces delinquency, settles litigation, or restores adequate insurance coverage — lenders can reclassify it as warrantable after a full project review. How to read a reserve study and find percent funded →

Check Your Reserve Study for Financing Red Flags

Upload your HOA's reserve study and get instant analysis of percent funded, annual budget allocation, and components at end of useful life. Free. No signup required.

Analyze Reserve Study →Related Articles

Sources & References

- Condominium Project Eligibility — Fannie Mae (warrantability criteria and reserve budget requirements)

- Reserve Requirements and Funding — State Legislation Tracker — Community Associations Institute (33 states with reserve-related laws)

- What is a Good Percent Funded for an HOA? — GoverningDocs (percent funded benchmarks and lender requirements)

- Florida Condo Crisis 2026: What Buyers Must Know — GoverningDocs (SIRS requirements and reserve funding mandates)

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or real estate advice. HOA documents, reserve funding requirements, and lender criteria vary significantly by state, lender, and association. Consult a qualified professional for guidance specific to your situation.