In This Guide

First-time condo buyers must review CC&Rs for rental restrictions, reserve study funding levels, and special assessments before closing. Don't skip HOA docs.

You found the perfect condo. Great location, within budget, and the monthly HOA fee looks manageable. You sign the contract, close in 30 days, and move in. Four months later, a $12,000 special assessment notice shows up in your mailbox.

This happens more than you'd think. First-time buyers focus on price, location, and layout. The HOA documents are an afterthought. Most people flip through 300+ pages of legalese, understand maybe 10% of it, and sign anyway. The warning signs were there. They just didn't know what to look for.

With more first-time buyers entering the condo market in 2026, understanding HOA documents isn't optional. It's the difference between a smart purchase and an expensive lesson. This guide covers the five things you need to check, the questions to ask your agent, and how to get help when you're short on time.

Why First-Time Buyers Often Choose Condos

Condos are the most affordable entry point into homeownership for many buyers, especially in urban markets.

The math makes sense on paper. Condos are typically 20-40% cheaper than single-family homes in the same area. You get a lower down payment, a smaller mortgage, and someone else handles the roof, the landscaping, and the exterior maintenance.

For buyers in cities like Miami, Seattle, or San Diego, a condo might be the only way to buy in the neighborhood where they work. Less maintenance responsibility. Urban location. Lower purchase price. It checks every box.

But condos come with something single-family homes don't: a homeowners association. And that HOA comes with documents. Lots of them.

The HOA Document Blindspot

Most first-time buyers don't realize HOA documents can reveal deal-breaking problems that don't show up in the listing or the inspection.

Here's how it usually goes. You make an offer. It gets accepted. During escrow, you receive a stack of HOA documents. CC&Rs, bylaws, budgets, meeting minutes, maybe a reserve study. It's 200-400 pages.

Your agent says something like "let me know if you have any questions." You skim the first few pages, see a lot of legal language, and move on. You're busy picking paint colors and scheduling the move.

The problem is that these documents contain information that can completely change the economics of your purchase. A special assessment the board voted on last month. A rental restriction that kills your backup plan to rent it out if you relocate. A reserve fund so low that a major repair could cost every owner $10,000 or more.

None of this shows up in the listing. Your inspector won't catch it. And your lender might not flag it until it's too late.

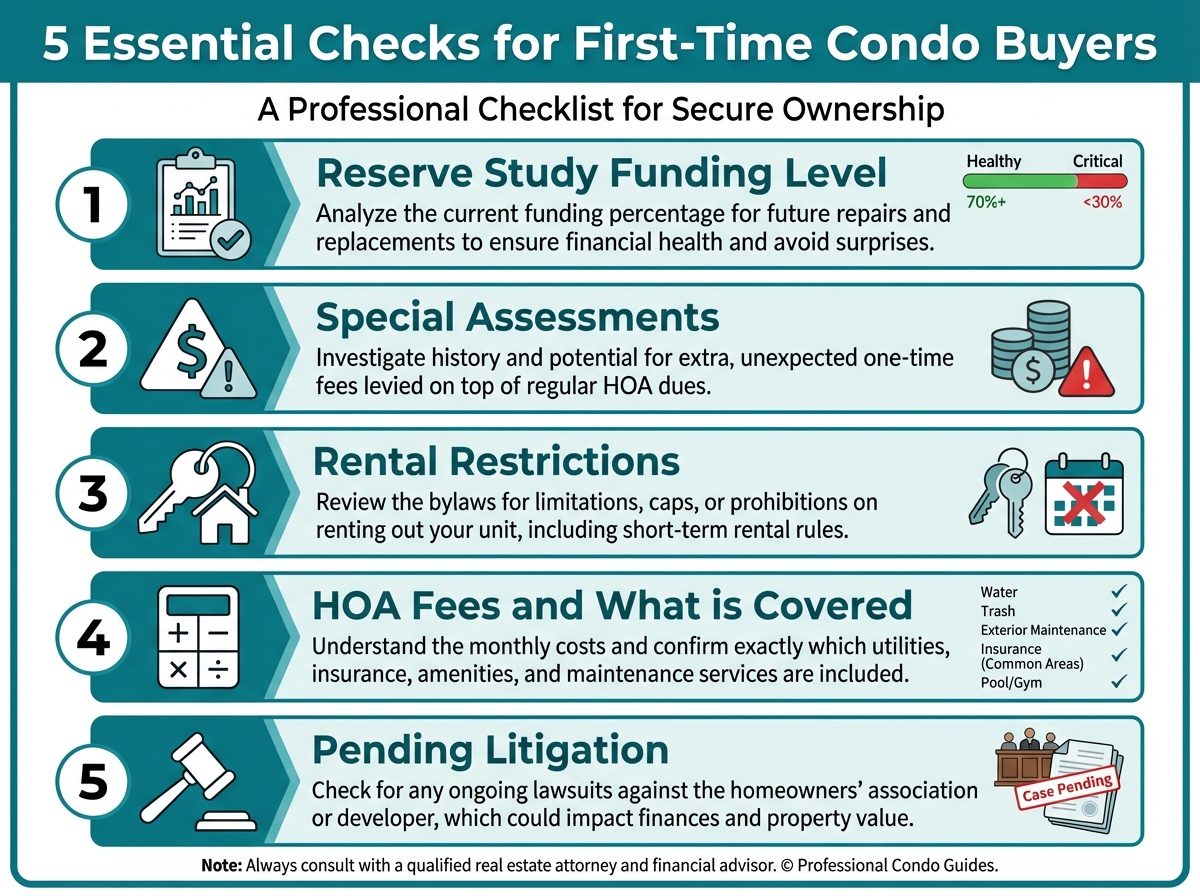

5 Things Every First-Time Buyer Must Check

These five items in your HOA documents can reveal thousands of dollars in hidden costs before you close.

Five critical items to review in your HOA documents before closing

1. Reserve Study Funding Level

The reserve study tells you how much money the HOA has saved for major repairs like roofs, elevators, parking structures, and plumbing. The key number is percent funded.

Industry standard is 70% funded or higher. Below 50% is a warning sign. Below 30% means the association almost certainly can't cover a major repair without hitting owners with a special assessment.

In Florida, new laws now require condos to fully fund reserves for structural components. Across our analysis of 1,900+ HOA documents, 1 in 3 reserve studies were below 50% funded. If your building is in that group, you need to know before you close.

2. Current or Planned Special Assessments

A special assessment is a one-time charge to every unit owner, usually for a major repair the reserve fund can't cover. These can range from $5,000 to $50,000+ per unit. In extreme cases, like some Florida condos dealing with structural compliance, assessments have reached $100,000-$400,000.

Check the board meeting minutes from the last 12 months. If the board has been discussing roof repairs, elevator replacements, or structural issues, an assessment could be coming. Also check the current year's budget for any line items labeled "special assessment" or "capital contribution."

Ask the seller directly: are there any pending or planned special assessments? Get the answer in writing.

3. Rental Restrictions

Even if you plan to live in your condo forever, rental restrictions matter. Life changes. Job relocations, marriage, family growth. If you can't rent your unit, your only option is to sell.

Check the CC&Rs for rental caps (e.g., only 20% of units can be rented at any time), lease minimums (e.g., 12-month minimum, no short-term rentals), and outright bans on leasing. Some associations require board approval before you can rent.

Rental restrictions also affect resale value. A building where 50% of buyers want the option to rent but can't will have a smaller buyer pool when you sell.

4. HOA Fees and What They Cover

The monthly HOA fee on the listing is just a number. What matters is what it includes. Some associations cover water, sewer, trash, insurance, and reserves in the monthly fee. Others cover almost nothing.

Look at the annual budget. Check whether reserves are being funded from monthly dues or if the board is keeping fees artificially low by skipping reserve contributions. Low fees today can mean a massive special assessment tomorrow.

Also check the history of fee increases. If fees have jumped 10-15% per year for the last three years, that trend is likely to continue.

5. Pending Litigation

Lawsuits against the HOA can signal deeper problems. Construction defect suits, personal injury claims, disputes with contractors. These cost money to defend, and the legal fees come out of the association's budget.

Check the meeting minutes and the financial statements for any references to legal actions, attorney fees, or settlement discussions. Ongoing litigation can also make it harder to get financing, since lenders view it as a risk to the building's financial health.

The 3-Day Review Problem

In many states, buyers get just 3 calendar days to review hundreds of pages of HOA documents and decide whether to move forward.

Three calendar days. Not business days. If the documents land on a Friday evening, your deadline is Monday. Good luck finding a real estate attorney or CPA over the weekend.

Most first-time buyers don't know what they're looking at. The documents are written by lawyers, for lawyers. Reserve studies are full of spreadsheets and component inventories. Meeting minutes reference motions, quorums, and board resolutions. None of it is written for someone buying their first home.

The result? Most buyers waive the review period entirely. They trust their agent, hope for the best, and sign. For a deeper look at why this system fails, see our guide on Why the 3-Day HOA Review Period Fails Buyers.

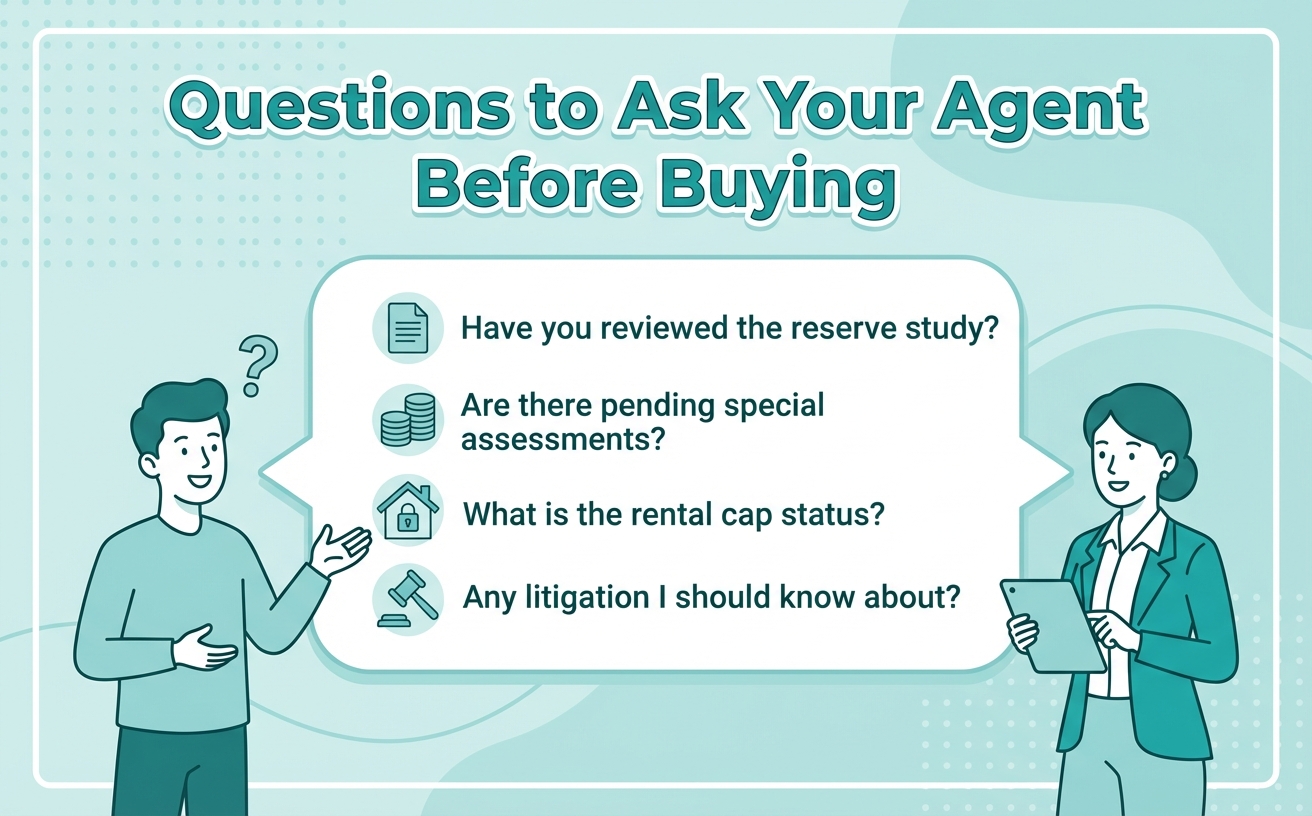

Questions to Ask Your Agent

Your agent should be able to answer these questions. If they can't, that's a red flag on its own.

Key questions every first-time condo buyer should ask their agent

A good buyer's agent should be able to walk you through the HOA documents and point out potential issues. If your agent treats the HOA review as a formality, you may want a second opinion.

What $10K in Surprise Assessments Looks Like

A special assessment four months after closing can wipe out your emergency fund and leave you financially trapped.

Here's a real scenario. A first-time buyer closes on a condo for $350,000. They put 5% down. They've got $8,000 left in savings after closing costs and moving expenses. Four months later, the board votes on a $12,000 per-unit special assessment for elevator modernization.

The warning signs were in the documents. The reserve study showed the building was 22% funded. Meeting minutes from six months before the sale mentioned "deteriorating elevator equipment" and "contractor bids." The annual budget showed zero being contributed to elevator reserves.

The buyer didn't read the documents. Their agent didn't flag it. Now they're $4,000 short on an assessment they can't avoid, in a home they just bought.

The cost of not reading HOA documents

A $12,000 special assessment on a $350,000 condo is a 3.4% hit on top of your purchase price. That's money that could have been negotiated off the sale price, or a reason to walk away entirely. Fifteen minutes reviewing the reserve study could have saved $12,000.

How to Get Help Fast

You have options for reviewing HOA documents, ranging from free to a few hundred dollars. The right choice depends on your timeline and comfort level.

DIY With a Checklist

Free

- ✓No cost

- ✓Covers the basics

- ⚠Easy to miss things

- ⚠Requires HOA knowledge

AI Document Analysis

$49-79 per property

- ✓Fast (results in minutes)

- ✓Covers all document types

- ✓Flags specific red flags

- ✓Links claims to source pages

Real Estate Attorney

$300-500+

- ✓Legal expertise

- ✓Can advise on contract

- ⚠Hard to find in 3 days

- ⚠Higher cost

For most first-time buyers, the sweet spot is a combination. Use an AI analysis tool to quickly identify red flags, then consult an attorney if something serious comes up. That way you're not paying attorney rates to read 300 pages of boilerplate, but you have professional backup when it matters.

Bottom Line: Read the Documents Before You Sign

Buying your first condo is one of the biggest financial decisions you'll make. The HOA documents aren't just paperwork. They tell you what you're actually buying into: the financial health of the building, the rules you'll live under, and the costs that aren't in the listing price.

Key takeaways:

Don't Buy Blind

Upload your HOA documents and get an instant breakdown of reserve funding levels, special assessment risk, rental restrictions, and red flags. Built for buyers who don't have time to become HOA experts.

Try Free CC&R Analysis →No signup required. Upload your CC&Rs and get results in under 3 minutes.

Frequently Asked Questions

What HOA documents should I ask for before buying a condo?

Request the CC&Rs (Covenants, Conditions & Restrictions), bylaws, current year's budget, most recent reserve study, last 12 months of board meeting minutes, and financial statements. Together, these give you a complete picture of the association's rules, finances, and any upcoming issues.

What is a good percent funded for an HOA reserve study?

Industry standard is 70% funded or higher. Below 50% is a warning sign that means the association may not have enough saved for major repairs. Below 30% significantly increases the risk of a special assessment. For more detail, see our guide on How to Read a Reserve Study in 5 Minutes.

Can I negotiate the price based on what I find in HOA documents?

Yes. If you find a pending special assessment, low reserves, or other financial issues, these are legitimate reasons to renegotiate. A $10,000 expected assessment is a valid basis for a price reduction. Your agent can help structure the negotiation.

What happens if I find a problem during the review period?

During the HOA document review period, you typically have the right to cancel the contract without penalty. If you find a serious issue, you can walk away, renegotiate the price, or ask the seller to address the problem. Consult your agent or attorney about the specific terms of your contract.

Do HOA fees ever go down?

Rarely. HOA fees typically increase over time as maintenance costs, insurance premiums, and labor costs rise. Associations that keep fees artificially low are often underfunding their reserves, which leads to special assessments later. Steady, moderate fee increases are actually a sign of responsible management.

Sources & References

- Community Associations Institute (CAI) — Industry standards for reserve study funding levels

- National Association of Realtors (NAR) — 75.5 million Americans live in HOA communities

- GoverningDocs analysis of 1,900+ HOA documents (reserve studies, CC&Rs, meeting minutes, budgets)

This article is for informational purposes only and does not constitute legal, financial, or professional advice. HOA rules vary by state and association. Consult a licensed real estate attorney or qualified professional for guidance specific to your situation.